Trucking Industry Hits the Doldrums with Neutral Economic Outlook

Decreasing freight rates, sluggish demand and slow truck orders are all signs of a trucking industry that has finally hit the brakes on the 2018 economic boom.

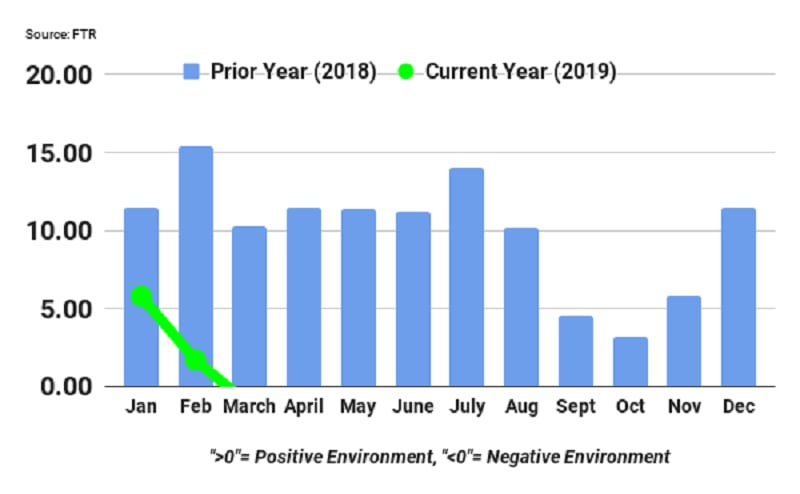

FTR’s Trucking Conditions Index for March showed its first negative reading in several years, reflecting a softening environment for carriers.

Source: FTR

FTR’s Trucking Conditions Index for March showed its first negative reading in several years, reflecting a softening environment for carriers.

The March TCI reading fell to -1.18 driven by easing freight rates and sluggish, though still positive, demand. Active truck utilization and the truckload rate have also continued to ease. The weakness in truckload rates was attributed mostly to spot rates, but FTR also found that the contract rate outlook has turned slightly negative.

FTR’s outlook for loadings growth has been revised downward from previous forecasts with year-over-year growth now expected to be under 2%.

“The trucking industry has essentially returned to neutral conditions as deterioration in most market factors are offsetting continued solid, but not robust, freight demand,” said Avery Vise, vice president of trucking for FTR. “We generally expect this balance to continue into 2020, but TCI readings could turn positive or negative month to month based on relatively minor shifts in demand, utilization, rates, or costs.”

This trend was also spotted by analysts at ACT Research who noted in the May Freight Forecast that slowing freight and increased tractor sales will likely have a downward effect on freight rates.

“Freight remains soft, as expected, and while we see reasons for recovery in the second half of 2019, escalating trade tensions raise the risk of freight recession,” said Tim Denoyer, ACT Research’s vice president and senior analyst. “Class 8 tractor retail sales are on fire, adding capacity to the market at an unfortunate time for truckers. Shippers are increasingly targeting freight cost savings, likely emboldened by attractive rates in the spot market.”

ACT Research found that dry van truckload spot rates and net fuel have fallen nearly 19% year-over-year in April and more than 3% from March, twice the historical average seasonal drop for April.

While new trucks may be selling well, Class 8 truck orders continued at a snail’s pace. In April, FTR tracked truck orders at just 16,400 units for the month, 52% below April 2018’s numbers.

While orders are low, that doesn’t mean the demand is not. Fleets are continuing to search for open build slots in the 2019 production schedule, according to FTR. Backlogs are fluid with orders being rescheduled, often opening up build slots in the near term. FTR expects this pattern to continue until ordering for 2020 begins.

“Economic growth is expected to moderate soon, slowing down the freight markets,” said Don Ake, FTR vice president of commercial vehicles. “However, currently there is still a need to replace older trucks and also get more new trucks on the road.”

Medium-duty Class 5-7 truck orders continued on at a positive rate, benefiting from underlying strength in the consumer economy, according to ACT Research. ACT tracked 23,100 Class 5-7 truck orders for April, down just 6.8% from the previous year and up 12% from March.

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →