Industrial activity has picked up its pace during 2017 after a stretch of weakness that lasted from mid-2015 until late 2016. Recent reports have done little to change our underlying assumptions of the U.S. economy or freight demand.

Recent reports on industrial activity have done little to change FTR's viewpoint on the strength of the U.S. economy or freight demand.

Industrial activity has picked up its pace during 2017 after a stretch of weakness that lasted from mid-2015 until late 2016. Recent reports have done little to change our underlying assumptions of the U.S. economy or freight demand.

Let’s key in on a couple of important segments to trucking and see what sort of movement has occurred during the first half of 2017.

It is easy to see from the chart above that mining activity was very, very strong early in 2017. This sector includes four important segments: stone/earth, metal, coal, and oil/gas. Not surprisingly, the impetus for growth has come from the oil and gas shale fields. Construction (and especially housing) have been lackluster, metal demand has rebounded some but remains weak, and coal demand turned back up in late 2016 but hasn’t moved much since then.

Durables are the biggest component of manufacturing and tend to be more cyclical than non-durables (we may not buy a new car during a recession, but we still eat and drive). This segment slowed noticeably during the second quarter – and it remains well below the average growth for this recovery.

Automotive (this includes both vehicles and parts) is a big component of durable manufacturing. While we did eke out a gain in the second quarter, you can easily see that we are running well below the recovery average and we had a very negative quarter in Q1. Automotive demand looks to have topped out, and growth in industrial activity or freight demand is not likely to come from this segment.

Non-durables did see a notable uptick in the second quarter. Surprisingly, this sector has been quite weak during much of this recovery. The three main segments are: food, fuel, and chemicals. Chemicals growth has been weaker than anticipated during this recovery as it seems that a portion of our export activity has dried up. Our abundant natural gas (thanks to fracking) would seem to be a positive since it is a major input into many of the chemical processes, but, as of yet, it has not made a big mark on overall output.

While some industrial activity has shown recent improvement, it is nowhere near the big gains in demand and pricing that we have seen from the spot market over the last year. Contract markets, however, are adjusting more slowly. Can we keep the growth going if the industrial sector doesn’t show further improvement?

One noteworthy item has been the sustained power of this recovery. It has not been overly strong, but it has been historically long. The good news is that there is nothing currently happening that would indicate a serious threat to the continuation of a 2%+ economy. That should give us a reprieve from recession talk for at least another year. After that…stay tuned.

ACT Research data shows volumes hitting a four-year high and supply-demand balance strengthening, but higher oil prices are undercutting tariff relief and tempering optimism.

Read More →

The patent-pending cargo solution integrates a digitally connected cargo door and an intelligent locking system with the TrailerHawk.AI technology platform.

Read More →

The impact of the Iran conflict extends beyond fuel costs, bringing more fraud and cybersecurity risks to the trucking industry.

Read More →

Speaking at the TMC Annual Meeting in Nashville, ATA President Chris Spear said trucking faces mounting pressure from rising fuel prices, geopolitical instability, and uncertainty around trade policy.

Read More →

More than 100,000 new trucking companies enter the industry each year, but regulators manage to audit only a fraction of them. That churn creates opportunities for inexperienced startups — and for “chameleon carriers” that shut down after safety violations and reappear under new identities. Read more from Deborah Lockridge in this commentary.

Read More →

HDTX is an intimate event that connects heavy-duty trucking fleet managers with industry suppliers through small-group discussions, educational sessions, and structured one-on-one meetings.

Read More →

New DAT One feature shows top-paying loads directly on an iPhone’s home screen, helping carriers react faster to spot-market opportunities.

Read More →

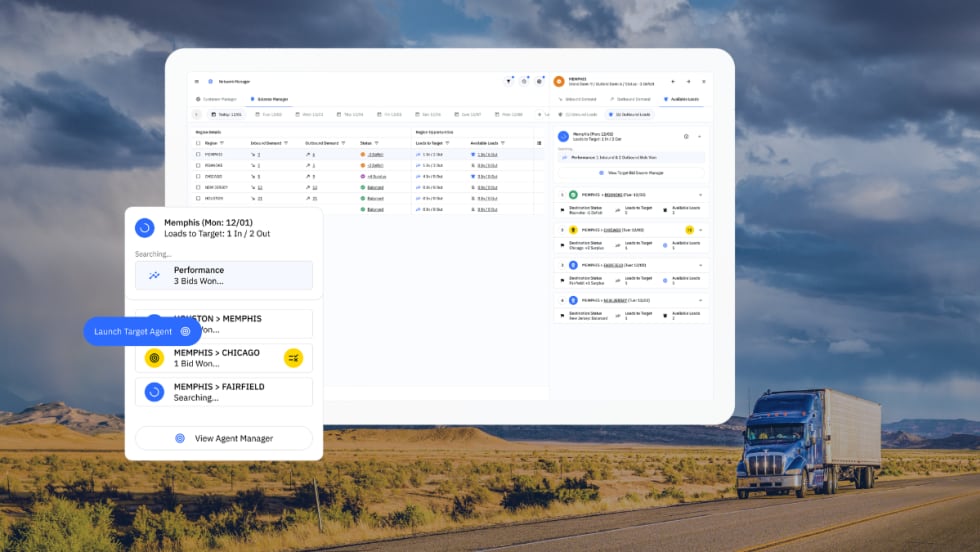

Optimal Dynamics says its new Scale platform uses AI agents and optimization to help carriers find and secure freight that improves network balance and profitability.

Read More →

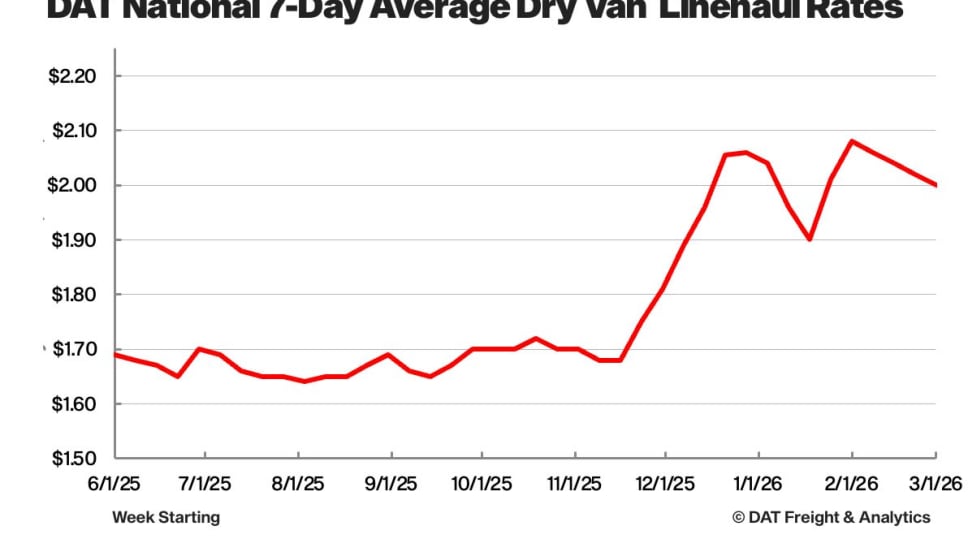

DAT Freight & Analytics data shows tightening flatbed capacity, easing produce markets, and softening van and reefer rates.

Read More →

NACFE's Run on Less - Messy Middle project demonstrates the power of data in helping to guide the future of alternative fuels and powertrains for heavy-duty trucks.

Read More →