From the HDT archives (2019): Trucking Looks for Solutions to California's Stringent New Independent Contractor Law

Can Strong Job Growth in Trucking Continue?

FTR's Avery Vise explores how trucking employment, truck order backlogs, fuel prices, motor carrier failures, and the attack on the independent contractor model all tie together.

by Avery Vise, FTR

June 15, 2022

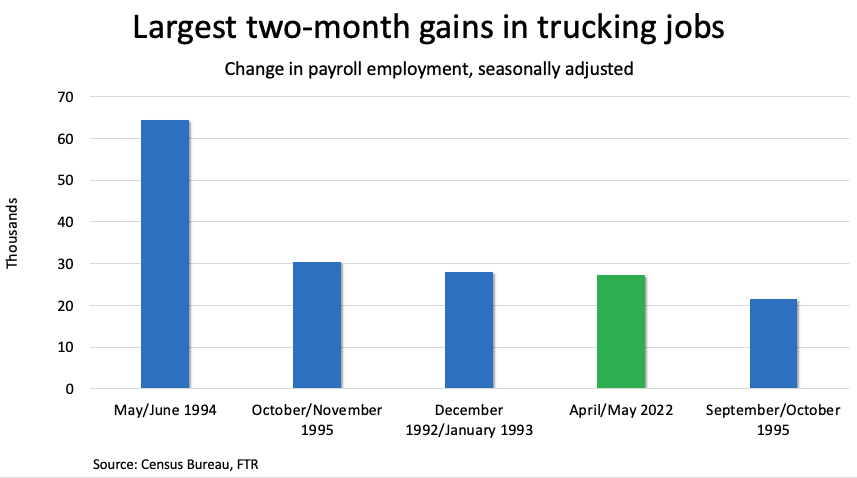

Only three times in the 32-plus years of available data has trucking seen a larger two-month surge in trucking employment. And at least one of those (May to June 1994) resulted from the resolution of a huge Teamsters strike.

Source: FTR

4 min to read

In April and May combined, the for-hire trucking industry added 27,300 payroll jobs (seasonally adjusted), according to the latest Bureau of Labor Statistics data. That puts trucking employment at the highest on record and 65,900 payroll jobs, or 4.3%, ahead of the pre-pandemic month of February 2020.

Only three times in the 32-plus years of available data has trucking seen a larger two-month surge in trucking employment. And at least one of those (May to June 1994) resulted from the resolution of a huge Teamsters strike.

As we reported recently, the number of trucking companies leaving the market has begun to rise, most of those single-truck carriers. But the data on DOT authority revocations clearly lags the reality of the marketplace. Given an unprecedented surge in diesel prices and, until recently at least, steadily weakening dry van and refrigerated spot rates, we presume that we have already seen a sharp increase in the number of those owner-operator drivers looking for a more stable environment in which they are less exposed — or perhaps not exposed at all — to higher fuel costs and rate volatility. That growing pool of willing recruits probably was a significant contributor to the extraordinary job growth in the past two months.

With diesel prices showing no signs of collapsing, the ground for recruiting should remain fertile as long as freight demand is solid. The relatively tamer volumes and rates in dry van and refrigerated appear to reflect primarily a shift of activity to the contract arena rather than a drop in overall demand. Given the unprecedented shift of capacity and volume into the spot market over the past two years, this trend could continue, assuming no limitations other than driver availability.

Truck Supply + Fuel Costs = A New Driver Model?

A ready supply of drivers is not the only issue, however. Add to the list of unprecedented situations the constraints on truck production due to the semiconductor shortage and other supply-chain problems. “Official” lead times for obtaining new trucks have come down from levels seen in 2021, although they are still nearly as high as the pre-pandemic peak in December 2018. However, the formal backlog-to-build metric is misleading. Truck manufacturers are unable to slot tens of thousands of would-be truck orders because they simply do not know when they can build them. So the true lead time for trucks clearly is higher than the more than 10 months FTR reports.

Constraints on new truck availability raise some interesting challenges for fleets. Carriers could snap up used trucks, which presumably should become increasingly available as these single-truck operations fail in greater numbers. However, many carriers will avoid doing that unless absolutely necessary, because operating used trucks — especially older ones — complicates maintenance practices and increases maintenance costs.

The more attractive approach for most carriers probably is to take on former independent carriers as leased owner-operators. Indeed, most of those small carriers probably had been leased owner-operators before the pandemic. However, today’s landscape is different. For starters, the leased owner-operator model is under attack. Indeed, it is even possible that by July they will be illegal altogether in California, depending on what the U.S. Supreme Court decides.

Fuel costs arguably are another hurdle to converting failing independent carriers into leased owner-operators. Even though the leased operator might get pass-through fuel surcharges, the time lag between payment and reimbursement is potentially a big pill to swallow. Many operators who have struggled due to surging diesel prices likely want out of the fuel-buying process altogether, preferring instead company driver jobs that give them company-paid fuel cards.

As aversion to fuel purchasing meets constraints on new trucks, FTR believes we could see growing interest in a new model where the larger carrier agrees to buy the single-truck carrier’s truck and to hire the driver to operate it. Think of it almost as the reverse of a typical lease-purchase agreement. We do not expect such an approach to become common, but it could be one way some carriers can deal with the current environment.

Avery Vise is FTR’s vice president of transportation.

Subscribe to Our Newsletter

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →