What Economic, Trucking Numbers Tell Us About Recession Likelihood

Is the U.S. in a recession? The usual measures of the country's economic health have been rendered unreliable by the continued fallout from the COVID-19 pandemic. Two experienced trucking analysts share what they're seeing in the numbers.

September 13, 2022

FTR's freight outlook doesn't look like a recession.

Source: FTR

8 min to read

Are we in a recession or not? The answers vary widely. CNBC noted in a Sept. 5 article that predictions of academics and analysts range from a recession is inevitable to a recession is unlikely.

Eric Starks, chairman and CEO of trucking industry analyst firm FTR, compared the situation to a baseball game where the scoreboard is broken. What inning are we in? How many outs? How many on base? Without the numbers, teams have a harder time making decisions on what to do next, he told attendees of Heavy Duty Trucking Exchange in a virtual address on Sept. 8.

When it comes to the overall economy and trucking, the topsy-turvy world we’ve been thrown into by the COVID-19 pandemic, supply chain problems, and shocks such as the war in Ukraine makes it hard to figure out just where we are. The traditional definition of a recession as two successive quarters of economic contraction just doesn’t seem to work this time, especially looking at the trucking environment.

Normally freight data leads the economy, with a freight recession one to two years before an economic recession, said Jeff Kauffman, another virtual speaker at HDTX, who is HDT's contributing economic analyst as well as Principal, Transportation & Logistics Equity Research at Vertical Research Partners. “This cycle marks the first time that the consumer or stock markets or equities are pricing in a recession before we see any evidence of a downturn in the freight markets.

“Is recession inevitable, given the Fed’s interest in fighting inflation, a drop in the value of consumer household assets .... and war in the world?” Kauffman said. “If you’re in charge of a truck fleet, how do you plan for the future against this backdrop?”

Starks and Kauffman offered some insight into the economic and freight indicators for HDTX attendees.

Economic Indicators in Chaos

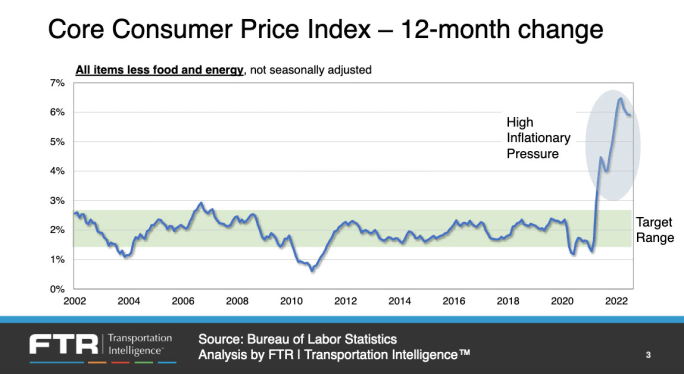

Inflation

Inflation has been a major concern, as well as the risk that in trying to slow the economy the Fed will overcompensate. But Starks pointed out that according to the Core Consumer Price Index (which does not include the volatile food an energy sectors), inflation does appear to have started easing.

Kauffman, saying inflation may have peaked in June, broke down the key components of inflation. Looking at a variety of commodity prices — corn, heating oil, aluminum, steel, etc. — and truckload spot rates and other indicators, he said, “We’re starting to see a little pull back in inflation,” although he noted it’s still high, averaging about 6% core for the last three months.

There has been some slowdown in hiring, in particular the consumer-goods and technology industries. “But it’s not because profits are suffering; it’s because they can’t get their equipment due to supply chain or chip issues.”

Inflation is still high but easing.

Source: FTR

Consumers

Retailers have been dealing with higher than expected inventories. “This has created some angst in the consumer sector, because if you’re in the retail sector you don’t want too much inventory,” Starks said.

Shipments of imports coming into North American ports have been high, but the export market really has not picked up. “That disconnect has become larger,” Starks said. “That’s a bit of a concern in some respects but suggests we have a fair amount of healthy demand. If we’re bringing stuff in, that means people are buying things.”

Although the most recent corporate earnings season shows “there are cracks in the dam, there’s nothing to forecast an imminent recession,” Kauffman said. “Tech- and consumer-facing businesses are slowing. Many retailers stocked up on the wrong type of goods because of supply chain issues. Walmart and Target have too many bicycles and outdoor furniture and big-screen TVs — but in terms of what people are purchasing, they don’t have enough.”

Manufacturing

As the red-hot consumer market has started to normalize following the post-pandemic surge, Starks said, the manufacturing sector appears to be making up the difference.

“Manufacturing was really kind of put onto back burner early in the pandemic… then we had supply chain issues… then it was competing with consumer market for capacity. Now that consumers are starting to ease back a little, it allows some capacity for manufacturing, so we expect manufacturing will continue on an upward trend,” he explained.

And new orders for capital goods have risen fairly steadily since the pandemic plunge, he said, which is one reason for FTR’s optimistic manufacturing outlook.

Wall Street and Corporate Profits

Since the stock market reached a high in late January, the S&P 500 fell 22% by June, Kauffman noted. It’s come back up the last few months but it’s still down about 11%, he said. Nasdaq fell 30% from its peak last November and has rallied but still is down more than 20%. Both of those types of drops tend to be reflective of the types of stock action we see in a recession, he said — but how warranted is this?”

With S&P 500 market values at 17 to 18 times forward earnings, Kauffman explained, these valuations are consistent with about a 3% to 2.25% inflation expectation. “The bet the stock markets are making is that investors believe this [current] core inflation of 6% is going to trend backwards to about 3%. That’s above the long-term 2% rate [that the Fed targets] but is still a much better place than we have been.”

What do the Economic Numbers Mean for Trucking?

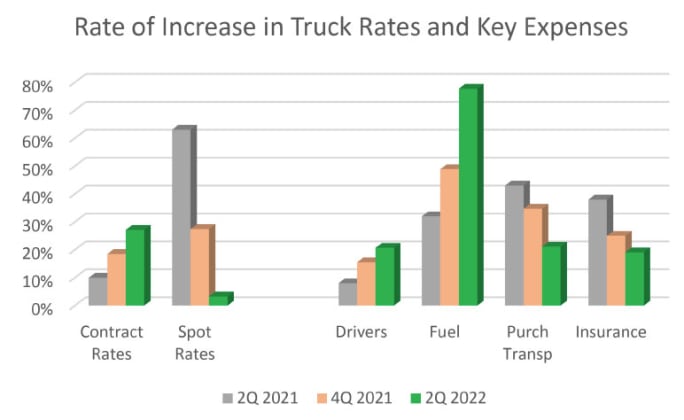

Looking at 30 of the biggest publicly traded freight companies, Kauffman said, “we continue to see upward momentum in contract rates.” Spot rates a year ago were about 60% higher but are basically flat right now.

“A lot of people believe there was freight forced out of its natural mode because of capacity and supply chain constraints,” he explained, and those substitute modes tended to cost more. “This year we’re seeing moderation – not because of more capacity, but because freight is going back to where it should be.” It’s not a misbalance of capacity and freight, he believes.

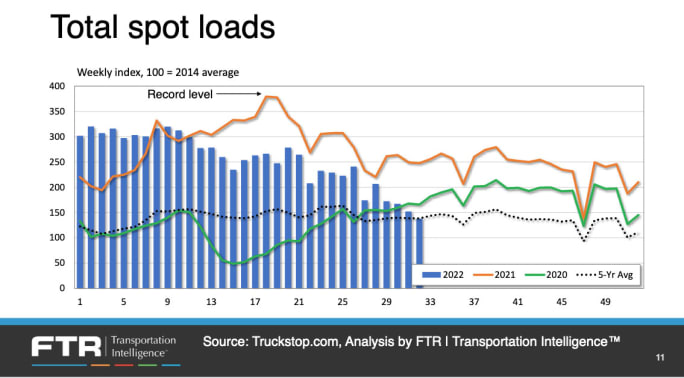

As the market has started to normalize, less freight is moving on the spot market.

Source: FTR

Freight markets and freight rates have experienced whiplash from the continuing effects of the pandemic and the following supply-chain imbalances.

Looking at the spot market, Starks said, “is helpful to see what inning we’re in. If we look at amount of freight in the system… the number of loads posted in the system is moving back to the five-year average – more of a normalization. The question is, will we continue to move below that or kind of stabilize?”

Spot rates have been falling, but he pointed out that they are still noticeably above the five-year average. And if you look at spot rates without fuel prices, he said, we’re still above pre-pandemic levels.

FTR’s truck freight outlook is still relatively healthy, with the company’s analysts predicting a 3% to 3.5% growth this year, which they believe will fall to about 2% in 2023, 1.8% in 2024. If the economy slows more than the firm is predicting, Starks said, “It could get us to a flat 2023 market, but we don’t get to a negative rate in our forecasts. This is different from a normal recession where we see a big cutback in freight.”

Truck utilization is starting to soften, Starks said, but it’s still above the 10-year average, “which suggests there’s still a little bit of pressure in the system from a pricing standpoint.”

Truck and Equipment Orders

Looking at Class 8 order activity, Starks said, “Clearly orders have softened. But we have to understand why. If we look at what backlogs are doing, they have been coming back down but are still at very high levels.”

New-truck lead time is still a projected 7.3 months he said – meaning if there were no orders at all, truck makers could continue to build at their current rate for seven months before they were caught up.

“We in essence are full for all build spots for the rest of 2022,” Starks said. “In fact, they are hoping they can build more, but Q1 2023 is likely full. This is not normal, folks! This tells me there’s still a lot of pressure for needing equipment.”

Kauffman also said that truck and trailer order numbers aren’t forecasting a recession. In fact, he said, ACT Research is predicting some 300,000 Class 8 orders next year and more still in 2024 and 2025.

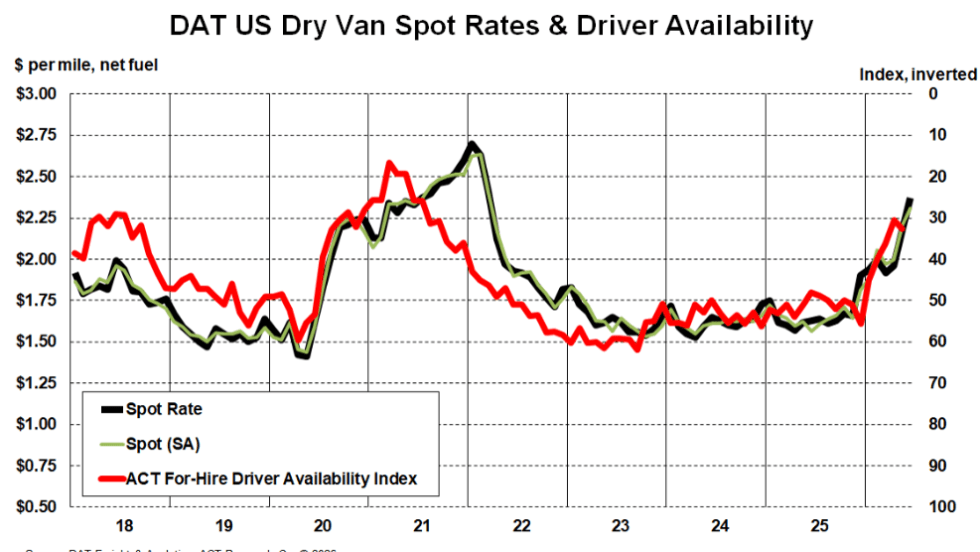

Although spot rates have fallen, contract rates have been rising.

Source:

Are We in a Recession? Is a Recession on the Horizon?

Kauffman noted that generally, freight grows at a faster rate than real GDP. But when comparing real GDP (indicating economic growth) to ACT Research’s freight composite index, historically, 1% GDP is consistent with a 2-3% freight deterioration. Going by that metric, he said, ACT’s projections for 2023 would be consistent with recession.

In addition to freight data, Kauffman is looking to corporate profits and rail carload data, which he said both tend to provide insight.

“Historically, profit recessions tend to appear before we see general recessions,” he explained, and that’s not what he’s seeing S&P 500 profits are rising about 17%; that’s dropping, he said, but said to also keep in mind that the numbers are tough comparisons to a year ago.

Meanwhile, he said, rail carload data is being artificially compressed by factors such as a poor grain crop last year and the chip shortages. “Rails are optimistic about the rest of the year.”

Overall, Kauffman concluded, “The normal recession trip wires haven been triggered yet:”

Rental fleet utilization remains at record levels

LTL weight/shipment remains higher

Rates continue to rise (but could be peaking)

Rail traffic is not a normal read right now, but it’s improving from constrained levels

Spot truck rates have fallen sharply, but that’s more about mode shift than lack of demand

“All in all, we feel like the market has some legs to it that means we aren’t going to fall off the cliff,” Starks said. “You’ll continue to hear about risks, but whether those will impact our market, the answer is not significantly.”

The numbers do not suggest a typical recession, Starks said. “Nor should we expect a traditional recession, because we’re coming out of the Covid environment. It doesn’t feel like a recession, even though we’ve had two consecutive negative-GDP quarters," he adds.

More Fleet Management

Van Spot Rates Top Contract Rates for First Time Since 2022

There’s more good economic news for the North American trucking industry according to the latest Truckload Volume Index report from DAT.

Read More →

Carrier Transicold Extends Refrigerated Trailer Life

Fleet Refresh enables refrigerated fleets to replace aging transport refrigeration units instead of entire trailers, while adding Lynx Fleet telematics and BluEdge service coverage.

Read More →

FTR Says Freight Rates Surged in May

FTR's Trucking Conditions Index surged to a record high in May, the analytics firm reports.

Read More →

Meet HDT's Truck Fleet Innovators at Heavy Duty Trucking Exchange

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for HDTX, September 23-25.

Read More →

Sponsored•July 1, 2026

Enhance Fleet Performance with High-Efficiency Auxiliary Power Units

Drive sustainable cost savings while increasing driver comfort during short- and long-haul logistics operations.

Read More →

Sponsored•June 30, 2026

Is Your Parts Procurement Process Reactive or Proactive?

Ready to revamp your parts procurement process? Learn how now with “Strategic Parts Purchasing: A Process Checklist”

Read More →

What Trucking Events are Happening in 2026?

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

Truckload Rates Keep Rising as Tight Capacity Fuels Freight Market Recovery

Spot and contract rates continued climbing in May and June, not because freight demand is surging, but because fewer trucks and drivers are available.

Read More →

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →