More from Avery Vise:

Were Job Growth and Retail Sales Weak in December? It’s Complicated

Surging Inventories Bolster Freight Economy

Retail inventories surged to end 2021. FTR's Avery Vise explores why it happened and what it means for freight.

by Avery Vise, FTR

March 1, 2022

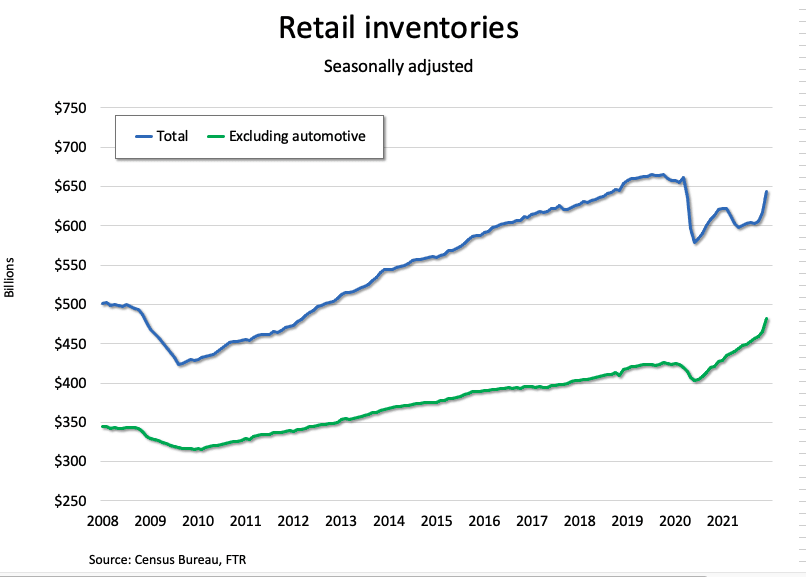

An increase in automotive inventories helped pad the numbers, but retail inventory growth in December was a record even without the auto industry’s help.

Graph: FTR

3 min to read

The U.S. economy in the fourth quarter of 2021 posted its strongest growth since the rebound from lockdowns in the third quarter of 2020. Gross Domestic Product (GDP) rose 6.9% quarter over quarter on a seasonally adjusted annualized basis.

The portion of the economy linked to freight — what FTR calls the GDP Goods Transport Sector — also saw a big gain in the fourth quarter, jumping 15.4% on an annualized basis. The increase was the largest in two years.

Retail inventories surged to end 2021, and inventories represented more than half of the fourth-quarter growth in both GDP and GDP Goods Transport. Seasonally adjusted retail inventories rose 4.4%, which is the largest gain for a single month since the Census Bureau began tracking the data in 1992. The increase followed a 2% gain in November, the third largest monthly increase on record.

As recently as October, total retail inventories were running nearly 8% below pre-pandemic levels. As of December, that deficit is less than 2%.

The automotive industry, slammed by a shortage of semiconductors, has been the principal drag on retail inventories for about a year. Excluding motor vehicles and parts, retail inventories have been outpacing the pre-pandemic norm since late 2020. However, December brought a record increase of 6.8% in retail inventories of motor vehicles and parts. November was no slouch either, with a 4.2% gain, the fourth largest on record.

Automotive certainly helped pad the numbers, but retail inventory growth in December was a record even without the auto industry’s help. Excluding automotive, retail inventories rose 3.6% — the strongest gain on record. As of October, inventories excluding motor vehicles and parts were already running about 8% ahead of February 2020, seasonally adjusted. By year-end, they were nearly 14% above pre-pandemic levels.

Census Bureau data on inventories is expressed in dollars and is not adjusted for inflation, so some of the recent gains could reflect higher prices. However, adjusting for inflation would not change the fundamental picture of sharply increased inventories on a unit basis.

What Inventories Mean for Freight

What does a surge in inventories mean for freight? Normally, rising inventories are great for freight volume in the here and now but a concern for the future. If inventories rise, the near-term demand for inventory replenishment typically wanes. However, this conventional wisdom might not hold during the pandemic economy.

One unusual factor is the extraordinary strength of consumer spending on goods. Retail sales on a not-seasonally-adjusted basis were the strongest ever in December. Strong retail sales have kept inventories very lean relative to sales, so we don’t expect an immediate decline in inventory replenishment.

If consumer spending drops significantly, however, we might see an inventory correction. Reduced consumer spending alone would mean weaker freight, but an inventory correction would compound the dynamic.

We do not forecast a collapse in consumer spending, but it’s possible, given inflation, fading stimulus, stock market volatility, and the sheer amount of stuff — including long-lasting durable goods — consumers already purchased over the past 18 months or so.

Supply chain disruptions also complicate things. For example, it is possible that some of the inventory build in late 2021 reflects seasonal products that did not make it to market in time for the holidays due to congestion at U.S. ports or other factors. If so, much of that inventory might not be relevant to an analysis of how rising inventories affect replenishment rates.

The inventory situation clearly bodes at least one upside for freight. Even with the gains late in 2021, inventories of motor vehicles and parts are still down about 30% from February 2020. Even if vehicle sales falter somewhat, the auto industry will still need to build as many vehicles as the supply of semiconductors allows just to get inventories back to comfortable levels. Also, depleted inventories probably are responsible for much of the recent weakness in vehicle sales, so the auto industry could be looking at months or perhaps even years of high production levels — if it can get the components it needs.

Subscribe to Our Newsletter

More Fleet Management

HDT Announces 2026 Truck Fleet Innovator Finalists

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Read More →

Van Spot Rates Top Contract Rates for First Time Since 2022

There’s more good economic news for the North American trucking industry according to the latest Truckload Volume Index report from DAT.

Read More →

Carrier Transicold Extends Refrigerated Trailer Life

Fleet Refresh enables refrigerated fleets to replace aging transport refrigeration units instead of entire trailers, while adding Lynx Fleet telematics and BluEdge service coverage.

Read More →

FTR Says Freight Rates Surged in May

FTR's Trucking Conditions Index surged to a record high in May, the analytics firm reports.

Read More →

Meet HDT's Truck Fleet Innovators at Heavy Duty Trucking Exchange

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for HDTX, September 23-25.

Read More →

Sponsored•July 1, 2026

Enhance Fleet Performance with High-Efficiency Auxiliary Power Units

Drive sustainable cost savings while increasing driver comfort during short- and long-haul logistics operations.

Read More →

Sponsored•June 30, 2026

Is Your Parts Procurement Process Reactive or Proactive?

Ready to revamp your parts procurement process? Learn how now with “Strategic Parts Purchasing: A Process Checklist”

Read More →

What Trucking Events are Happening in 2026?

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

Truckload Rates Keep Rising as Tight Capacity Fuels Freight Market Recovery

Spot and contract rates continued climbing in May and June, not because freight demand is surging, but because fewer trucks and drivers are available.

Read More →

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →