Related: DAT Analytics Guru Explains how Freight Forecasting Works

Cautious Optimism for a Better 2024 for Trucking

As the U.S. economy stuttered along in 2023 toward a hoped-for “soft landing,” trucking struggled. But many economic and trucking industry analysts believe 2024 is looking up.

January 24, 2024

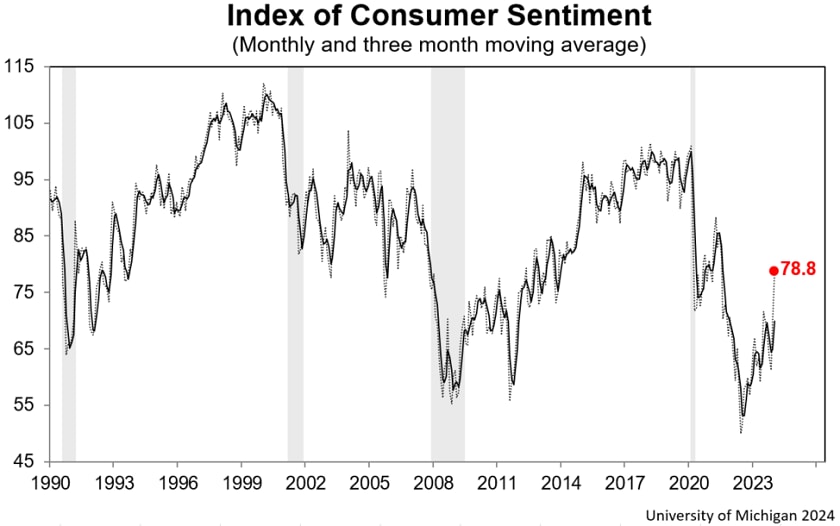

Consumer sentiment is looking better, according to a University of Michigan index.

Source: University of Michigan

8 min to read

As the U.S. economy stuttered along in 2023 toward a hoped-for “soft landing,” trucking struggled. But many economic and trucking industry analysts believe 2024 is looking up, especially in the second half of the year.

The transportation analysts at Stifel recently reported that for public trucking company earnings, “last year represented the worst annual financial comps … since the [Great Recession] as the Pandemic-era ‘sugar rush’ to earnings came to a screeching, cyclical halt.”

Many fleet management teams overestimated their earning ability during what Stifel called “an unusually long trough.”

However, Stifel reported that truckload rates have returned to a pattern of normal seasonality after ticking up prior to the holidays, and barring any major economic disasters, it anticipates that pattern to continue.

Demand during the first half of 2024 is expected to be “generally sluggish, though stable,” Stifel said. “As a result, we think supply will be a greater near-term determinant of spot rates, and diesel prices will be a key indicator when monitoring capacity changes.”

Consumer sentiment looks to be improving, according to the University of Michigan’s consumer survey.

“Consumer sentiment soared 13% in January to reach its highest level since July 2021, showing that the sharp increase in December was no fluke,” wrote Surveys of Consumers Director Joanne Hsu. “Consumer views were supported by confidence that inflation has turned a corner and strengthening income expectations. Over the last two months, sentiment has climbed a cumulative 29%, the largest two-month increase since 1991 as a recession ended.”

Improving Freight Cycle Fundamentals

The trucking industry analysts at ACT Research believe U.S. freight cycle fundamentals will improve in 2024.

Freight demand is below trend, but starting to recover, as post-pandemic effects fade. Both real disposable incomes and retail sales are accelerating, ACT said, and disruptions in ocean shipping are likely catalyzing the end of the 18-month destock.

“The new year begins with global shipping in turmoil, import freight shifting from East to West, and for-hire demand on the long side of a two-plus-year downturn,” said Tim Denoyer, ACT Research’s vice president and senior analyst. “Changing ocean and inventory dynamics support an upturn in freight demand, particularly intermodal, where we raise our rate forecasts this month.”

Global ocean shipping disruptions will likely change freight patterns and could bring more to trucking, especially intermodal.

“The two primary routes from Asia to the U.S. East Coast have been severely impacted by conflict in the Red Sea and low water in the Panama Canal,” Denoyer explained. “This is pressing freight to the west coast ports, where the intermodal network will likely experience strong demand, which will eventually flow into the truckload market.”

“Real retail sales recently turned positive after a year of declines, and after 18 months of destocking, a restock is drawing near, spurred by ocean risks. Supply dynamics are also shifting as 2024 begins, setting up a new stage of the cycle. While partly temporary, the mid-January cold-related slowdown in rail volumes is already sparking truckload spot activity,” Denoyer added.

‘New Normal’?

2024 may give the freight market a sense of the “new normal,” according to Motive’s first monthly economic report of the year.

“After three years of impacts from the pandemic and major external forces disrupting the freight market, 2024 may be the first time carriers will get a sense of what the new normal will look like,” Motive analysts said in the report. “Retailers are re-stocking inventories again, potential interest rate cuts could mean better access to capital, and consumer demand could be less volatile if inflation keeps cooling.

"While we will likely continue to see overall contraction of the freight market, we expect that 2024 will be less volatile, creating more predictability in freight and inventory planning.”

Motive’s data showed the trucking market’s contraction peak in December, though trucking visits to warehouses of the top 50 retailers in the U.S. reached 2023 highs.

“For the coming year, this contraction is set to continue, but market stabilization may not be far off,” they said.

The trucking market saw its highest levels of carrier exits and the lowest number of new carrier registrations in 2023. Motive predicts that this contraction of the freight market will continue in early 2024, but retail trends and economic factors indicate we may see less volatility in the second half of the year. Some highlights from Motive’s report:

Carrier exits: 4,860 carriers excited the trucking market in December, a 52% increase in closures compared to the 2023 average of 3,203.

Carrier entrants: New carrier registrations fell for the fourth consecutive month, dropping 4% month over month to 6,503. This latest decline marks an 18% year-over-year drop and a 43% decrease compared to December 2021, when consumer demand was at some of its highest levels.

Diesel prices: Continued to fall in December, dropping 4 cents to $4.14 per gallon. Experts are predicting that in general, we should see lower average prices at the pump and less volatility in 2024.

Truckload Rates Nearing More Normal Pattern

DAT Freight & Analytics reported that spot truckload rates rose in December and the gap between spot and contract van rates closed to its narrowest point since March 2022, when prices to move truckload freight were near all-time highs.

A convergence of spot and contract rates would signal an end to the current cycle of falling prices for truckload services, according to the company.

“At 39 cents, the spread between spot and contract van rates is still substantial but was down 7 cents compared to November,” said DAT Chief of Analytics Ken Adamo. “The price to move van freight under contract hit its lowest point in nearly three years. Entering 2024, shippers are in a strong position as they negotiate contract rates, and carriers on the spot market have some optimism that the market will turn.”

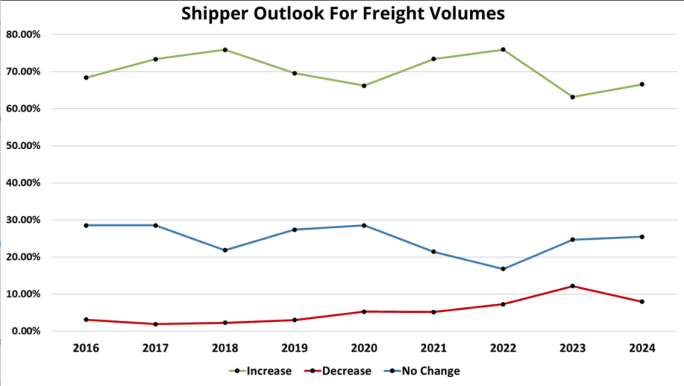

Less-than-Truckload: Shippers Expect to Move More Freight in 2024

“Though the general economy in the U.S. remained resilient throughout 2023, the swift and steep decline in shipping volume was felt within the freight transportation sector,” said Averitt in its 2024 State of the North American Supply Chain report. “Many players in the industry were forced to close their doors, including Yellow Corporation and Convoy Inc., which made headlines week after week.”

In its new survey of more than 1,400 shippers, Averitt reports, 67% of respondents said they anticipate moving more freight in 2024 than in 2023. “This marks a 4-percentage-point gain over the previous year — a positive sign for shippers and carriers alike.”

The results suggest a return to a more stable freight economy, according to Averitt.

Averitt's annual shipper survey shows more expecting to ship more freight in 2024.

Source: Averitt

“This is particularly evident when compared to the turbulent period of 2020-2022, the early years of the pandemic, which were marked by unprecedented uncertainty and a widespread strain on capacity across various sectors.”

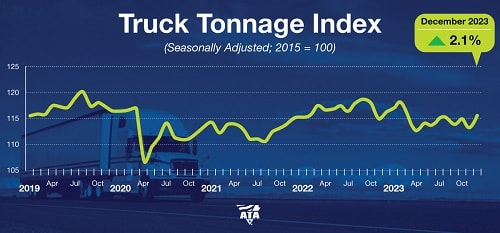

ATA Tonnage Index: 2023 Worst Year Since 2020

American Trucking Associations’ For-Hire Truck Tonnage Index rose by 2.1% in December, capping a down year that the association said was the worst since 2020.

ATA’s advanced seasonally adjusted index increased 2.1% in December after falling 1.4% in November. In December, the index equaled 115.7 (2015=100) compared with 113.3 in November.

“While 2023 ended on a better note, truck tonnage remained in a recession as it continued to fall on a year-over-year basis,” said ATA Chief Economist Bob Costello. “With that said, for-hire contract freight, which is what comprises our index, in December was 2.6% above the trough in April.

American Trucking Associations’ For-Hire Truck Tonnage Index rose by 2.1% in December, capping a down year that the association said was the worst since 2020.

Source: American Trucking Associations

“For the entire year, tonnage contracted 1.7% from 2022 levels. This makes 2023 the worst annual reading since 2020, when the index fell 4% from 2019, and the only year since 2020 that tonnage contracted.”

Compared with December 2022, the seasonally adjusted index fell 0.5%, which was the 10th straight year-over-year decrease, albeit the smallest over that period. In November, the index was down 1.6% from a year earlier.

ATA calculates the tonnage index based on surveys from its membership and has been doing so since the 1970s. In calculating the index, 100 represents 2015. The Index is dominated by contract freight as opposed to spot market freight.

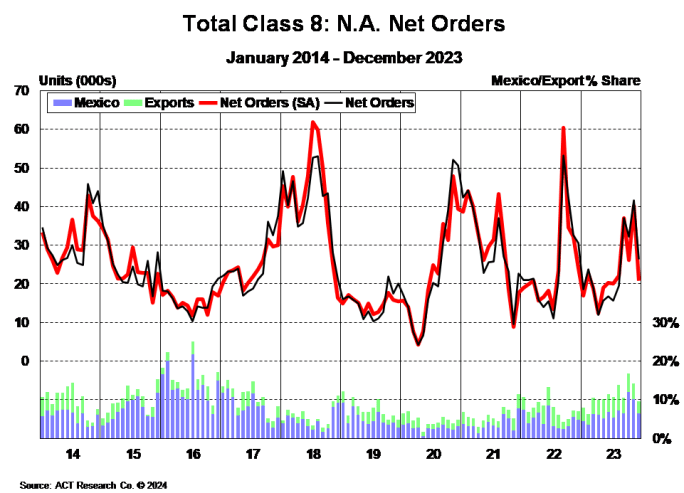

Vocational Market Leads Class 8 Truck Orders

December net orders for Class 8 trucks, at 26,352 units, were down 14% year over year, according to ACT Research. Tractor orders were down 31%, but vocational equipment orders were up 71% from a year earlier.

“For freight-related tractors, the decline in orders may hint at private fleet demand starting to diminish, which would be welcome news for spot rates, said Kenny Vieth, ACT president and senior analyst. “At the other end of the spectrum, vocational equipment orders remain strong as pent-up demand continues.”

December net orders for Class 8 trucks, at 26,352 units, were down 14% year over year, according to ACT Research. Vocational truck orders bucked the trend.

Source: ACT Research

Vieth also said truck production in December was higher than planned, which ACT believes are primarily attributable to a California prebuy ahead of California Air Resources Board regulations that started Jan. 1.

That could mean lower truck sales in the first quarter, he said.

“Weakening sales trend in a period of still-strong production suggests the potential for a rapid inventory escalation in Q1 as we enter the weakest period of the year for sales.”

Used-truck retail sales volumes jumped 22% month over month in December, significantly more than normal seasonality would suggest, according to ACT Research. Steve Tam, ACT vice president, explained, “December sales are historically close to average and see an eight-percentage point gain from November. Framed in that context, used truck demand seems solid.”

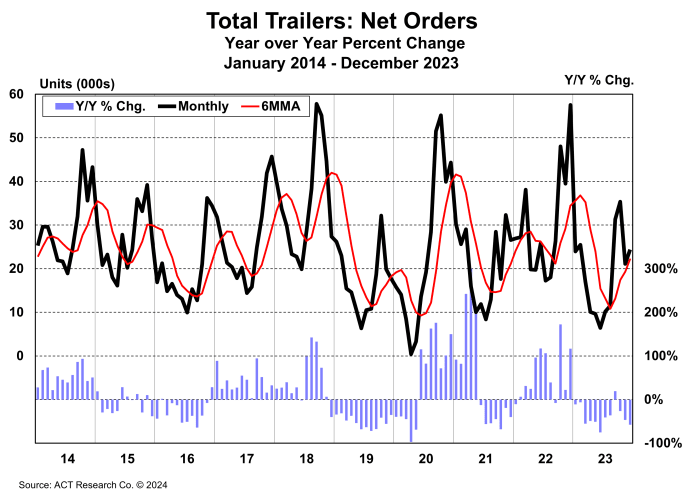

Trailer Market: 'Hoping and Coping'?

ACT Research also reported that December net orders of trailers, at 24,300 units, were nearly 58% lower than a year ago, but 3,300 units more than were booked in November.

For the trailer market, "the 2024 game plan is more about hoping and coping than full steam ahead,” said ACT Research.

Source: ACT Research

“With freight markets continuing their bounce along the bottom, carrier profits at a low ebb, and pent-up demand exhausted, the 2024 game plan is more about hoping and coping than full steam ahead for the trailer market,” said ACT in a news release.

“With 35% of the year’s orders historically booked in Q4, the quarter’s seasonal factors run roughshod on the nominal data,” said Jennifer McNealy, director–CV Market Research & Publications at ACT Research.

However, industry analysts at FTR pointed out that while the number of trailers ordered over the last 12 months fell to just above 243,000 units, the end of the year was looking up. December U.S. trailer net orders rose 10% over November to 23,434 units — 16% above the monthly average for 2023. Average monthly build for trailers is still healthy at more than 26,600 units.

Eric Starks, FTR chairman, said the “overall picture is still of an industry that is continuing its move towards a pre-pandemic level of stability."

More Fleet Management

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →

July Imports Poised to Set Container Record

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

Read More →

HDT Announces 2026 Truck Fleet Innovator Finalists

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Read More →