Freight Recession: Signs of Improvement?

The freight recession continues to bump along the bottom, with the spot market continuing to be battered by overcapacity amidst freight demand that is somewhat improved but still soft.

The American Trucking Associations' For-Hire Tonnage Index includes truckload and LTL freight, but very little spot-market freight.

Source: American Trucking Associations

The freight recession continues to bump along the bottom, with the spot market continuing to be battered by overcapacity amidst freight demand that is somewhat improved but still soft, according to recent reports from economic analysts at ACT, FTR, and the American Trucking Associations.

“After hitting a floor in April, tonnage has slowly and inconsistently improved, but remains 3% below its recent peak in September 2022,” said ATA Chief Economist Bob Costello.

ATA’s seasonally adjusted For-Hire Truck Tonnage Index increased 1.1% in October after declining 1.1% in September. The October index was 115.2 (2015=100) compared with 113.9 in September.

“Despite the monthly gain, truck freight remains soft as it continues to contract on a year-over-year basis,” Costello said.

ATA calculates the tonnage index based on surveys from its membership, including both truckload and less-than-truckload. Costello emphasized that the index is dominated by contract freight, with minimal amounts of spot market loads.

“The traditional spot market remains much weaker than contract tonnage,” he said.

Are We There Yet?

ACT Research said expectations are for freight markets to continue bouncing along the bottom in the near term, with some holiday volatility and a change in trajectory on the way next year.

They believe retail sales will improve following a year of declines.

“The acceleration in real disposable income growth as inflation slowed sharply this year, and the ongoing strong labor market, support a recovery in goods demand,” said Tim Denoyer, ACT Research VP and senior analyst. “The end of destocking, rise in imports, and recent easing in oil prices improve our confidence that peak season will end on a higher note for freight demand.

“With freight volumes broadly starting to pick up, the spot market is still loose heading into winter, but we expect the trajectory of rates to shift in 2024,” Denoyer said.

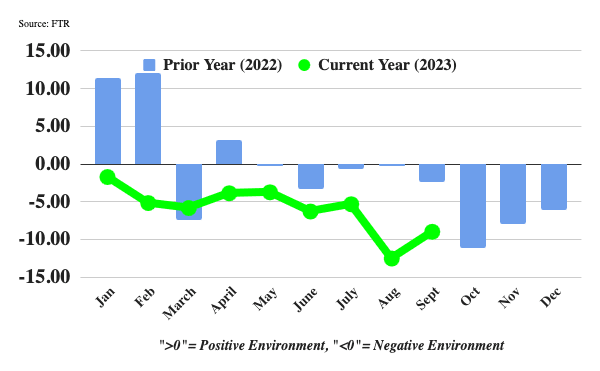

FTR's Trucking Conditions Index is still in the negative but could be starting to head in the right direction.

Source: FTR

FTR’s Trucking Conditions Index in September improved to -8.97 from August’s -12.54, thanks to more stable fuel prices and modestly stronger freight demand. However, FTR analysts say market conditions remain quite tough for carriers and the outlook is for consistently negative readings for the TCI into late 2024.

The TCI tracks the changes representing freight volumes, freight rates, fleet capacity, fuel prices, and financing costs, and combines them into a single index indicating the industry’s overall health. A positive score represents good, optimistic conditions. A negative score represents bad, pessimistic conditions.

“Although carriers today are seeing some temporary relief due to the recent drop in diesel prices, freight rates look to improve only gradually over the next year,” said Avery Vise, FTR’s vice president of trucking.

The Capacity Problem

Why? Better freight volumes likely won’t be enough on their own. There’s still too much capacity chasing too little freight.

Spot load postings remain low, and while spot equipment posts have declined, the rebalancing of capacity is making little net progress with the industry still adding capacity, according to ACT Research.

“The trucking industry continues to struggle with more capacity than is ideal given sluggish freight volume,” said FTR’s Vise. “Many operations apparently are hanging on or maintaining driver levels in hopes of a near-term rebound, but that approach amounts to an increasingly high stakes game of chicken.”

Data from Truckstop and FTR for the week ended Nov. 17 show a spot market that did not experience its typical rate strength during the week before Thanksgiving. Broker-posted dry van spot rates were down during the week and refrigerated spot rates were essentially flat.

Spot rates for both equipment types typically rise significantly during the week before Thanksgiving; refrigerated rates occasionally surge 10 cents or more heading into one of the biggest food-centric holidays of the year.

“Capacity shortfalls during Thanksgiving week usually mean higher dry van spot rates, but weakness in the latest week raises doubts about that outcome,” according to FTR.

Private fleet capacity expansion continues to pull freight from the for-hire market, said ACT’s Denoyer, but “we think equipment purchasing patterns are changing, which should propel the freight cycle forward in 2024.”

“For carriers, the long bottom in freight rates continues, with spot rates little changed since April,” said Kenny Vieth, ACT president and senior analyst. “A big driver of rate weakness has been lagged private fleet capacity additions. As for-hire fleets tend to be the first buyers in line, private fleets have been the drivers of Class 8 market strength in 2023, adding equipment at the bottom of the cycle and prolonging the rate pain.”

Denoyer said slowing Class 8 tractor sales means fewer new additions to capacity, and the pace of fleet exits remains historically elevated, so the removal of overcapacity is gaining momentum under the surface.

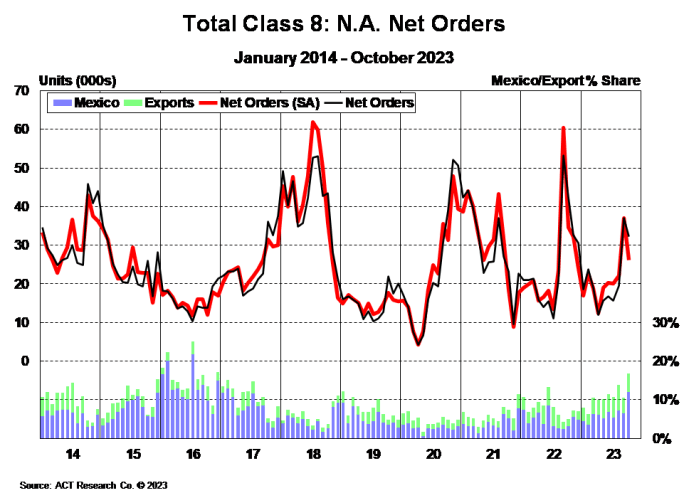

How is the Freight Recession Affecting Truck Orders?

While strong relative to freight market conditions, Class 8 orders were down 24% year over year in October, according to ACT Research. Final Class 8 net orders were 32,287 units in October, with the largest drivers of orders being market segments with lingering pent-up demand, according to ACT analysts.

October Class 8 orders were driven by demands for vocational and export trucks, according to ACT Research.

Source: ACT Research

ACT Research believes these numbers show several factors at work in 2024 that will drive greater Class 8 demand than might be expected given the overall freight recession, including:

Ongoing pent-up vocational truck demand. The vocational straight truck market saw orders rise 24% y/y in October.

Strong tractor demand in Mexico. Export market orders were up 91% y/y in October.

A healthy LTL market. Orders destined for the Mexican market were up a whopping 187% in October.

Supply chain integrity.

“One of the things staying our hand from deeper forecast cuts, in the face of weak freight fundamentals, has been a solid industry-wide start to ‘order season,’” Vieth said. “The last trimester of the year is the period in which the OEMs usually open their out-year order books, leading to a period of outsized orders that typically extends into March.”

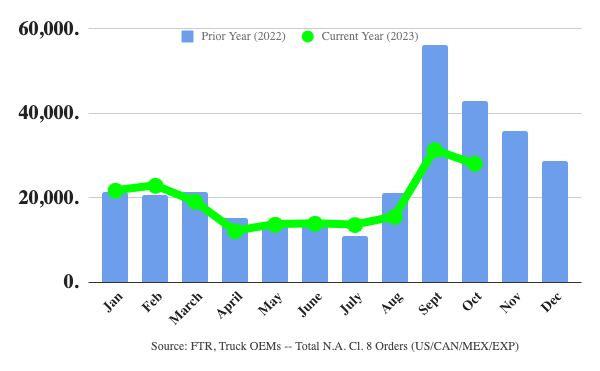

FTR said it expected the drop in Class 8 orders. Despite freight weakness, fleets continue to be willing to order new equipment, said FTR analysts.

Source: FTR

FTR’s preliminary Class 8 orders for October were lower than ACT’s at 28,000 units, down 10% from September and 35% from October 2022. FTR analysts said this was to be expected, given the weakness in freight transportation and the ongoing normalization of equipment markets following exceptional demand in 2022.

“Build slots continue to be filled at a healthy rate,” said Eric Starks, FTR chairman of the board. “We expected a year-over-year decrease in orders and were not surprised by the month-over-month easing, either. The overall picture for truck demand is steady. Despite freight weakness, fleets continue to be willing to order new equipment, affirming our expectations of replacement demand during 2024.”

Weak Spot Market Affects Dry Van Trailer Orders

ACT analysts expect both Class 8 and trailer orders to remain relatively the same in November, but it has pulled back its forecasts for dry van due to a recalibration of expectations regarding power-only brokerage.

“To accomplish the scheme of introducing drop-and-hook productivity into the small carrier spot market was a plan by large fleets and brokerages to boost trailer-to-tractor ratios, build trailer pools, etc., into the wildly growing pandemic stimulus and supply-chain constrained spot market,” explained Vieth.

But those spot market drivers are no longer the case, and that means lower trailer orders than once anticipated.

Peak order season for trailers opened in September, and October net orders continued to show strong bookings. However, cancellations in some segments remain elevated, despite healthy backlogs, according to ACT Research.

October net orders, at 35,300 units, were 26% higher year over year, ACT said, and 4,000 units more than were booked in September.

However, when seasonally adjusted, October’s orders fell to 26,200 units, and on that basis, instead of rising from September, orders decreased 9% month over month.

“While the last two months’ order intake is a positive sign, what we don’t yet know is for how long this level of deal closing will be sustained in the freight recession that is expected to linger into early 2024,” said Jennifer McNealy, director–CV Market Research & Publications at ACT Research.

“On balance, two solid months of orders are not enough for us to say ‘sunny skies ahead,’ particularly when freight markets continue their bounce along the bottom and carrier profits remain at a low ebb,” according to ACT’s State of the Industry: U.S. Trailers report.

More Fleet Management

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →

July Imports Poised to Set Container Record

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

Read More →

HDT Announces 2026 Truck Fleet Innovator Finalists

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Read More →

Van Spot Rates Top Contract Rates for First Time Since 2022

There’s more good economic news for the North American trucking industry according to the latest Truckload Volume Index report from DAT.

Read More →

Carrier Transicold Extends Refrigerated Trailer Life

Fleet Refresh enables refrigerated fleets to replace aging transport refrigeration units instead of entire trailers, while adding Lynx Fleet telematics and BluEdge service coverage.

Read More →