Analysis Shows Shifting Port Patterns, Spot Market Bottom

What can shifting patterns of port use and the related impact on intermodal, the spot market reaching bottom, and orders for Class 8 tractors and trailers tell us about the health of the trucking industry? Find out what FTR said in its State of Freight webinar.

More carriers with 100 trucks or more have been lost in the first five months of 2023 than in the same period last year.

Source: FTR

Avery Vise, of FTR, sees the bottom of the spot market.

Source: FTR

What can shifting patterns of port use and the related impact on intermodal, the spot market reaching bottom, and orders for Class 8 tractors and trailers tell us about the health of the trucking industry? Panelists provided insights during FTR Transportation Intelligence's State of Freight webinar June 8.

Eric Starks, FTR chairman, led the discussion and was joined by Avery Vise, vice president, trucking; and Todd Tranausky, vice president, rail and intermodal.

After touching on broader economic conditions, the panel turned to discussing ports, corridors, and trucking trends they see in the data.

Ports and Intermodal

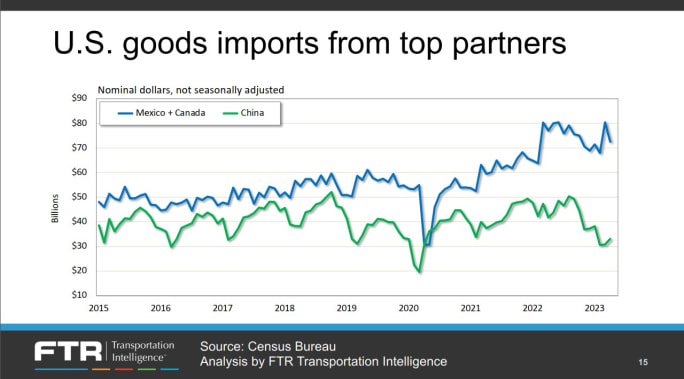

Vise provided a look at U.S. goods import data. He compared China to Mexico and Canada combined, noting that imports from Mexico/Canada have always exceeded China — but the gap has widened. He pointed to a widening of the gap in 2019 that he said was largely due to the Trump administration’s tariffs placed on China.

The gap between Mexico/Canada imports and China imports is growing.

Source: FTR

It’s still too early to draw a conclusion about the role of nearshoring in this trend, Vise explained. In a follow-up conversation with HDT, Vise explained that the difference is partly driven by the nature of what's being imported.

The key background is that imports from China are heavily skewed toward consumer goods (electronics, toys, apparel, etc.) while imports from Mexico (especially) and Canada are heavily focused on the automotive sector.

"Basically what has been happening is that imports of consumer goods have been falling while imports of vehicles and parts have been rising," Vise said. "So the divergence probably is not due mostly to near-shoring — although near-shoring probably is a contributor — but rather is a function of the broader trends in what goods the U.S. is importing."

The discussion around imports transitioned to further talks of ports and intermodal, with Tranausky providing some insight.

“To set the stage at a basic level, imports are running above where they were before the pandemic. Exports are not quite that same story; exports continue to struggle. Exports have not come back to nearly the same level that imports have,” he explained.

Digging into the details of how port activity is transitioning to the Gulf Coast and East Coast and away from the West Coast, Tranausky said, “Historically, the West Coast has always been the big dog. But you can see over time, even before the pandemic, that delta between the West Coast and everybody else was already narrowed.

"And then we got to 2019, we got to the pandemic, and we got to the period after the pandemic. And everybody remembers all the congestion on the West Coast and all the issues that we were facing in moving goods," he said.

“So, folks went and looked at other alternatives. They went to Houston, they went to Savannah, they went to New York. What's happened, even as imports have declined, you've seen the East and Gulf Coast ports hold up better than the West Coast. They definitely felt the decline, but they felt it a little bit later and not as drastically as what folks have seen on the West Coast,” he added.

Those changes have dictated shifts in where intermodal equipment is positioned and where carriers provide services. Some carriers started providing new services, he pointed out, using Houston as an example.

Once the economy normalizes, the question will be if the West Coast can regain the position they have lost or if companies will continue to use ports they have adjusted to in recent years, Tranausky said.

In general, he pointed out that as the West Coast has lost market share to the other port areas — primarily Gulf Coast and East Coast — these shifts to new ports impact the intermodal corridors that link the ports to other areas.

“But I'll say this, it's been nearly a year that we haven't had a contract on the West Coast when it comes to labor. And so, folks have gotten used to using these alternative ports. They've developed new relationships with transportation suppliers. They may not just flip a switch and come back to the West Coast,” Tranausky added.

Spot Market Bottom

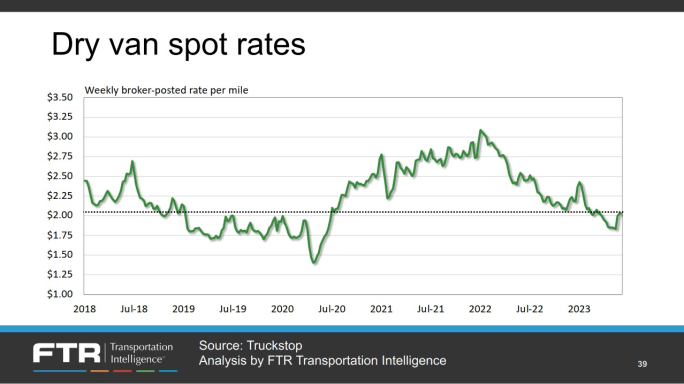

Vise turned to load metrics, using dry van loads as an example, and reported they are running “fairly close” to where they were in 2019. He pointed out a number of similarities between 2019 and 2023.

“And in fact, when we look at rates, you see something very similar, where those rates have come down from very high levels. But they have started to recover,” he said.

“Our assessment is that spot rates have bottomed out. I think it's fairly clear at this point, absent a big negative change in some of the macroeconomic issues that I talked about earlier, that we've bottomed out and will, at worst, probably flatten out, from the perspective of carriers at least,” Vise said.

He sees a flat environment as far as freight is concerned in general and added that is very similar across segments, although refrigerated is a little stronger and flatbeds a little weaker.

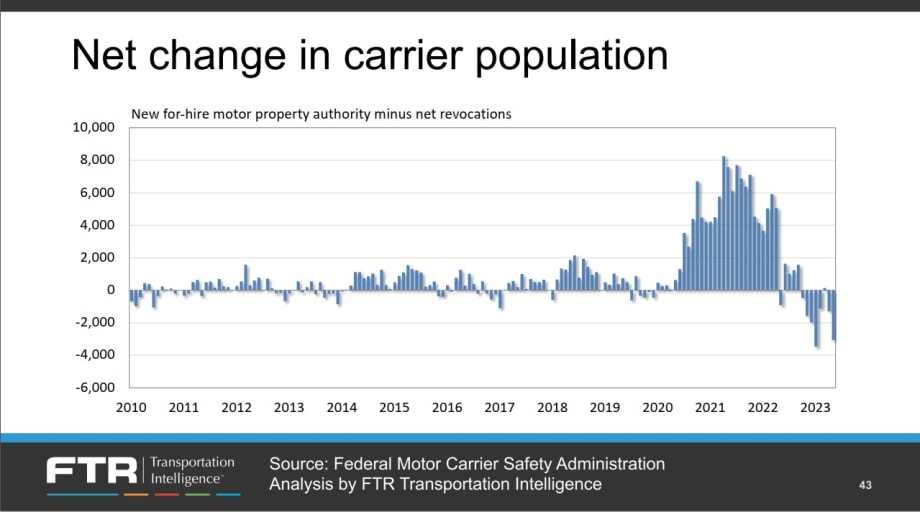

The growth trend in trucking employment has now reversed.

Source: FTR

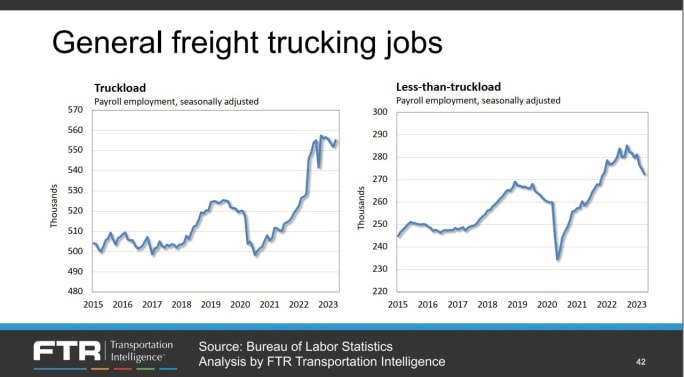

The numbers also show that capacity starting to shift. Vise pointed to a flattening in growth in overall payroll employment in trucking. But a different pattern in employment is detected between less-than-truckload and truckload.

“There are a couple of factors behind this. One is LTL has a lot of jobs that are not driving, relative to truckload. Truckload is very heavily driver-centric and tends to have pretty low overhead relatively speaking, certainly relative to LTL. So that's one factor,” he said.

“But I think there's another factor that's in play here as to why the overall payroll employment is still high in truckload and has been falling fairly consistently in the LTL. And that's because there are no owner-operators in LTL and so, there's a little bit of a boost that I think payroll employment is getting due to the shift in what we're seeing in the market,” he explained.

Tying it all together, he said he sees an incremental increase in spot rates, but it’s going to be very gradual, especially through this year, and the contract market still hasn’t quite bottomed out. Avery said that bottom is getting very close, but it probably will take the remainder of the year to actually get to that bottom.

Losing Carriers

In looking at the net change in motor carrier population, Vise pointed out increases from 2014 to 2015 and from 2018-2019.. However, the number of new motor carriers grew drastically from the middle of 2020 through 2022. That growth trend is now reversing.

“It started reversing really in October," Vise said. "It had slowed before then, and we've seen some very large declines this year. Some of them are a little bit calendar-driven just because of the nature of how the data falls in the month, but it's clear we're losing these carriers — most of them very small. So, they're freeing up drivers and those drivers have gone to work for truckload carriers,” he explained.

Larger carriers are now “starting to see more pain” as well.

Vise referenced an analysis he did of the first five months of 2022 compared to the same period in 2023. During that period in 2022, 10 carriers with 100 or more trucks were lost. In comparison, in the first five months of this year, 31 carriers with 100 trucks or more were lost.

He explained that if we consider the flattening of payroll employment in trucking in light of the net decrease in the number of carriers that we have seen since last fall, the trucking industry almost certainly is losing a significant number of drivers. Therefore, even with stagnant freight volumes, capacity is starting to tighten. FTR assesses the relationship between demand and capacity through a metric called active truck utilization, and its latest forecast suggests that utilization has bottomed out.

Equipment Purchases

In analyzing orders for new Class 8 trucks, Vise noted the number of orders have not collapsed. Yes, they have been falling, and now starting to fall below replacement range, he explained.

“But a lot of that has to do not so much with fundamental demand, or at least we're not sure it is. It has to do more with the fact that build slots are basically completely full for the rest of this year. The OEMs have not opened up build slots yet for 2024 and therefore you essentially just can't order anymore. So, we could actually see this number come down for the next couple of months to below 10,000,” said Vise.

He reported something similar in net orders for trailers but pointed out that the number of trailers ordered in April nearly matched the number of Class 8 units ordered in May. As is happening with tractors, the numbers are being held back because the production slots are “quite stressed,” according to Vise.

“But I think the larger point is we haven't seen them fall to extraordinarily low levels, like we saw, for example, in 2019,” he pointed out.

More Fleet Management

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →

Import Cargo Volume to See Year-Over-Year Gain Again in June, Then Remain Below 2025 Levels Into Fall

After July, the report predicts a weakening in import volume as consumer uncertainty remains high and the impact of increasing inflation takes its toll.

Read More →

AUCTION OF EQUITY INTEREST IN HEAVY HAUL TRUCKING COMPANY!!

Mark your calendar: June 30, 2026 (10:00 a.m. PDT). A 37.5% ownership interest in MagnaTrans, LLC, a California limited liability company doing business as Magna Transportation Group, will be sold in an in-person and online auction to the highest bidder or bidders under Article 9 of the Uniform Commercial Code. The Rancho Cucamonga-based heavy haul and over-dimensional trucking company operates across California, Oregon, and Arizona.

Read More →

Volvo Trucks Adds Unattended Over-the-Air Software Update Capabilities

The latest evolution of Volvo’s over-the-air update technology allows software updates to run while trucks are parked, helping fleets keep vehicles current without disrupting operations.

Read More →

How Waste Connections is Using Data, Telematics, and AI

How do you manage and maintain more than 18,000 connected trucks? Data. Lots of it.

Read More →