Related: What’s Behind Recent High-Profile Trucking Closures?

Are We In a Truck Recession?

First-quarter 2019 GDP grew at 3.2%, and the latest guess about the second quarter is 1.7%. That latter number is a disappointment for sure, but it is not a negative, says longtime trucking economic analyst Noel Perry. But what about freight?

by Noël Perry, Trucktop.com

August 5, 2019

Source: Trucktop.com

5 min to read

Whether or not we are in a truck recessoion is a matter of fact and a matter of perspective. Let’s deal with the facts first. Economists loosely define a recession as two consecutive quarters of GDP growth of less than zero. For the six quarters beginning in 2008, we had five when GDP shrunk. That’s a recession! This year, first-quarter GDP grew at 3.2%, and the latest guess about the second quarter is 1.7%. That latter number is a disappointment for sure, but it is not a negative. No economic recession here.

But what about freight? That’s a good question. Sometimes freight goes negative even when GDP is positive. In 2001, there was no “official” recession, but freight shrunk each quarter. Is that happening now?

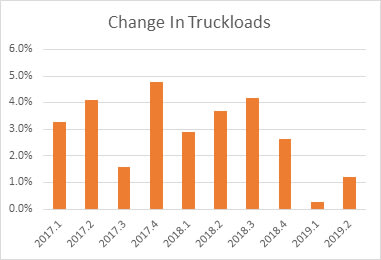

Looking at the quarterly numbers in truckloads from the last two years, all are positives – although the last two quarters are well down. I said above that recession can be a matter of perspective. If one is used to freight growth of 2 or 3%, two quarters of growth less than 2% may feel like recession.

Does this mean that capacity utilization is getting soft? We are fortunate to have very up-to-date information on the spot market, itself a significant space. It also has value as a leading indicator for the whole truckload market.

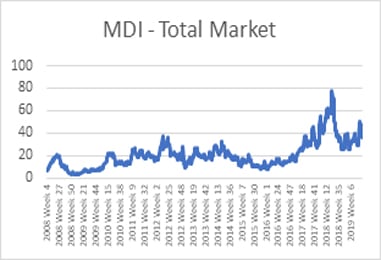

In the next chart, you can see the data from the Truckstop.com MDI measurement (loads posted/trucks posted).

Source: Trucktop.com

This historical data shows us that a bad recession, like 2008-2009, produces numbers below 10, while a soft spot like we had in 2015-2016 produces numbers around 10. Currently, we are above 30. That is certainly weaker than the peak of a year ago, but it is decidedly not recessionary.

The contract price data tells us the same thing. We measure rates compared to their long-term trend to understand the dynamics of any individual year. Rates have risen a little each year since 2003, so one has to factor that trend out before you can understand the short term dynamic. Although the current value is down two percentage points in the last two quarters, it is still a robust 5% above trend. In previous recessions, it fell to 5 or 10% below trend.

While shippers are pleased that the peak is past, they are definitely not enjoying recessionary contract rates. While we expect contract rates to steadily move back towards trend, they do not indicate recession.

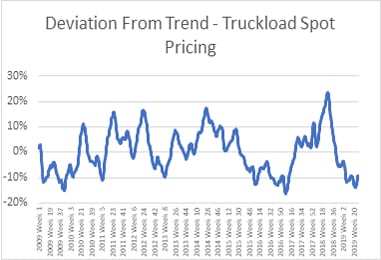

The story with spot rates is more nuanced. With spot rates, it is as if the facts were a matter of perspective. We have, again, the data from Truckstop.com to thank for the facts. They appear again as deviations from the underlying trend.

A “0” on the graph is ‘normal’. You can easily see the peak of the recent capacity spike at 20% above trend. Ominously, the latest data is 10% below trend – and this is the important finding. It is in the same rough range as during the 2009 recession and the weak spot in 2016. We know from the fact above that neither this event nor the 2015-16 event qualified as a recession by other perspectives. Still, this data suggests that spot prices are at or nearing recessional levels.

Source: Trucktop.com

We thus have factual evidence full of contradictions that beg for insight. I suggest three possibilities: First, this may simply be a temporary reaction to the shock of falling so quickly from the high place of a year ago. The latest data show rising spot prices; maybe we are on a rebound towards normal. Second, and ominously, this data may be the canary in the coal mine that indicates a real economic or freight recession to follow. That did not happen with spot prices before 2008 – quite the reverse. However, this one bears watching.

Third, maybe it just “shy” pricing. Finally, this data provides evidence of what I have long called “shy” trucking pricing. Despite the extraordinary value provided by American truckers and the growing difficulty of acquiring sufficient capacity, truckers are dangerously dependent on emotion with their pricing. When events, as in 2004, 2014, and 2018, provide emotional cover, prices move up rapidly. But with the first signs of trouble, truckers usually give back much of their gains. So, rather than a gradual, well-managed return to normal from the 2018 peak, enough people have panicked at the softening market conditions to drive pricing to “recessionary” levels – despite the absence of recessionary conditions.

Horray for big data! It's important to note that in the 2004-2008 cycle, when we now know the same things happened as with today, we had great difficulty figuring out what was going on until six to nine months after the events occurred. In 2019, using Truckstop.com data, we have weekly updates on a variety of market conditions down to the specific lane detail. This should enable a variety of industry participants to follow development closely and to respond more quickly and more effectively to the volatile events of our markets.

We urge you to invest more time in such analysis, recognizing that it is not some abstract evidence of far-off events, but rather tangible evidence of what is happening in your markets.

Editor’s Note: Noël Perry is chief economist at Truckstop.com and owner of Transport Futures. He follows all aspects of transportation, including strategy, market sizing, operations, technology, modal competition, pricing, regulation, and public policy. This article was authored under the guidance and editorial standards of HDT’s editors to provide useful information to our readers.

Subscribe to Our Newsletter

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →