Are We Near the Bottom of the Freight Cycle?

ACT Research reports the supply and demand dynamics in the freight market are beginning to recover. Its recent data suggests demand fundamentals improving and capacity starting to tighten may signal the industry is approaching the bottom of the freight cycle.

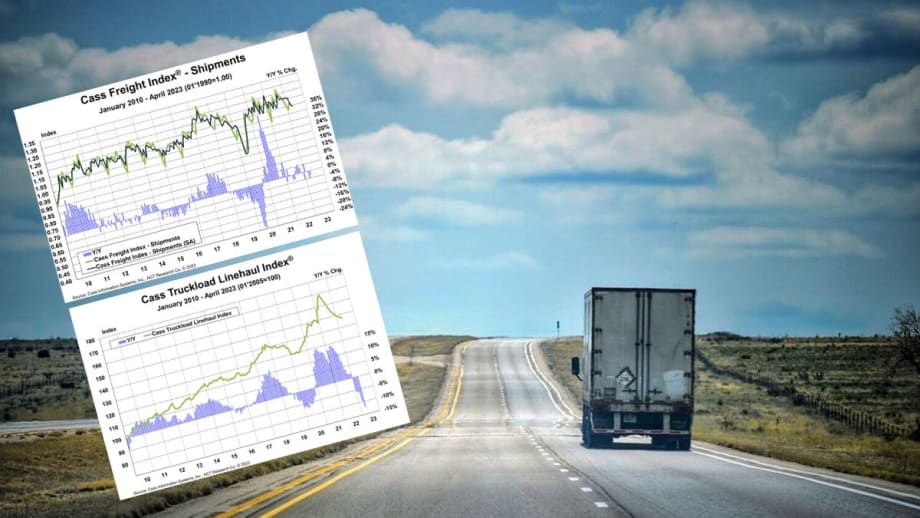

Supply and demand numbers indicate the freight cycle is approaching the bottom.

Source: ACT Research/Cass Information Systems/Canva

ACT Research reports the supply and demand dynamics in the freight market are beginning to recover. Its recent data suggests demand fundamentals improving and capacity starting to tighten may signal the industry is approaching the bottom of the freight cycle.

“After a long soft patch, we see the U.S. freight transportation industry on the verge of a new cycle as we begin to transition from the bottoming phase into the early phase of the freight cycle in the months to come,” Tim Denoyer, ACT Research’s vice president and senior analyst, said in the Cass Transportation Index Report April 2023.

The latest release of the ACT Freight Forecast report points out that the freight cycle is “still weak” and truckload spot rates are nearing the bottom.

Truckload Volume Index

According to the Truckload Volume Index, freight volumes dropped and national average spot rates for dry van and refrigerated loads fell for the fourth consecutive month in April, said DAT Freight & Analytics.

Van TVI was 206, down 15.5% from March and 12.3% lower year over year.

Reefer TVI fell to 154, a 16.3% decline from March and 12.5% lower year over year.

Flatbed TVI was 239, 13.7% lower compared to March but 3.5% higher year over year.

DAT also reported the national average load-to-truck ratios decreased, indicating weaker demand for truckload capacity on the spot market.

Van ratio: 1.9, down from 2.0 in March, and 3.4 in April 2022.

Reefer ratio: 2.7, down from 3.0 in March and 6.3 year over year.

Flatbed ratio: 12.1, down from 12.1 in March and 64.5 year over year.

According to DAT, this lower demand for truckload services led to a drop in national average spot van and reefer rates:

The spot van rate averaged $2.06 per mile, down 10 cents compared to March and 71 cents lower year over year.

The spot reefer rate fell 9 cents to $2.41 a mile, 72 cents lower than in April 2022.

The spot flatbed rate dipped 4 cents to $2.67 a mile, down 70 cents year over year.

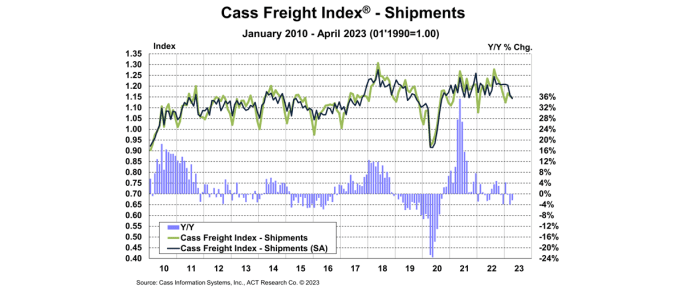

Cass Freight Index

The Cass Freight Index shows shipments declined 2.4% in April when compared to the same period last year. Data within the Index includes all domestic freight modes and is derived from 36 million invoices and $44 billion in spend processed by Cass annually on behalf of its client base of hundreds of large shippers. The diversity of shippers and aggregate volume provide a statistically valid representation of North American shipping activity, according to Cass.

The shipments component of the Cass Freight Index fell 2.4% in April compared to the previous period last year.

Source: ACT Research/Cass Information Systems

According to the report, warm weather appears to have pulled some freight shipments into January and February instead of shipping in March and April. When seasonally adjusted, the index declined 1.3% from month to month in April, which followed a 3.8% drop in March.

“With produce season arriving late this year and the freight market likely passing the peak of the destock, freight demand is near the bottom,” said Denoyer. “With inflation easing, improving real income trends will allow for a bit more holiday spending this year, when even less destocking will mean more freight volume.”

Fleet Capacity

Regarding fleet capacity, Denoyer explained, “Interstate operating authorities are contracting at a record rate, with about 11,000 net revocations since last October, including about 1,600 net revocations in April. Total revocations were about 10,800 in April, near record levels, but grants and reinstatements are also elevated. This is beginning to tighten capacity, which will also help spot rates find the bottom and begin to rise.”

He also pointed out long-distance trucking employment is contracting, as reflected in a first-quarter decline of 8,700 jobs. Those numbers marked a 1.0% decrease; however, driver employment numbers were still up 3.0% year over year in that latest March data point. Denoyer said the series will be down on a year-over-year basis by June on its current level. Denoyer also said since trends in employment follow trends in freight rates, long-haul jobs are set to decline this year.

Denoyer concluded, “The intersection of additional volume and tightening capacity underpins our forecast for a near-term bottom in spot truckload rates. We’ve been expecting the bottom roughly around this month since we introduced 2023 spot rate forecasts 16 months ago, and we still think RoadCheck this week will help usher in a new freight cycle.”

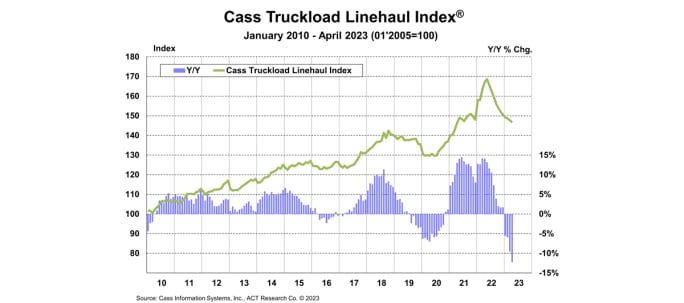

The Cass Truckload Linehaul Index fell 12.3% in April compared to last year, following declines in March.

Source: ACT Research/Cass Information Systems

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →