The Shifting World of Aftermarket Parts

How e-commerce, consolidation, new competition, and technology and integration are changing the aftermarket.

How e-commerce, consolidation, new competition, and technology and integration are changing the aftermarket.

So much of the news in the trucking industry lately is about the vehicle or the supply chain. Will trucks be autonomous? Will electric power replace internal combustion engines? What will be the impact of blockchain on the delivery of goods? What about last-mile delivery?

Not being talked about as much is what’s going on in parts distribution. Yet there are a variety of significant factors at work that are changing — or soon will change — the face of truck parts distribution.

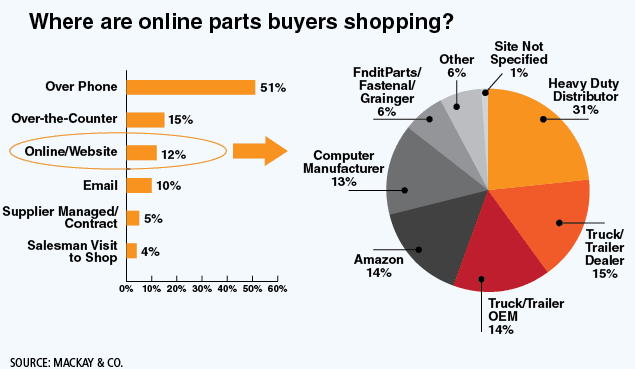

Online parts sales may never completely replace the role of local parts dealers/distributors, but the digital channel is growing in popularity, especially with millennials.

Source: Mackay

The continued growth of e-commerce

There is no denying the impact e-commerce has had on all our lives. “We certainly have seen retail sales via e-commerce as a percentage of GDP on a very healthy growth trajectory,” says Steve Tam, vice president of market research and analysis firm ACT Research. He explains that if you include food and services, about 10% of all retail sales are made through e-commerce.

Moving specifically to the trucking industry, Jim Pennig, vice president of business development for Vipar Heavy Duty, says, “The heavy-duty aftermarket is behind when it comes to e-commerce, but we are seeing a lot of momentum to move into it more aggressively.” In fact, Vipar has seen a 50% improvement since the beginning of the year for online parts sales through its members’ e-commerce platforms.

Aftermarket research firm MacKay & Co. found in a recent survey that fleets ordered 12% of their parts online. John Blodgett, vice president of sales and marketing, reports that survey respondents also indicated they expect online parts purchases to increase to 15% of total purchases in the next three years. (See graph on opposite page.) Interestingly, 31% of those parts were purchased through a heavy-duty distributors’ website, with Amazon seeing 14% of total online parts purchases from the surveyed fleets. (See graph on page 48.)

According to Bill Wade, managing partner of consulting firm Wade & Partners, more than $6 million of heavy-duty parts are bought online each year.

Dave Seewack, founder and CEO of FinditParts, an online truck parts marketplace, says the company is seeing 100% sales growth year-over-year, but declined to quote specific numbers. “Our customers are coming back and buying more frequently, and more fleets seem to be getting comfortable with the process of buying online.” He explains that fleets initially used the site for hard-to-find parts, but today “they are using it more frequently for more SKUs.” He says many fleets are purchasing consumables such as lights, filters, belts, hoses, etc.

Seewack attributes the growth to more millennials in the workforce, who are more accustomed to buying online and to the convenience online buying offers. And in fact MacKay’s research indicated that convenience was cited as a rationale for online parts purchases by 78% of survey respondents.

“We have people that order from us every day or two,” Seewack says. “Basically they fill a cart, and then every couple of days they process it and place their order. I think the benefit is that they can get a trailer part or a tractor part across a variety of categories all from the same supplier.”

Seewack admits that online parts sales “will never replace the local distributor, but is a good adjunct to distributor sales.”

Mike Harris, senior vice president of sales and branch operations at FleetPride, the largest independent distributor, agrees with Seewack’s assessment. “There are certain products that require in-depth questions, product knowledge and expertise and that can present a challenge for e-commerce,” he explains. “The opportunity is to solve some of those problems, so there is still a balance. Customers want to use e-commerce to streamline the ordering process for repetitive purchases. They want a better method of placing orders faster. However, solving for the more complex questions in parts ordering is a challenge for e-commerce, but one that I think the industry can solve.”

Blodgett says one of the reasons survey respondents cited for not purchasing parts online was a concern over losing the relationship with their local distributor. He adds, “It will be interesting to see as millennials become even more responsible or assume higher positions within organizations whether that same philosophy will continue.”

Rick Reynolds, president and owner principal of Peach State Truck Centers, a Freightliner and Western Star dealership with 11 locations in Georgia and Alabama, believes online retailers like Amazon will be a threat to some degree, “but in the long run I still believe the local dealer or distributor will have a competitive edge over these large e-commerce warehouse organizations because of the level of service they can deliver as part of the value proposition that comes with purchasing a part.”

According to Ryan Colby, corporate parts director at Kenworth Sales Co., a Kenworth dealership with 22 locations in seven western states, last year 5% of the company’s parts sales were through the company’s B2B e-commerce solution. “So far this year we are maintaining that 5%, but I dare say, that sooner rather than later that number will be 20% of all retail sales.”

Greg Klein, president and CEO of Inland Truck Parts, an independent parts and service operation that now has 42 retail locations following its recent merger with Drive Train Industries, says e-commerce will continue to grow “and will be part of the pricing issue, especially for those companies who are just trying to distribute parts without any value added.”

Stephen Swords, president of Parts and Service Solutions LLC, the distribution arm of Pilot Flying J, raises an interesting point regarding e-commerce. “The true e-commerce guys are going to struggle if they don’t also have brick and mortar, because when a truck is broken down along the highway, that e-commerce level really does not do a lot of good, because you need the part right [at the site of the breakdown] in order to get the truck fixed and back on the road.”

He does add that for stocking items, e-commerce will have an impact. “I personally think this is a good thing, because there are some huge opportunities in e-commerce, especially on the B2B side.”

About 12% of heavy-duty parts are purchased online. Of all online parts purchases, heavy-duty distributors are getting the bulk of the business with truck dealers getting the second biggest share. Amazon is currently only getting 14% of the online purchase of heavy-duty parts. Overall, online parts purchasing is expected to grow, and there may be shifts in where those parts are purchased.

Source: Mackay

Consolidation is happening at every level

While e-commerce has had a big impact on the truck parts marketplace, it is not the only force at work changing distribution patterns. “Consolidation seems to be the word of the day in our industry,” Colby says.

However, Klein says the industry has been consolidating very significantly over the last 20 to 25 years. “Consolidation is now reaching its culmination after a long process that has been going for several decades.” In fact, he does not believe there is a lot of consolidation left on the independent side of the parts business.

Tam, however, sees a lot of opportunity for additional consolidation on the dealership side. “Something like 40% of all commercial truck dealers are single locations,” he says. “I don’t know what the right number is or how many dealer groups there should be, but there certainly is an opportunity to get some synergy out of that market with consolidation. There is an advantage to the fleet to see the market consolidate.”

Don Reimondo, president and CEO of marketing group HDA Truck Pride, expects to see consolidation continue on the supplier side. “It is a reality of the marketplace and it is going to continue in the Tier 2 and 3 marketplaces. It is driven by the fact that margins have eroded and technology is rapidly changing.” But he is quick to add that he does not think this will have “a profound impact on the market. [Consolidation] has become a way of life.”

Blodgett also expects to see more consolidation on the supplier side. “Vehicle manufacturers are attracted to someone who can come to the table with a wider breadth of product. Rather than having to interface with two or three companies, they can interface with just one.”

He adds, “As vehicles become more complicated, it is much easier for the components to communicate with each other if they are all under one umbrella.” He believes this could result in better product development, which ultimately will benefit the fleet.

Tam believes technological developments are playing a role in supplier consolidation. “Technology is poised to change dramatically with things like autonomous trucks and electric trucks. Suppliers are dipping their toes in the waters to develop solid offerings — not so much reinvent themselves, but rather to change with the times and change with technology to remain relevant.”

Consolidation of the distribution base, whether dealer or independent distributor, can also benefit fleets, giving them fewer contracts to be negotiated and consistent pricing across a broader network.

Swords says consolidation will help fleets when they are operating outside their home network. “Consolidation gives them the ability to go into a familiar provider and be taken care of, knowing that if there is an issue it takes just one phone call to get it resolved no matter where the truck is.”

One of the main factors behind consolidation has to do with the aging of the ownership of these businesses. “There are a tremendous number of baby boomers that are reaching an age where they will have to make a decision on what to do with their business,” explains Tom Marx, partner in Hart Marx Advisors, a mergers and acquisitions firm. “Often times they don’t have a structure in place, either family, ESOP [employee stock ownership plan], or partners, so the best option is to sell the business.”

Marx does not believe consolidation on the distribution side will have much impact on fleets, “because they still will have plenty of distributors they can choose to do business with.”

In fact, he adds, “It might make it easier to deal with the larger distributors, because they may have more depth of product and the fleet could get better service from a larger distributor.”

However, Reynolds cautions fleets that they need to look at what is gained or lost when doing business with a company that has consolidated. “Is the customer going to have an enhanced customer experience? Will it remain the same as before the consolidation, or will it decrease?”

Harris says the truck parts market is still very fragmented. “Smaller distributors, whether it is an independent parts distributor or dealer, may have a difficult time meeting the demands of the customers moving forward as expectations increase and customers further consolidate.”

Marx says that as dealers try to get more of the fleets’ business, “they are up against very entrenched distribution systems, and that puts the fleet in a strong position to negotiate. They may be able to get a little more of a price point.”

However, a highly consolidated market is not without its risk. The biggest concern if you get to a single source of supply is lack of parts availability, and there could be some loss of price competitiveness.

How long can fleets expect consolidation to continue? Marx says, “As long as capital remains relatively low cost, it could continue for another three to five years.” There are, however, several things that could derail the current trend toward consolidation. “One of those would be interest rates,” Marx says. “If the Fed continues to push them up significantly higher, that could be a problem. And the second factor is a general economic downturn. If we head into a recession, there will be some impact on the value of these types of businesses.”

He is quick to add that it is difficult to have a crystal ball, because the current upturn has lasted longer than most people thought it would.

One of the benefits of consolidation is that fleets get a consistent array of parts across a wide network.

Photo courtesy Fleet Pride

New kids on the block

Trucking has attracted a great deal of outside attention lately, with companies from the automotive and industrial sectors venturing into truck parts sales. Colby explains that for manufacturers such as Paccar, only about 40% of the parts on their trucks are proprietary, leaving 60% of parts open for other firms to compete in. “The Napas and the Graingers are coming to get a piece of that pie.”

And it’s a big pie, says MacKay & Co.: $30.4 billion at retail every year from parts for Class 6-8 trucks, school buses, trailers and container chassis.

Blodgett says he does not doubt “the ferocity or ability of some of these new entrants.” He adds, “They have a footprint across the nation and have distribution all figured out, or at least have [parts distribution centers] strategically located. It is, however, a bit of leap for them” to find the right counter people to be able to sell truck parts.

‘There is a lot more to a parts transaction than just buying the part,” Reynolds says. “There is a lot of value that is contributed to that experience after the fact. On a consistent basis the customer deserves to have parts immediately available, delivered to them sometimes multiple times a day, and have a sales consultant who can provide then with the best information as quickly as possible.”

Reimondo says he understands the encroachment by the automotive parts sellers into the truck space. “They have to find a way to continue to expand or grow, and the medium-duty marketplace is a massive adjacency,” he says. “They are already selling the guy brakes for his 1-ton pickup truck, so why wouldn’t they sell them for his grain truck?”

HDA Truck Pride encourages its distributor base to do the exact same thing and explore the medium-duty market, which Reimondo thinks “is significantly underserved in the aftermarket.”

Pennig says traditional aftermarket distributors need to recognize that these new companies are targeting the truck parts aftermarket. But a more disturbing trend to him is some suppliers attempting to sell directly to the end user, bypassing traditional distribution. He believes distribution plays an important role in the parts transaction by providing knowledge and expertise about parts.

Wade is seeing a new class of trade in the truck parts aftermarket, which he calls bundlers. “These are companies that buy for resale, but act as traditional suppliers, not as intermediary businesses.” He references companies such as Dorman and Automann that do not manufacture anything but have as many as 150,000 SKUs available.

Fleets are looking to consolidate their parts purchases and do business with fewer vendors.

Photo courtesy Kenworth Sales Co.

Technology and component integration complicate matters

Today’s trucks are technological wonders, and lately we have seen more integration, especially in the drivetrain. “I think the independent channel is at a disadvantage as that trend progresses,” Blodgett says, “but do not underestimate their ability to figure out ways to support that market.”

Klein says on the surface, integration may appear to favor the dealer network, “but the countervailing force against that is the fact that there are simply not enough dealer bays to fix all the vehicles out there, and customers do not want to wait weeks and weeks to get service performed.”

Integration is not without its challenges. “It’s certainly nice for dealers, because they can have a smaller parts inventory and will not have to train their technicians on multiple systems,” Tam says. “The flip side of the coin is that some fleets still have a brand preference for ‘mismatched’ systems, for lack of a better term.” He believes it is incumbent for independent distributors to have a pull-through marketing strategy in place so those options remain available.

Pennig believes that the original equipment supplier and independent channels can continue to coexist in the market, regardless of product complexity. “The independent as well as the dealer needs to continue to invest in people and technology in order to stay viable and relevant in the market. If they don’t, it doesn’t matter which channel they come from — they won’t survive.”

Despite all these changes in truck parts distribution, Wade says, “The power is in the hands of the fleet, and even the owner-operator, about their choice in parts and service sources. The fleet is gaining more and more market power because distribution has become so fractured.” This means the fleet owner determines where he is comfortable buying parts. Wade explains, “He may buy filters by the case from Amazon, transmissions from the dealer, and headlights and maintenance items from Charlie down the street or from Fastenal. He will buy where he is comfortable buying.”

Related: Blockchain Enters the Aftermarket

More Aftermarket

ConMet Expands Aftermarket Brake Drum Lineup With TruCast

A new heavy-duty truck brake drum option in the aftermarket gives customers more flexibility within the ConMet product family.

Read More →

Phillips Opens High-Tech Distribution Center for Faster Parts Delivery

Phillips Industries’ new Cincinnati-area distribution center is now shipping aftermarket trucking parts nationwide, aiming to speed up delivery times for customers.

Read More →

Volvo to Sponsor America’s Road Team for 2025

Volvo Trucks announced that it is extending its exclusive sponsorship of America’s Road Team for 2025.

Read More →

Webb to Start Taking Orders for UltraSet Pre-Adjusted Wheel Hubs

Webb, which recently acquired the Stemco Trifecta pre-adjusted hub program, will soon start taking orders for its replacement pre-assembled hub, the UltraSet.

Read More →

All-Makes Automatic Brake Adjusters, Ride Height Control Valves from Midland

SAF-Holland has added automatic brake adjusters and ride height control valves to its Midland All-Makes Program.

Read More →

ZF Aftermarket Expands [pro]Academy Training

ZF Aftermarket said it is expanding its ZF [pro]Academy training and will be adding 40 new modules this year.

Read More →

Eaton Adds Remanufactured Advantage Line of Clutches

Eaton has added its Advantage clutches to its remanufactured product line. The clutches feature a unique strap drive intermediate plate designed to allow customers to choose the latest OE specification

Read More →

ConMet Acquires TruckLabs, the Creator of TruckWings

Commercial truck and trailer parts provider ConMet acquired TruckLabs, the company that created TruckWings, an aerodynamic device that attaches to truck cabs and deploys to close the gap between truck and trailer. TruckLabs now operates as a subsidiary of ConMet.

Read More →

Diesel Laptops Releases Fault-Code-to-Part-Number Tool

Diesel Laptops said its Truck Fault Codes allows users to input a fault code and immediately identify and order the parts needed to complete repair work.

Read More →

Heavy Duty Parts and Labor Costs Dropped in Q2

A benchmarking report from TMC and Decisiv reveals good news for fleets as heavy-duty parts and labor costs dropped in the second quarter of 2023.

Read More →