Vehicle Sales, Operating Population and Utilization Lead to Aftermarket Demand Growth

Aftermarket demand for Class 6-8, trailers, and container chassis in 2018 is expected to total $30.1 billion, according to John Blodgett, vice president, sales and marketing, of MacKay & Co.

U.S. aftermarket demand for Class 6-8, trailers, and container chassis in 2018 is expected to total $30.1 billion once final numbers become available.

Source: MacKay & Co.

U.S. aftermarket demand for Class 6-8, trailers, and container chassis in 2018 is expected to total $30.1 billion once final numbers become available, according to John Blodgett, vice president, sales and marketing, of MacKay & Co., speaking at Heavy Duty Aftermarket Dialogue in Las Vegas.

Vehicle population plays a big role in what happens in the aftermarket. Blodgett shared figures from Wards and FTR showing Class 8 retail sales for 2018 were up 31% and are forecast to be up an additional 10% this year to 274,000 units. However, by 2020 that number is expected to drop by 12%. For comparison’s sake, 20 years ago that number was 189,000.

Class 6 and 7 retail sales for 2018 were 136,000. They are expected to be flat this year and then fall 4% in 2020. Trailer sales reached 316,000 units in 2018; predictions are for them to fall by 2% this year and 8% in 2020.

In 2018 there were 825,000 Class 6 vehicles operating in the U.S., 1.33 million Class 7 vehicles, 3.4 million Class 8 vehicles and 4.6 million trailers. MacKay’s forecast calls for the operating population of Class 6 vehicles to grow by 12% by 2023, Class 7 to decline 6%, Class 8 to grow 8%, and the trailer population to grow 7%.

Vehicle utilization is another factor that drives aftermarket demand, and for the forth quarter of 2018, Class 6-8 power unit utilization was at 85.3%, according to MacKay data.

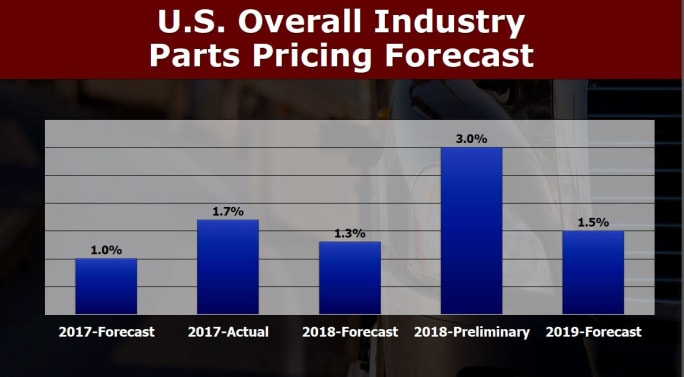

MacKay is predicting a 1.5% price increase for U.S. parts in 2019, on top of a 3% price increase seen in 2018.

Source: MacKay & Co.

MacKay is predicting a 1.5% price increase for U.S. parts in 2019, on top of a 3% price increase seen in 2018.

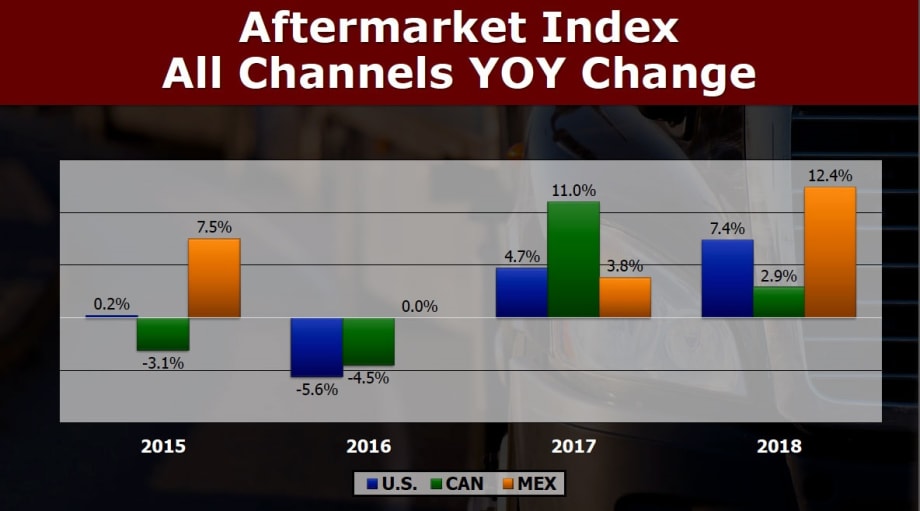

For 2018, MacKay’s Aftermarket Index shows demand up 7.4% in the U.S., 2.9% in Canada and 12.4% in Mexico. Looking further into the number, Blodgett says that in the U.S. the OES channel saw 9.7% growth year over year, while the independent channel was up 4.2%.

In the U.S. truck dealers have 49% of the aftermarket business, distributors 18%, and independent repair garages 9%. The balance of aftermarket sales are through other sources including specialists (7%), engine distributors (5%), auto parts distributors (4% and other sources (8%).

Presenting data based on input from more than 700 fleets, Blodgett said the number one concern for fleets in 2019 is the state of general economic activity, followed by the driver shortage, the complexity of new components (this was the number one fleet concern in 2018), and the technician shortage.

Looking to the future, Blodgett forecast U.S. aftermarket demand as follows:

2019 $31.1 billion

2020 $32.2 billion

2021 $33.3 billion

2022 $34.9 billion

2023 $36.3 billion

Related: Economic Growth Ahead at Trend Level, Says Economist at Aftermarket Event

More Aftermarket

What Three Fleets Are Doing Differently When Buying Truck Parts in 2026

With freight improving but costs still climbing, fleet maintenance executives explain how they're balancing price, quality, and supplier relationships.

Read More →

ConMet Expands Aftermarket Brake Drum Lineup With TruCast

A new heavy-duty truck brake drum option in the aftermarket gives customers more flexibility within the ConMet product family.

Read More →

Phillips Opens High-Tech Distribution Center for Faster Parts Delivery

Phillips Industries’ new Cincinnati-area distribution center is now shipping aftermarket trucking parts nationwide, aiming to speed up delivery times for customers.

Read More →

Volvo to Sponsor America’s Road Team for 2025

Volvo Trucks announced that it is extending its exclusive sponsorship of America’s Road Team for 2025.

Read More →

Webb to Start Taking Orders for UltraSet Pre-Adjusted Wheel Hubs

Webb, which recently acquired the Stemco Trifecta pre-adjusted hub program, will soon start taking orders for its replacement pre-assembled hub, the UltraSet.

Read More →

All-Makes Automatic Brake Adjusters, Ride Height Control Valves from Midland

SAF-Holland has added automatic brake adjusters and ride height control valves to its Midland All-Makes Program.

Read More →

ZF Aftermarket Expands [pro]Academy Training

ZF Aftermarket said it is expanding its ZF [pro]Academy training and will be adding 40 new modules this year.

Read More →

Eaton Adds Remanufactured Advantage Line of Clutches

Eaton has added its Advantage clutches to its remanufactured product line. The clutches feature a unique strap drive intermediate plate designed to allow customers to choose the latest OE specification

Read More →

ConMet Acquires TruckLabs, the Creator of TruckWings

Commercial truck and trailer parts provider ConMet acquired TruckLabs, the company that created TruckWings, an aerodynamic device that attaches to truck cabs and deploys to close the gap between truck and trailer. TruckLabs now operates as a subsidiary of ConMet.

Read More →

Diesel Laptops Releases Fault-Code-to-Part-Number Tool

Diesel Laptops said its Truck Fault Codes allows users to input a fault code and immediately identify and order the parts needed to complete repair work.

Read More →