Costello: What it Will Take to Get Freight Back in Balance

If the pandemic-triggered boom times were the party, what we’ve been experiencing for the past year is the hangover, said Bob Costello, American Trucking Associations chief economist, in a session at ATA’s management conference in Austin this week.

ATA Chief Economist Bob Costello speaking at the assoociation's annual management conference.

Photo: Deborah Lockridge

If the pandemic-triggered boom times were the party, what we’ve been experiencing for the past year is the hangover, said Bob Costello, American Trucking Associations chief economist, in a session at ATA’s management conference in Austin, Texas, this week.

“We are going to continue to see more supply leave this industry, and even though demand is not going to pick up much, I think come a quarter, a couple of quarters from now, things are going to start to feel a little better for you. Not 2021, by no stretch… but all the evidence, both macro as well as industry-specific, points to, things are going to get better for our industry.”

However, it’s going to be painful to get there for parts of the industry, especially fleets that depend on the spot market, because in order for the industry to get back into balance, excess capacity must exit the market.

The Macro Economy

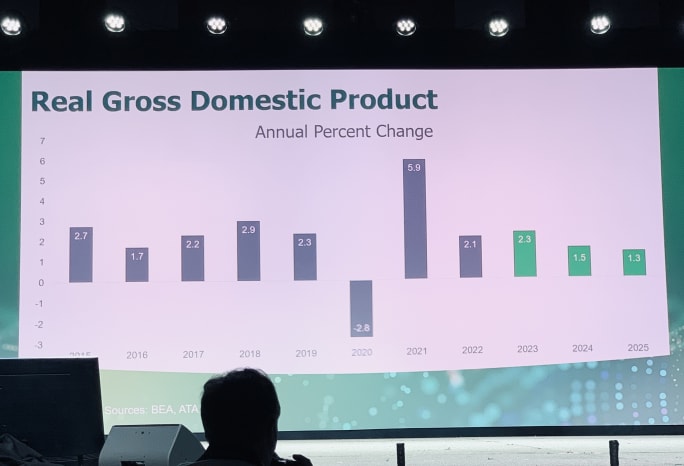

Looking at real Gross Domestic Product (GDP adjusted for inflation), Costello said, over the long run the U.S. sees an average 2% growth. But in 2021 we almost had 6% growth. The government pumped trillions of dollars into the economy.

“I’ll call that the party,” he said. “Now is the hangover. We’re going to revert to the mean and see slower economic growth.”

Because that party also led in part to high inflation, the Federal Reserve has implemented the most aggressive monetary policy in 40 years to try to curb it.

Costello said he’s been waiting for a recession (as a great many economic watchers have), but so far it hasn’t happened, and at this point if it does, it’s likely to be mild.

Real GDP is slow but we're not in a recession.

Photo: Deborah Lockridge

Looking at inflation, Costello said he doesn’t believe the Fed is going to be able to bring inflation down to its 2% target. “I think we ultimately are going to settle at a higher rate than we’ve been used to, 2.5 to 3% a year, because of the labor market.”

Wages have risen as companies struggle to find workers, and that’s affecting inflation. He doesn’t see that trend reversing because of demographic trends.

“We simply don’t have enough population growth, which ultimately will keep the labor market tighter,” he said. “We’re not having enough kids and not enough people coming to this country legally to live and work” to support the kind of population growth we’ve had isn the past.

Goods vs. Services

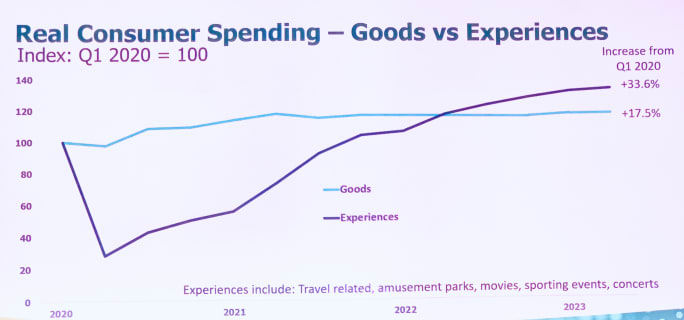

When looking at the economic environment for freight, however, GDP doesn’t tell the whole story, because it includes both goods and services. Goods mean more freight moves than services do.

So looking at the goods side of the economy, Costello shared some numbers on the three major areas that affect trucking freight: Consumer goods, construction, and factory/industrial production.

The pandemic created a freight boom when consumers couldn't spend money on experiences.

Photo: Deborah Lockridge

Consumer spending got out of whack during the pandemic, because people weren’t spending on services, such as vacations, concerts, and eating out. Instead, they poured money into goods, taking on home remodeling projects, for instance, buying new appliances and furniture.

When consumers were able to spend on services again, that spending shifted, and that shift was a big part of what caused the freight recession.

A lot of the Covid-19 relief money from the government went into savings. The population accumulated excess savings of $2.1 trillion. “They have not worked that completely off,” Costello said.

“The good news is households are still pretty good financially. The delinquency rate on loans is still low from a historical perspective. But there’s no extra oomph in spending coming.”

That means spending on goods will be below par for the near future.

Another economic indicator that is important for freight is the inventory to sales ratio. Freight was so good during the pandemic because inventories were so lean, and the supply chain got scrambled, eventually leading to inventories that were too high. As retailers have worked down those inventories, there was less freight to haul.

The good news, Costello said, is inventories appear to be getting back closer to normal. Some big-box retailers have publicly announced that they have inventories back down where they want them.

“There’s still some to go,” he said. “When inventories are in good shape, I think freight will start to feel better.”

Construction and Industrial

The Fed’s aggressive raising of interest rates to curb inflation has affected home building and existing home sales, as mortgage rates make it harder or less attractive to buy a house.

This year we are going to see housing starts fall almost 9%, Costello said, and existing-home sales are down 17%.

Non-residential construction, however, is a different story, up 15% this year, although he expects it to drop back to more normal levels the next couple of years.

A lot of this is infrastructure, Costello said, thanks to a boost from federal infrastructure spending. But it’s also building factories, including new types of factories like semiconductors.

And that ties into the factory and industrial indicators.

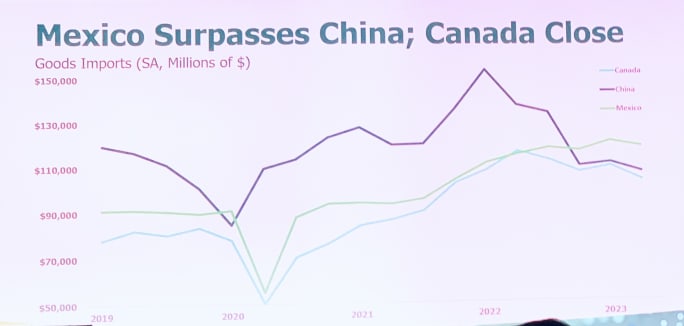

Resshoring and nearshoring are helping the demand side of the freight economy.

Photo: Deborah Lockridge

“I am very bullish on North American manufacturing,” Costello said. “This idea of nearshoring, reshoring, it’s real, it is happening. It doesn’t happen overnight but we know it’s happening.

“Mexico is now the U.S.’ largest trading partner, not China,” he said, noting that we’ve had two administrations, one Republican and one Democrat, pushing policies to make this happen.

He pointed out that while truckload volumes are down 3, 4, 5% year over year, truckloads coming in from Mexico are up 2.3Z% this year.

Trucking Indicators

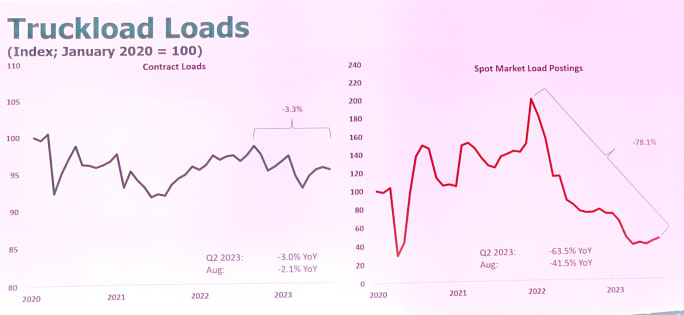

The pandemic-induced freight boom spurred a red-hot spot market, with the spt market doubling in size and rates hitting record highs as shippers who were trying to get their goods to market had to turn to the spot market when regular contract carriers couldn’t provide the extra capacity.

Costello recalled having dinner with the head of truck transportation for a large shipper in the Fall of 2021. Before the pandemic, this shipper moved no more than 2% of its loads in the spot market. At that point in the Fall of 2021, they were at 21%.

But what goes up must come down and as the economy slowed, there was no longer all that excess freight fighting for capacity. The spot market has plummeted 78% from its peak.

Contract freight, in contrast, is down 2 or 3%. A freight recession, to be sure, but not nearly as bad as the spot rates.

Carriers that rely on the spot market for the bulk of their freight, “those are the companies in trouble.”

Carriers that don't depend as much on the spot market are doing better than those that do.

Photo: Deborah Lockridge

Capacity: ‘This is Not a Demand-Side Story.’

“Any turnaround in the marketplace is going to be supply driven,” Costello said. There’s too many trucks chasing the freight, resulting in an overcapacity situation and a freight recession.

He believes that capacity is going to tighten, as lower rates and higher cost pressures drive some carriers out of business.

During the boom of the pandemic, many drivers and owner-operators left the fleets they were working for, getting their operating authority to cash in on the spot market. With the collapse of that hot spot market, many of those new carriers are struggling to survive, he said.

Fuel prices will drive some overcapacity out of the industry.

Photo: Deborah Lockridge

At the same time they’re faced with less revenue, they are dealing with cost pressures, including higher wages (“we’ve seen the largest cumulative increase in driver pay we’ve ever seen”) and fuel prices (“I think this is the catalyst to driving capacity out of the industry.”)

On top of that, many of those newly minted fleets bought used trucks and trailers at very high prices. “I know some of you were selling used equipment for nearly what you paid for it,” Costello told the audience. Those used-truck values have since dropped.

In short, “There’s going to be more and more folks going out of business,” Costello said. Carrier failures will continue, bringing supply and demand closer to balance.

“I hate saying it; other people’s pain is our gain. But it needs to happen and it is in fact happening.”

More Fleet Management

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →

July Imports Poised to Set Container Record

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

Read More →

HDT Announces 2026 Truck Fleet Innovator Finalists

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Read More →

Van Spot Rates Top Contract Rates for First Time Since 2022

There’s more good economic news for the North American trucking industry according to the latest Truckload Volume Index report from DAT.

Read More →

Carrier Transicold Extends Refrigerated Trailer Life

Fleet Refresh enables refrigerated fleets to replace aging transport refrigeration units instead of entire trailers, while adding Lynx Fleet telematics and BluEdge service coverage.

Read More →