The 34th annual State of Logistics Report, entitled “The Great Reset,” found that U.S. supply chains responded to the global volatility over the past two years by transforming supply chain networks to improve resiliency against future disruption.

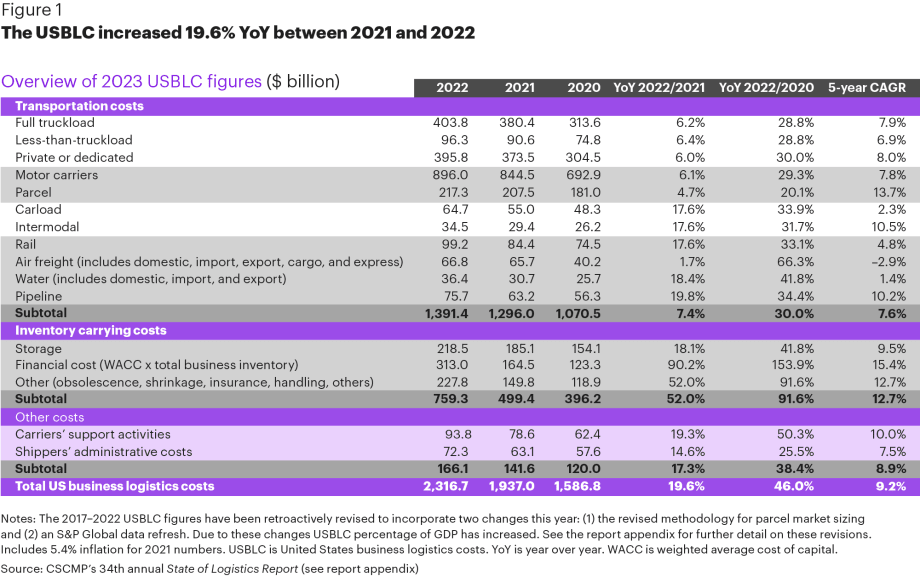

The USBLC increased 19.6% from 2021 to 2022. Motor carriers increased 6.1% over the same period, but 29.3% from 2020.

Source: CSCMP's State of Logistics Report

6 min to read

The 34th annual State of Logistics Report, entitled “The Great Reset,” found that U.S. supply chains responded to the global volatility over the past two years by transforming supply chain networks to improve resiliency against future disruption.

Produced annually for the Council of Supply Chain Management Professionals by global consulting firm Kearney and presented by leading third-party supply chain provider Penske Logistics, the annual report offers a snapshot of the American economy via the lens of the logistics sector and its role in overall supply chains.

Ad Loading...

The report, available here, is a comprehensive compilation of leading logistics intelligence from around the world and shines a spotlight on industry trends and key insights on ever-evolving supply chains across a number of sectors.

While last year’s report highlighted the need to get back in sync in the wake of the COVID-19 pandemic, the 2023 version focuses on how logistics operations can build long-term resilience in an effort to best serve customers through a variety of distribution channels.

"As the logistics sector moves forward from years of supply chain challenges and bottlenecks, our report shows that now is the time to begin thinking seriously and proactively when it comes to building strategic capacity," noted Balika Sonthalia, senior partner at Kearney and co-author of the 2023 State of Logistics Report. Although the market has swung back in shippers' favor — to the detriment of carriers — we cannot emphasize enough the importance for all industry participants to begin planning for geopolitical tensions, cybersecurity threats, climate change, related natural disasters, slowing e-commerce growth, and global recessionary factors."

Ad Loading...

Key Findings

Key report findings for 2023 include:

A key report statistic, U.S. business logistics costs, shows an increase. The U.S. Business Logistics Cost index (USBLC) now stands at a record $2.3 trillion (compared to $1.85 trillion last year), representing 9.1% of national GDP—the highest percentage of GDP ever.

While consumers are continuing to return to stores, e-commerce sales are not slowing down. In 2022, the U.S. e-commerce market grew by 8%, to $1.03 trillion (the previous year it was $871 billion). It is now 14.5% of the entire U.S. retail market.

Third-party logistics providers are investing more capital into their technology offerings, as opposed to shippers. Respondents indicated that 96% of 3PLs have migrated to the cloud (shippers indicated 86% of them have), while 80% of 3PLs are investing in IoT (77% for shippers).

The reshoring movement continues. For a number of businesses, reshoring has gone from a strategic possibility to a market reality. According to the Kearney Reshoring Index, American imports of Mexican manufactured goods have grown by 26% (dating back to spring 2020).

The Great Reset

Sonthalia explained, in a press briefing, that the report found that moving past disruptions such as Covid-19, a freeze in Texas, and other global macroeconomic events, the fundamental relationships between shippers and carriers continue getting back “in synch” and supply chain executes are addressing structural costs to strengthen their foundations.

She pointed out that since the pandemic hit in 2020, the USBLC has continued to rise steadily. The study period noted the second-highest growth in USBLC in a decade and, according to Sonthalia, the USBLC is the highest percentage of the GDP ever seen.

Other critical factors Sonthalia noted include:

Ad Loading...

19.6% year-over-year USBLC growth from 2021 to 2022

46% USBLC growth from 2020 to 2022

USBLC was 9% of 2022’s $25 trillion GDP.

“I believe with the corrections that are taking place through all the transportation categories, we expect to see a significant return to the levels that we are used to seeing of USBLC see as a percentage of the GDP,” she explained. “However, with the lingering shadow of inflation, we see prices remain elevated in certain categories and routes. And a lot will depend on the monetary policy.”

Cost by Logistics Mode

The report breaks down each logistic mode contained within the USBLC equations.

Changes in transportation mode costs noted were:

Motor carriers mode grew 6.1% as margins were threatened by lower rates and high resource costs, with smaller carriers that were reliant on the spot market under more acute pressure, according to the report.

Parcel mode increased 4.7% as revenues increased as major deliverers shifted toward a focus on profitability over volume.

Rail mode increased 17.6% as Class I railroads saw increases in operating income and total revenue, however rising costs undermined operating ratios.

Air freight mode increased by 1.7% as demand declined and capacity surged as passenger flights resumed and new planes entered service.

Domestic water mode increased 18.4%, despite a projected sharp decline in ocean carriers’ profits.

Ad Loading...

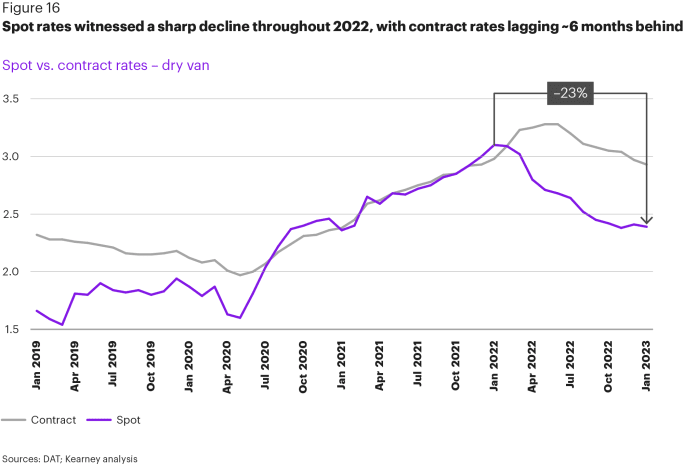

Spot rates declined 23% year over year from 2021 to 2022.

Source: CSCMP's State of Logistics Report

Motor Carrier Capacity

“In 2022, we saw that demand was relatively unchanged, while there was an increase in available capacity because demand had not significantly increased,” Sonthalia said. “This also reflects the concerns that shippers had about inflation, rising interest rates, and overstock inventories, which overall resulted in the small change we saw on demand.”

The report looked at the DAT Freight & Analytics dry and load-to-truck ratio, and Sonthalia pointed out that the dry and load-to-truck ratio is at the lowest since it has been in June 2020, which is a signal of the level of capacity that's available in the market.

“With improving service levels and falling in the spot rates, we are seeing that shippers are thinking about turning to the spot market more than the contractor market. That said, keeping an eye on strategic relationships is always important and not dropping the ball on being a shipper of choice is important,” said Sonthalia.

The report also noted a greater spread between spot and dry rates than in previous years, and Sonthalia said that trend will continue in the coming months. From January 2022 to January 2023, the spot rate declined 23%.

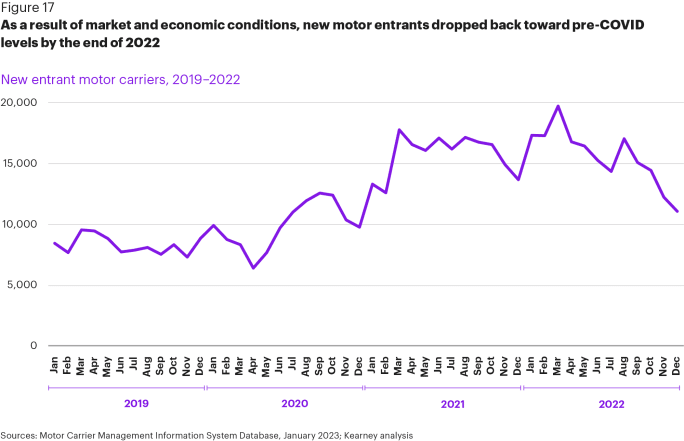

New motor carriers increased in recent years but then declined sharply back to pre-pandemic levels at the end of 2022.

Source: CSCMP's State of Logistics Report

Motor Carrier Registrations

The report explained how the number of new carrier registrations declined significantly during the pandemic, but more recently has skyrocketed. With rates going down, smaller carriers who were once the beneficiaries of a volatile spot market were forced to make decisions to protect themselves by switching to contract, joining a larger carrier, or leaving, the report stated.

Ad Loading...

“Now we are kind of seeing correction going back to the pre-pandemic levels,” Sonthalia added.

Takeaway

Growth in freight is slow, but it is still growing. Sonthalia pointed out the even though road freight overall has lost some momentum when compared to 2020 and 2021 growth periods, it still grew by 6.1% year-over-year into 2022.

“We are committed to supporting this report with timely and frequent ongoing commentary that ensures relevance throughout the year ahead,” said Mark Baxa, CSCMP president and CEO. “After reading the report cover-to-cover, I encourage you to ask, ‘what’s different, and do I understand the course of action to ensure maximum logistics success on the road ahead?’ Whether you are the senior leader or an entry-level analyst, you have decisions to make that will make a difference in your supply chain’s performance.

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Fleet Refresh enables refrigerated fleets to replace aging transport refrigeration units instead of entire trailers, while adding Lynx Fleet telematics and BluEdge service coverage.