FTR Forecasts Only Incremental Freight Market Improvement in 2024

Avery Vise, FTR vice president of trucking, explained why the forecaster believes we'll see a sluggish freight economy for the near future.

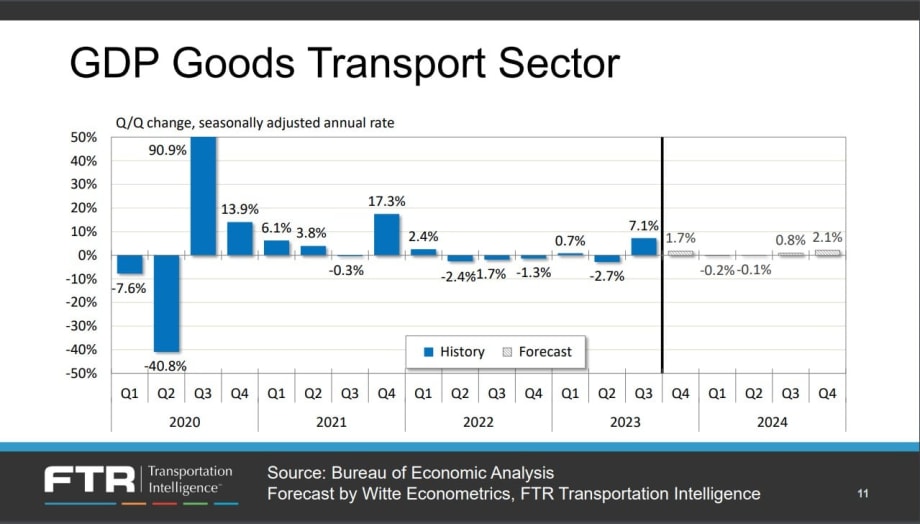

The goods transport sector is expected to grow 1.2% in 2024 and about 2% in 2025.

Source: FTR

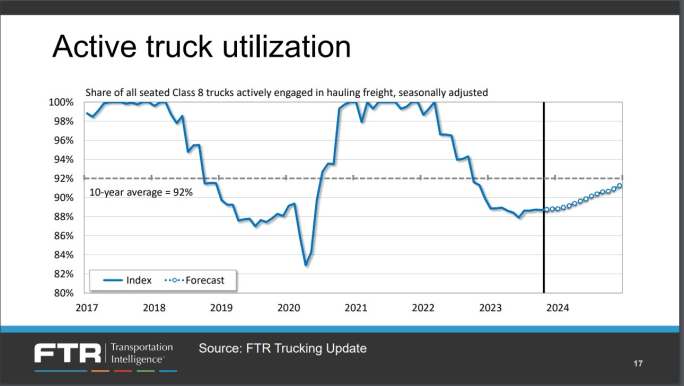

FTR forecasts incremental increases in truck utilization in 2024.

Source: FTR

FTR’s Avery Vise, vice president of trucking, provided an analysis of what 2024 holds in store for trucking, including how he expects only incremental improvements in both spot and contract rates. He also described the county’s industrial production for 2024 as “sluggish,” but noted consumer spending remains solid.

Economy and Consumption

Vise opened FTR’s webinar, Transportation Outlook – Transitioning to Growth in 2024, by saying one of the biggest issues that continues to confound everyone is what is happening with the consumer sector regarding consumption. He said consumer spending remains solid, but he expects continued growth and the economy is at record levels both in services and in goods spending.

The country is still not back to the trend line in inflation-adjusted spending on services, but it is above the trend line on goods adjusted for inflation. Both, he said, are pretty stable and not expected to change very much. Vise did say he thinks there will be changes over time in healthcare, noting that a lot of healthcare jobs are still being added.

“But I think the real issue that everyone’s focusing on is we have not seen a decline in spending,” Vise explained. "Spending... is actually at a record level in goods. It isn’t growing very much, but it’s holding steady.”

Household debt levels are holding steady, he said. The debt levels are not increasing as some have reported and are holding around pre-pandemic levels. But there is an increase in credit card delinquencies, he said. Personal savings rates are down also, according to Vise.

With all the economic concerns mentioned, Vise still said the current level of consumption can continue, absent some type of inflection event.

Goods Inventories Lean

In the wholesale sector, according to Vise, the inventories-to-sales ratio is at the same point as pre-pandemic levels. In the retail sector, excluding automotive, he said inventories were “actually quite lean.”

“In fact, they're the leanest on record, except for the period of pandemic disruption itself, which we would put at between mid-2020 through the end of 2021,” Vise said.

Lean inventories could mean a short-term increase in truck freight as businesses restock their inventory after the holiday shopping season.

Industrial Production

Vise predicts industrial production to decline in 2024 by nearly half a percent. Last year, 2023, saw just a slight increase of two-tenths of a percent.

He describes industrial production as “sluggish” and “not horrible, but not good.”

Gross Domestic Product

In taking a look at a broad measure of the economy, gross domestic product, Vise suggests that the GDP will grow about 2%, which he calls okay, but not great.

In the portion of the economy linked to freight — what FTR calls the GDP Goods Transport Sector — 2023 was flat, but data suggests there will be around 1.2% growth in 2024 and a little over 2% in 2025.

“That does not get you very much in terms of actual freight volumes. You really need to get to 2% or more before you really start to even notice it,” Vise said. “In the near term, it means a very sluggish freight economy.”

Once the final data is in for 2023, Vise anticipates it will confirm that truck loadings were flat for the year. Last year followed a 2% increase in 2022 and a 5% increase in 2021. For 2024, he suggests only about three-tenths of a percent increase.

The numbers have been pulled down by short-haul bulk freight, such as aggregates, which make up a large amount of tonnage as well as loadings, Vise explained.

Dry van last year was up half a percent, and for this year Vise said it will be up about 1%. Refrigerated was stronger last year and is anticipated to be stronger again this year. Flatbed was down yearly 1% last year and is expected to be down again this year.

Capacity: The Elephant in the Room

“Let's go on and talk about the elephant in the room, which is capacity, because that's really where things are going to change likely in the coming year, as we don't see a lot of reason to expect a big increase or decrease in freight volume," Vise said.

FTR closely tracks what goes on with the motor carrier population, and we have been seeing a reversal over the past year in new carrier creation seen in mid-2020 through late 2022. In the fourth quarter, there was the largest decrease in carrier population ever, according to Vise. However, the industry still has about 100,000 carriers more now than before the pandemic.

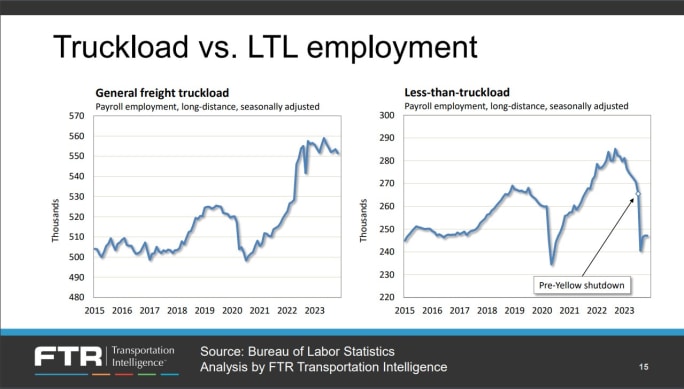

At the same time, general freight truckload is still holding up very high, and truckload employment is at almost record levels, Vise pointed out.

Since Yellow’s closure, less-than-truckload has added back some capacity, but not much, he added. He pointed to how LTL is closely tied to industrial production, which he says will remain relatively flat. A lot of Yellow’s assets are still working their way through being repurposed, he said. The employment situation in LTL is still a little constrained by physical assets. That will work its way through, according to Vise.

“Obviously, there's another element involved, and that is the fact that the Yellow drivers were unionized and how that’s going to play out for the other carriers, most of which are non-union,” said Vise.

There are about 16% more drivers in the market now than before the pandemic.

Source: FTR

There are about 16% more drivers in the market now than before the pandemic when looking at the employment numbers for general freight truckload, Vise said.

“That really puts us in a situation where we clearly do not have a shortage of drivers overall in the market,” he explained. “That’s not to say that we’re not going to be once again, within the next couple of years, back into the same tight labor market that we’ve always seem to be in, but we’re not there right now.”

FTR looks at FMCSA new carrier data and BLS data when considering capacity, and Vise noticed an early increase in smaller carriers and little growth among large carriers. However, that trend has shifted, and now smaller carriers are relatively flat, and larger carriers are increasing.

FTR reports the industry has about 100,000 more carriers now than before the pandemic.

Source: FTR

Active Truck Utilization

Vise explained active truck utilization is the number of Class 8 trucks needed to haul the freight divided by the number of active trucks. Truck utilization, he said, was massively stressed in 2021, in a similar fashion to late 2017 into early 2018. Where the industry is now is more comparable to 2019 – a little bit stronger, but not significantly, he said.

“As we look ahead, though, the more important issue is that we’re not really recovering very quickly,” Vise said. “It is going to be very incremental increase in utilization as we progress through the year.”

Even by the end of the year, it is not likely truck utilization will be back to the 10-year average estimate of 92%, he said.

He said the biggest question is if the industry will continue to lose more capacity than what has been lost to this point and if there be an acceleration of that.

Rates

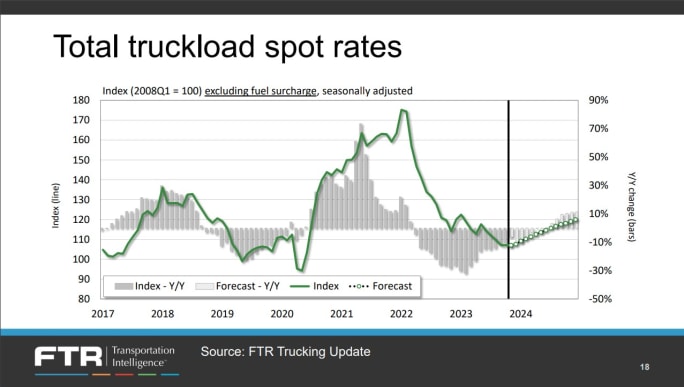

“Obviously, spot rates have had a wild swing over the last few years. They were down nearly 19%, year over year last year, that was after being down nearly 16% in 2022, surging about 28%. In 2021,” explained Vise.

“We don’t think we’re past the bottom,” he added.

Spot rates have seen wild swings in recent years.

Source: FTR

He said on a seasonally adjusted basis, FTR sees only incremental improvement over the next year. Rates will likely run a negative year over year comparison, probably until the middle of the year. Then, after the middle of the year, he believes spot rates will start to increase and begin running positive year over year, but not in a way that will greatly change the market.

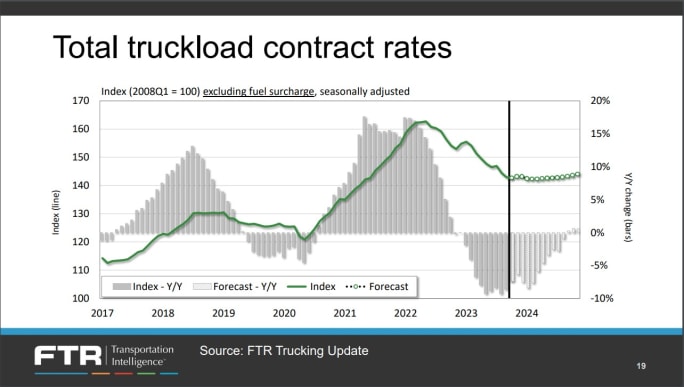

Contract rates were up about 13% in 2021, up more than 7% in 2022, and down about 7% in 2023.

FTR expects contract rates to be down about 3% this year, mostly due to early-year comparisons. Near the end of the year, Vise said he expects to see rates increase a little when compared year over year.

Contract rates are forecast to be down slightly in 2024.

Source: FTR

More Fleet Management

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →

July Imports Poised to Set Container Record

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

Read More →

HDT Announces 2026 Truck Fleet Innovator Finalists

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Read More →