Commentary: Drug Testing and the Driver Shortage

FTR's Trucking Outlook: What the Numbers Say About Freight, Rates, and Drivers

Economic growth and freight rates are expected to remain solid well into 2022, according to transportation analysis firm FTR, but the struggle to find drivers is expected to continue to plague the industry.

September 6, 2021

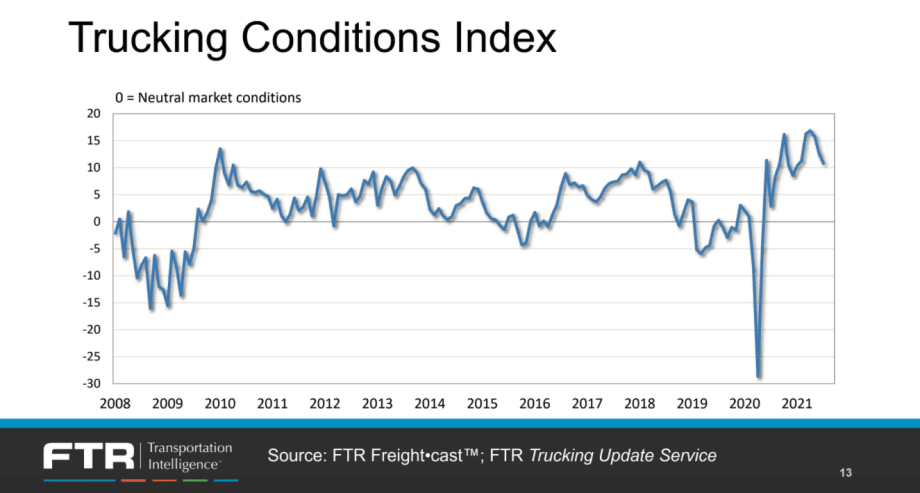

According to FTR’s Trucking Conditions Index, motor carriers are still enjoying conditions “as good as they had seen prior to the pandemic."

8 min to read

Economic growth and freight rates are expected to remain solid well into 2022, according to transportation analysis firm FTR, but the struggle to find drivers is expected to continue to plague the industry.

With its annual conference cancelled due to rising COVID-19 cases, FTR has launched a series of webinars in its place. On Sept. 2, FTR’s vice president of transportation, Avery Vise, noted that according to FTR’s Trucking Conditions Index, motor carriers are still enjoying conditions “as good as they had seen prior to the pandemic, although they’ve moderated somewhat from what was a record level.” (This index combines data on freight volumes, freight rates, fleet capacity, fuel price, and financing.)

Economic indicators such as the labor market, the consumer economy, industrial production and housing still reflect the volatility of recovering from the COVID-19 pandemic as well as persisting supply chain problems. Nevertheless, growth in both the gross domestic product and what FTR calls the Goods Transport Sector (the parts of GDP that affect freight) remain solid, Vise said, “and we expect it to be well into 2022 before we level down to what we think of as a normal pattern.”

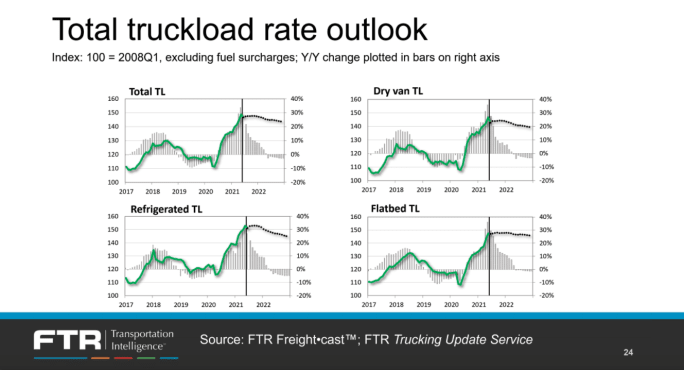

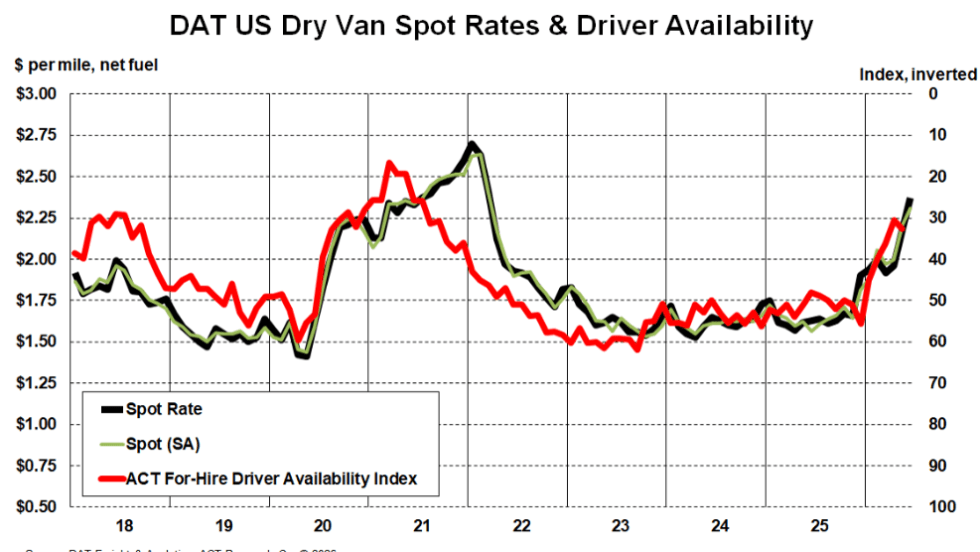

The spot market continues to operate at relatively high levels. Volumes aren’t keeping pace with the same period last year, but you have to keep in mind that growth in summer of 2020 was driven by much of the nation was reopening from COVID-19 shutdowns.

In the Truckstop.com system, dry van spot rates are 12% higher than last year – and they were very strong a year ago. For 2021 as a whole, FTR is forecasting spot rates to be up about 27% over last year. Looking ahead, FTR expects spot market rates to ease in 2022 but still be very strong. “By the end of next year, spot rates should still be running higher than they were even at the peak of the market in 2018.”

Vise noted that the spot market is only about 30% of the freight market, while 70% is less-volatile contract rates. However, he added, “the surge in spot rates has been so huge that it’s pulling up contract rates.”

FTR forecasts truckload contract rates to be up about 13% for the year, but don’t expect it to peak until early 2022. It is projecting contract rates for 2022 as a whole to be about 4% higher than this year. For less-than-truckload, he said, rates are up about 15% this year, and it projects them to flatten or drop slightly negative for 2022.

The spot market is only about 30% of the freight market, while 70% is less-volatile contract rates. However, “the surge in spot rates has been so huge that it’s pulling up contract rates.”

Looking at total loadings, Vise said, FTR projects 2021 will end up the year with strong growth of 6%. However, he said, you have to put that in context of the drop in 2020. “So while 2021 should be stronger than 2019, it won’t be by that much.” For 2022, Vise forecasts a 3% to 4% growth in total loadings compared to 2021.

The Truck Driver Situation

Vise identified several factors affecting the ability of motor carriers to find drivers, as well as exploring some of the economic indicators that attempt to measure the situation.

Typically, analysts have looked at payroll employment in for-hire trucking for an indication of driver supply. While not all these jobs are drivers, Vise explained, most are. Those numbers show that through July, the industry is still down 33,000 jobs, 2.2% below the pre-pandemic numbers from February 2020 (seasonally adjusted).

“We’ve seen stronger hiring in the past couple of months, but it has taken seven months to add less than half the number of employees that the industry added in the fourth quarter of last year,” Vise said.

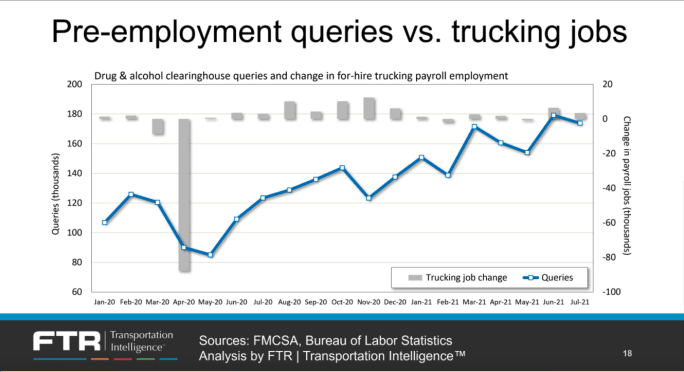

He also noted that these numbers do not include private fleets. One new statistic that does include both for-hire and private fleets is the Federal Motor Carrier Safety Administration's Drug and Alcohol Clearinghouse. Because full queries would indicate drivers that fleets are hiring (or attempting to hire), he explained, this offers a new picture into the driver situation. And, not surprisingly, the numbers “imply that it’s increasingly difficult to find drivers.”

Pre-employment queries in the Drug and Alcohol Clearinghouse “imply that it’s increasingly difficult to find drivers.”

Vise also said that payroll employment numbers are a less-useful benchmark of driver supply than what we’ve seen traditionally, and that’s because it appears that many former employee drivers or leased owner-operators have struck out on their own.

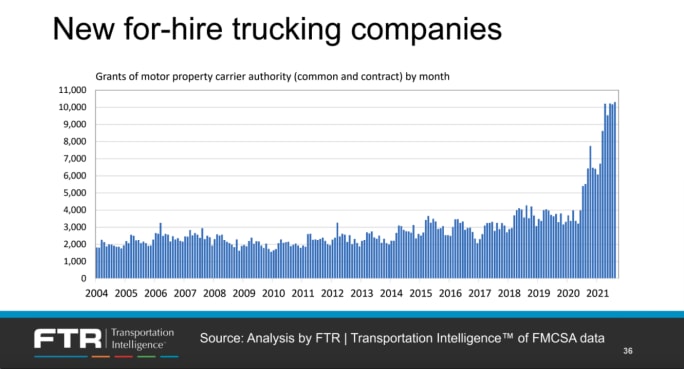

Since last July, he said, the number of new for-hire trucking companies getting their DOT authorization has surged – nearly 110,000 through August. About 70% of those have just one driver, and those aren’t likely to be captured by payroll employment figures. Most of them probably used to be owner-operators leased to a company, and some were likely company drivers, who decided to take advantage of robust spot freight rates and the growth of digital load boards and other new technology allowing them to more easily access freight.

“That’s creating something of an artificial deficit” in those payroll employment numbers. Those people are still driving, but they’re not available for larger trucking companies to hire.

Complicating analysis of the driver shortage is the number of former leased owner-operators and company drivers who decided to start their own trucking companies.

Why Can’t We Find Drivers?

In addition to the new-entrant trend, Vise outlined several reasons that it’s currently difficult to find drivers:

The overall labor participation rate, which has not moved positively in the past year. Some of this is parents who need to be home with their children because of virtual schooling or other pandemic-related concerns. Some portion of this has exited early through retirement.

Training and licensing of new drivers has lagged because of the pandemic; in fact, DOT numbers suggest the number of CDLs issued in 2020 was nearly 30% lower than in 2019.

The Drug and Alcohol Clearinghouse contributes to tightness in driver supply. As of Aug. 1, more than 82,000 drivers were flagged with violations since the database cranked up in January 2020, with nearly 67,000 still barred from driving. Vise said the numbers indicate that’s nearly 2% of the driving force we’re “glad to be rid of,” but it still means a lower driver supply overall.

Other industries are recruiting people who otherwise might be truck drivers. Although construction and manufacturing, viewed traditionally as competition for this part of the labor market, are still down from pre-pandemic levels, residential construction, warehousing and storage, and local delivery are all at higher levels than before the pandemic and are in need of workers. Local delivery, Vise said, is especially one to watch, since it offers more home time and significant relief from federal regulation.

Productivity: Despite the adoption by many fleets of technology to help improve the utilization of their fleets, “productivity hasn’t returned to where we thought it would be by this point,” Vise said, with continuing supply chain challenges.

Factors That Could Change the Forecast

There are still a lot of uncertainties leading to what economists call upside or downside forecast risks — basically ways the forecast could turn out to be wrong, either for better or for worse.

The pandemic. Although the Delta variant has led to case levels and hospitalizations not seen since last year, it has not appeared to cause significant economic damage — so far.

Labor supply. “The situation is quite extraordinary,” Vise said. There were more than 10 million job openings at the end of June, the highest ever since the government started tracking these statistics in 2000. And the lack of sufficient labor can have multiple economic impacts.

Inflation. “This spring we saw an increase in CPI (Consumer Price Index) like we had not seen in nearly 40 years,” Vise said. “We did get better figures in July, but inflation is still elevated compared to the norm.” On a 12-month basis, inflation, excluding food and energy, is more than 4%, which is very high compared to the past two decades. However, about a third of that increase is related to the price for used cars and trucks, which are in high demand and short supply as the automotive industry continues to grapple with shortages of chips and other components.

Competitive issues. Rail and intermodal are struggling with service issues, meaning shippers are putting more pressure on trucking.

Supply chain disruptions, with maritime capacity and port congestion compounding the issue. By the time the goods get to the port, they’re already behind schedule, which again means more demand for trucks.

Lean inventories relative to sales. “In retail, we are essentially at record low levels,” Vise said, and wholesale inventories are the leanest in nearly seven years – although, like inflation, much of that is due to inventories of motor vehicles and parts.

The semiconductor/chip shortage. This is at the root of the problems we’re seeing in automotive, he explained. “People can’t find the vehicles they want, so they just aren’t buying.” This is causing two issues:

We are seeing variable production in manufacturing, which complicates supply chain logistics and is one reason the spot market is so high.

When things stabilize and automakers try to meet pent-up demand, that’s going to mean high demand for trucking capacity and that will keep the driver supply tight.

The high number of new entrants and independent owner-operators in trucking. At some point, Vise predicted, this trend will swing the other way. “There should be some event, whether that’s softness in freight or just stabilization in the supply chain, [where] we will find spot rates will fall significantly and many of these new carriers will find their margins collapse, or worse, and they’ll flock back to larger carriers, as leased owner-operators, or will sell their trucks and become employee drivers.”

Subscribe to Our Newsletter

More Fleet Management

Sponsored•June 30, 2026

Is Your Parts Procurement Process Reactive or Proactive?

Ready to revamp your parts procurement process? Learn how now with “Strategic Parts Purchasing: A Process Checklist”

Read More →

What Trucking Events are Happening in 2026?

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

Truckload Rates Keep Rising as Tight Capacity Fuels Freight Market Recovery

Spot and contract rates continued climbing in May and June, not because freight demand is surging, but because fewer trucks and drivers are available.

Read More →

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

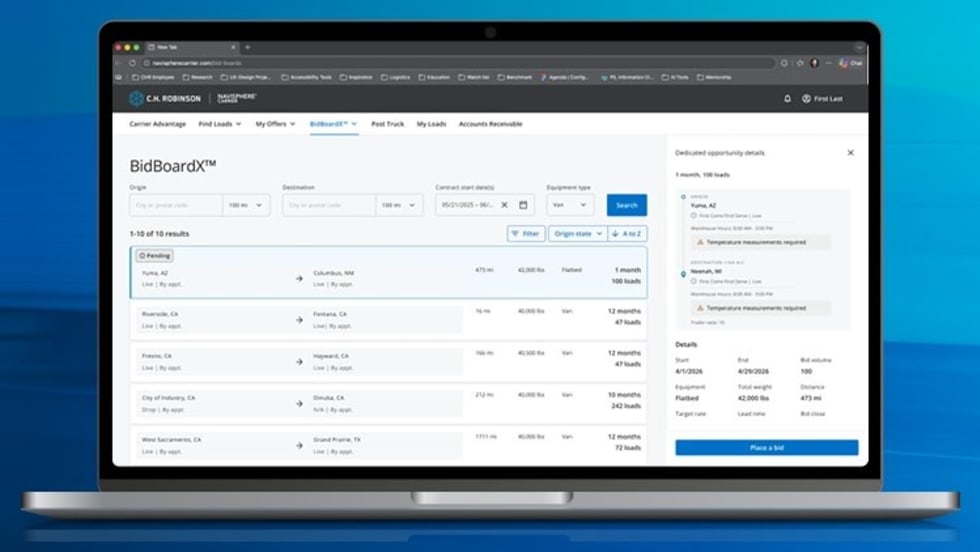

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →

Import Cargo Volume to See Year-Over-Year Gain Again in June, Then Remain Below 2025 Levels Into Fall

After July, the report predicts a weakening in import volume as consumer uncertainty remains high and the impact of increasing inflation takes its toll.

Read More →