Higher Trailer Build Forecast, Class 8 Backorders Easing

ACT Research analysts expect higher trailer build numbers in 2023 and 2024, but there are clouds, while Class 8 2023 build backlogs will continue to decline, as the rebalancing of the freight market is being drawn out.

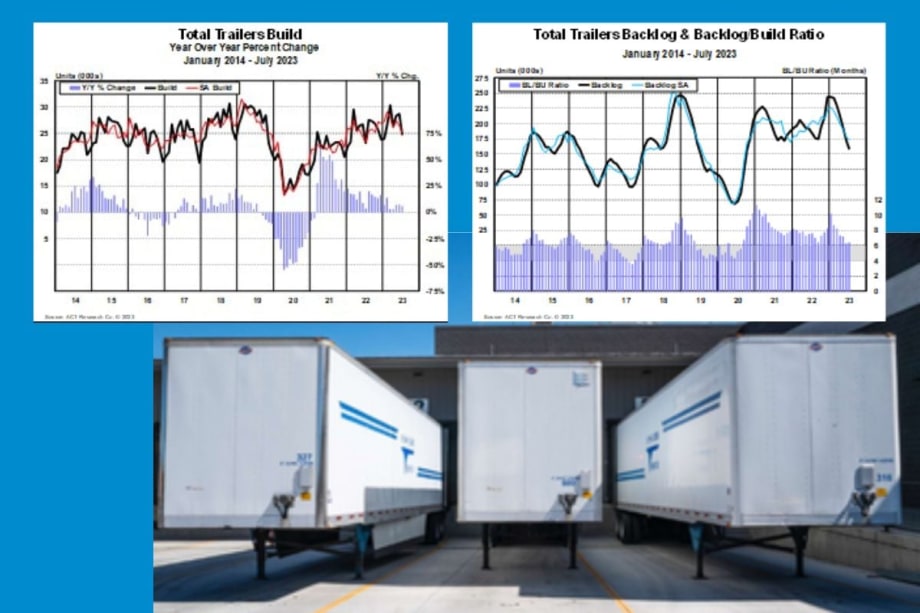

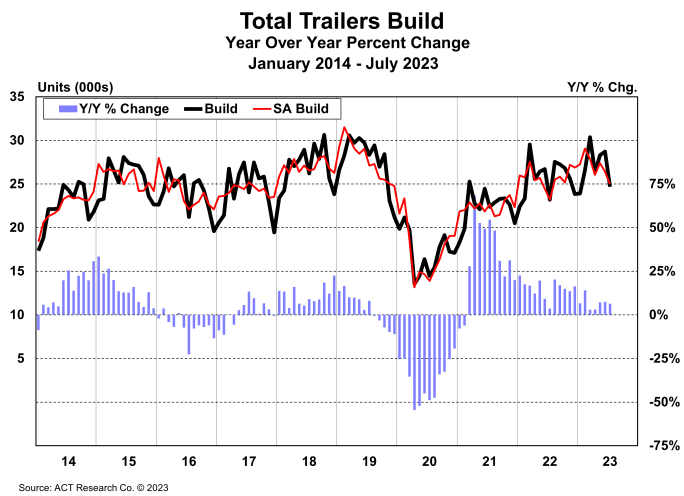

According to ACT Research’s Trailer Components & Raw Materials Forecast, the US trailer forecasts for 2023 increased during the past three months.

Source: ACT Research/HDT Illustration

ACT Research has raised its 2024 trailer forecast, reflecting higher build in 2023 and 2024.

Source: ACT Research

ACT Research analysts expect higher trailer build numbers in 2023 and 2024, while Class 8 2023 build backlogs will continue to decline amidst the continuing rebalancing of the U.S. freight market.

ACT’s U.S. trailer forecasts for 2023 increased during the past three months. The 2024 trailer forecast is now higher, reflecting higher build in 2023 and 2024, with the economy continuing to outperform expectations, higher GDP and freight forecasts, and more normalized supply chains.

“Build in the last three months (May-July) of 81,700 units was 7% higher than the same three-month period last year, while net orders of 26,300 trailers were about 58% lower for the May-to-July-2023 period, versus the same three months in 2022,” said Jennifer McNealy, director-CV market research and publications at ACT Research.

She also noted order backlogs at 157,300 units were 15% lower than the 184,900 units pending production last year.

As part of ACT Research’s recent trailer-maker survey, analysts asked about 2024 orderbook openings and dealer inventory levels.

“Based on responses, it appears that about 35% of the industry’s Q1’24 books have opened, with limited slots available beyond that,” said McNealy. “Regarding dealer inventories, answers were product dependent, with generalist trailer levels higher than specialty trailer inventory levels.”

Order backlogs for trailers are 15% lower than a year ago, but still high.

Source: ACT Research

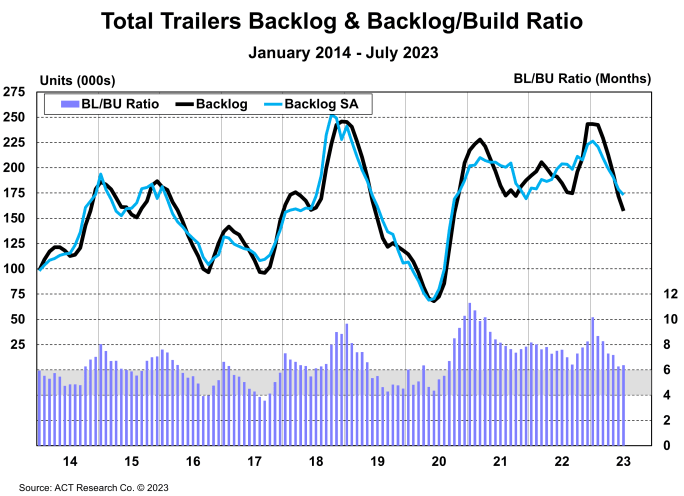

Class 8 Orders

On continued strong build rates and seasonally weak order volumes, July’s North American Class 8 backlog fell by 11,632 units to 163,576 units. At 5.9 months, the nominal backlog-to-build ratio remains comfortably healthy into year end, according to ACT Research’s latest State of the Industry: NA Classes 5-8 report.

According to Kenny Vieth, ACT’s president and senior analyst, “With over 90% of the current backlog scheduled for build in 2023, Class 8 backlog is likely to continue to decline until 2024 orderboards are opened.”

On medium-duty, he continued, “The Classes 5-7 backlog slipped 1% to 116,890 units in July. The BL/BU ratio fell to a still elevated 4.6 months on the smaller backlog and higher daily build rate.”

With the current backlog front-end loaded, Class 8 truck orders will receive heightened attention as 2024 orderboards are opened in the next few months, said ACT Research.

Source: ACT Research

Regarding July’s Class 8 build rate, he noted, “Build slightly exceeded OEM build plans, but remainder of the year guidance was trimmed slightly. Notably, Class 8 build and retail sales were virtually identical last month, keeping inventories at relatively lean levels. Tight inventories are a reminder that pent-up demand continues to be worked off in 2024.”

Class 8 orders rose 41% y/y to 15,573 units. On a seasonally adjusted basis, orders were flat sequentially at 20,100 units. Classes 5-7 orders rose 22% y/y against 2022’s easiest order comp to 16,736 units.

Vieth concluded. “July is the worst month of the year for both Classes 5-7 and Class 8 orders. While vacations are a likely factor, the bigger ones are systemic. As is often the case, the current year backlog is full. At the same time, the OEMs have typically not yet opened orderboards for next year. Hard to book an order in those circumstances. With the current backlog front-end loaded, orders will receive heightened attention as 2024 orderboards are opened in the next few months.”

Freight Market Rebalancing

The rebalancing process in the U.S. freight market is being drawn out by reluctance to part with workers and significant private fleet capacity expansion, even as pressure on fleets worsened this month as diesel prices spiked, according to the latest release of the ACT Research Freight Forecast.

“Although seasonality remains loose and demand soft, spot market dynamics have begun to shift since the end of operations at Yellow on July 31," said Tim Denoyer, ACT Research’s vice president and senior analyst. "While this is a game-changer for [less-than-truckload] rates, so far, the truckload market is still loose enough for rates to be largely unaffected. We see the impact growing over time, along seasonal patterns."

ACT reported the publicly traded for-hire fleets reduced their collective tractor count by 3% in the first half of the year, but Class 8 tractor sales and production are still near maximum levels, adding considerably to the Class 8 tractor fleet. Private fleets are still growing and pulling freight from the for-hire market.

“Class 8 orders will be very interesting over the next several months and, in our view, pivotal to setting the market tone for 2024,” Denoyer concluded.

More Equipment

Atlas Expands Kodiak Driverless Truck Fleet in Permian Basin

Atlas Energy Solutions is expanding autonomous frac sand hauling in the Permian Basin with a second load-out location and plans for 100 driverless trucks by mid-2027.

Read More →

Putting Mack’s Command Steer to the Test

A test drive of Mack’s Command Steer active steering system evaluates how it can make truck driving easier and less tiring.

Read More →

Mack, Volvo Expand DEF Derate Software Updates

The updated software gives Mack and Volvo truck owners more time to address DEF-related issues before the engine derates or the vehicle goes into reduced-speed inducement, following new EPA guidance.

Read More →

Rush, MCT Team Up to Grow Refrigeration Service Network

The joint venture will operate MCT's network of Carrier Transicold dealerships and mobile service locations, with the companies promising greater service capacity and uptime for refrigerated fleets.

Read More →

Cummins Adjusts 2027 Engine Rollout After EPA Proposal

The engine maker will gradually introduce its new Model Year 2027 diesel engines while continuing to offer current models during the transition, citing the EPA's proposed emissions rule changes.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Peterbilt 589 Spotlight: A Close Look at a Custom Working Truck [Video]

There's more to this customized Peterbilt Model 589 and Great Dane refrigerated trailer than chrome and stainless (although there's plenty of that too!) A veteran driver explains the design choices and practical features behind this working truck.

Read More →

Continental Expands Retread Lineup With New ContiTread HDL 5 EP

New long-haul drive retread is designed to improve fuel efficiency, extend tread life, and lower fleets' cost per mile.

Read More →

EPA Proposal Could Ease 2027 Truck Costs and Buying Uncertainty

The proposal doesn't change the tougher NOx standard, but it would revise key implementation requirements that manufacturers say have driven up costs and complicated fleet purchasing decisions.

Read More →

Cummins, Paccar Ease DEF Derates After EPA Guidance

Updated diesel engine software gives truck operators more time to address emissions-system issues while staying compliant with EPA emissions standards.

Read More →