More from Jeff Kauffman: The Great Modal Migration of 2021 Continues [Commentary]

Fleet Financial Trends Imply Solid Start to 2022

As we neared the end of 2021 and took a look at third-quarter fleet earnings reports, the news looked good — good enough that the stock prices of the group were up 15.6% during the earnings reporting season, compared to the Standard & Poor’s 500 Index that was up 7.6%.

January 4, 2022

Jeff Kauffman, a recongized trucking and transportation authority for almost 30 years, breaks down the trucking's economic indicators in HDT's Behind The Numbers column.

Graphic: HDT

4 min to read

As we neared the end of 2021 and took a look at third-quarter fleet earnings reports, the news looked good — good enough that the stock prices of the group were up 15.6% during the earnings reporting season, compared to the Standard & Poor’s 500 Index that was up 7.6%.

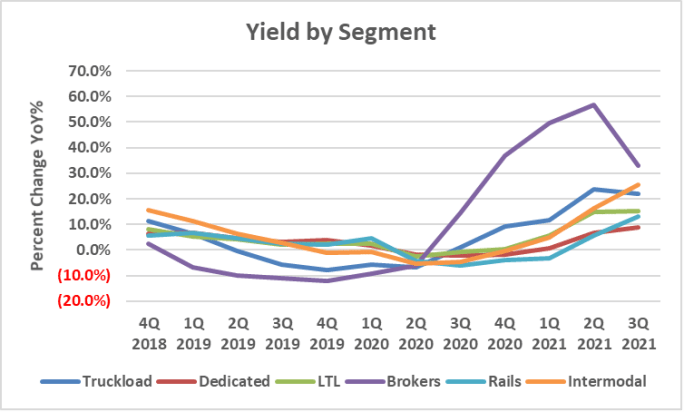

The big story for the third quarter was the overall rate of improvement in yields (pricing + fuel surcharge + mix.) Nearly every freight sector has been experiencing double-digit yield improvement. Because yield improvement carries no associated variable cost, much of this offsets inflation and drops straight to the income line.

We look at margin improvement in terms of basis points (100 basis points = 1 percentage point). The top performances from a margin improvement standpoint this past reporting quarter have been:

Rideshare (Uber/Lyft): 2,725 basis point margin improvement

Delivery (Uber): up 450 basis points

Brokerage/Logistics: up 390 basis points

Intermodal: up 385 basis points.

Both key trucking modes (over-the-road truckload and less-than-truckload) reported solid margin improvement as well, up 230 and 210 basis points, respectively.

On the other side of the coin, sectors disappointing were:

Supply Chain/Warehousing: 550 basis point margin decline

Dedicated Truckload (a larger 320 basis point margin decline)

Final Mile (down 50 basis points).

The common themes here were supply chain inefficiencies and labor cost inflation.

Source: Company Reports, Tahoe Ventures LLC

8 Observations from 3Q Earnings Reports

Truck OEMs are having trouble delivering vehicles related to the chip and supply chain shortage, but we believe that difficulty will peak in the fourth quarter.

Less capacity coming into the industry is a positive in terms of tight truck capacity and therefore pricing favorable to fleets will likely last through 2022.

Tight capacity is also boosting gains on sales for companies in trucking and leasing

Rail system fluidity looked like it might be turning a corner in October.

We are seeing a narrowing of the negative spread between contract pricing and spot rates.

Consumer and retail stock-outs and gift cards may extend holiday shipping into the first quarter of 2022.

LTL continues to be a safe haven within trucking, setting an all-time quarterly rate increase.

Intermodal rates are rising quickly behind trucking rates.

Trucking Sector Performance

Pure Truckload

Truckload fleet earnings are still contracting (down 6%), but yields are rising ahead of expectations, and more than offsetting rising driver wage costs. Those trends resulted in another quarter of double-digit revenue growth (+10.7%) and 230 basis points (2.3 percentage points) of margin improvement — the fifth straight quarter of at least such improvement. Many carriers have been reducing capital spending this year related to truck production challenges of OEMs.

Dedicated Truckload

While dedicated fleets have been a strong growth opportunity over time, they are the Achilles heel of the freight space this year, as long-term contracts have not allowed companies to keep up with rising labor costs, and high purchased transportation expenses have eaten into margins, resulting in a year-over-year margin decline of 320 basis points (3.2 percentage points). Revenue growth remained about 14% higher. In addition, some carriers are being negatively impacted by auto plant shutdowns and in many cases, retail staffing challenges.

Less-than-Truckload

LTL fleets reported some of the most consistent improvement in trucking. LTL yields continue to notch higher, up 15.3% year-over-year in the third quarter, up from a 12.7% rate the quarter before. Tonnage growth was a strong 6.3%, leading to a 2.1 percentage point improvement in operating margins — the fifth straight quarter of margin improvement.

Brokerage/Logistics

The brokerage and logistics group share the elevated revenue growth rates of the transportation sector, though contract rates are not yet keeping pace with spot rates. Companies reported an average of 57% revenue growth with accompanying 62% operating expense growth — yet operating margins grew by 3.9 percentage points because of the 33% improvement in brokerage/logistics yields.

The spread between revenue yields and purchased transportation expense is narrowing, which should be good for brokerage profits in coming quarters.

One trend we are taking note of is growing trailer pools. Some carriers, such as J.B. Hunt, run it through their truckload operation, but many brokerage and logistics companies are developing “power only” options, and those appear to be adding to margins across a greater number of companies.

Subscribe to Our Newsletter

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →