Why Trucking May Not Be a Leading Economic Indicator This Cycle

Traditionally, trucking was looked to as an early indicator of larger economic problems. Find out why HDT’s economic analyst thinks this freight cycle may be different.

The May consumer price index report showed an unexpected acceleration in total inflation to about 8.6%.

Source: Bureau of Labor Statistics/Tahoe Ventures

Inflation, Inventory Bullwhip, Stagflation, Recession… there’s no shortage of negative headlines. Yet freight markets continue to show positive volume growth and double-digit yield improvement, resulting in stronger year-over-year profits. Rental utilization remains strong, less-than-truckload weight per shipment continues to rise, and industrial production continues to improve at a 6% clip.

So are the stock market and media concerns overblown?

Traditionally, trucking was looked to as an early indicator of larger economic problems. This freight cycle may be different.

The type of slowdown we could be headed toward might not resemble anything we have seen in about 50 years. Each of the last four or five downturns (excluding the Covid-shutdown recession of 2020) was caused by an imbalance of some sort. In 1990 it was the savings and loan crisis. In 2001, the dot-com bubble; in 2008-2009, the housing/mortgage crisis. And the soft economic landings of 1986, 1995, 2015 and 2019 were inventory/overbuild driven.

Why This Cycle Is Different

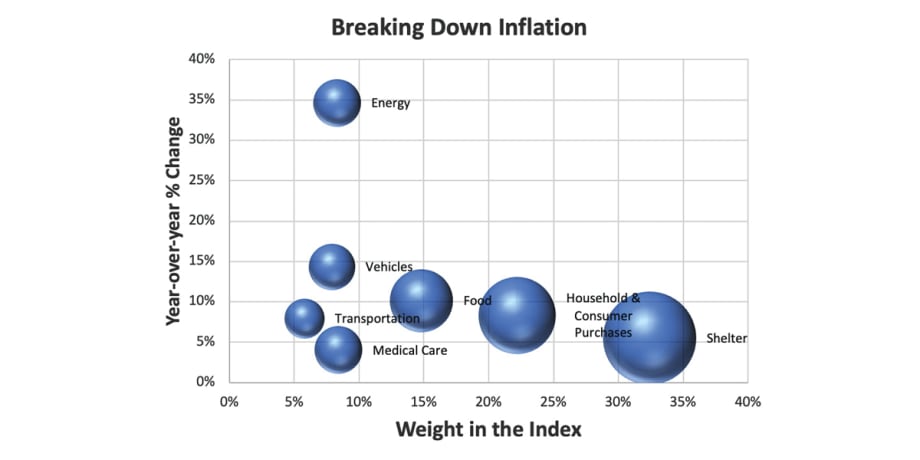

What is different this cycle is we have uncontrolled inflation that was given an unexpected boost by the geopolitical events in Europe. We have broken down the sources of current inflation and their weight in the calculation of the index in the graph below to make this point.

The May consumer price index report showed an unexpected acceleration in total inflation to about 8.6%. It rose 1% from April after a 0.3% increase the previous month. The largest contribution was from energy. Energy makes up only 8.3% of the index, but this sector rose 34.6% year-over-year, largely over concerns about a potential withdrawal of Russian oil. This accounted for about 2.9% of that 8.6% inflation.

The second largest contribution was the cost of shelter. It only rose 5.5%, but it accounts for about 32.4% of the index, so that’s another 1.8% of the 8.6%.

The other large contributions came from food, which saw 10.1% inflation because of drought, supply chain challenges, and the Russia-Ukraine conflict. This accounts for about 14.8% of the index, or about 1.5% of the 8.6%. Vehicles (new and used) account for 7.9% of the index and saw inflation of 14.3%.

How Do We Beat This Inflation?

In theory, the government can try to slow the economy by raising interest rates (monetary policy) and taking actions such as releasing strategic oil reserves and improving supply chain congestion (fiscal policy). A slowing economy will result in slower growth or contraction in housing/rent, energy use/prices, and consumer prices. Hopefully, inflation should moderate toward a more acceptable level like 3% to 4%.

However, here is the concern: This might not be enough to contain inflation. A continued push for higher rates may slow economic activity too much, causing a recession.

Energy and food inflation (23% of the index) are being caused more by geopolitical events in Europe and weather, which governmental slowdown initiatives cannot control. Furthermore, the supply chain squeeze might take more than the economy to stabilize, and that accounts for about 20% of the index.

Lastly, the 32.4% of the index that is being caused by shelter costs might not slow quickly with rising interest rates. The positive news is that shelter, medical, and transportation-related inflation is only rising at a 5.6% rate, contributing only a 2.6% impact toward the index. Food and energy are adding 4.5% to the figure.

What’s the Message for Trucking?

We may not see it yet, but the slowdown is coming. Consumer spending patterns are already reacting to the higher prices. The magnitude and duration of the pending downturn remains uncertain, and the market for bank and capital access may be more challenging in a year.

Will there be a recession? Most likely. When will it happen and how long will it last? This is the uncertainty, so plan accordingly. By the time we see it in the freight data, it may be too late.

This commentary first appeared in the July 2022 issue of Heavy Duty Trucking.

More from Jeff Kauffman: Fleet Financial Trends Imply Solid Start to 2022

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →