Want more? Logistics in 2022: Technology Further Rides to the Rescue

State of Logistics: Supply Chains Seek to Get in Sync

"The logistics sector has begun to enable changes which should benefit manufacturers, retailers and consumers alike," says the new State of Logistics Report — but it may be a bumpy road to get there.

June 21, 2022

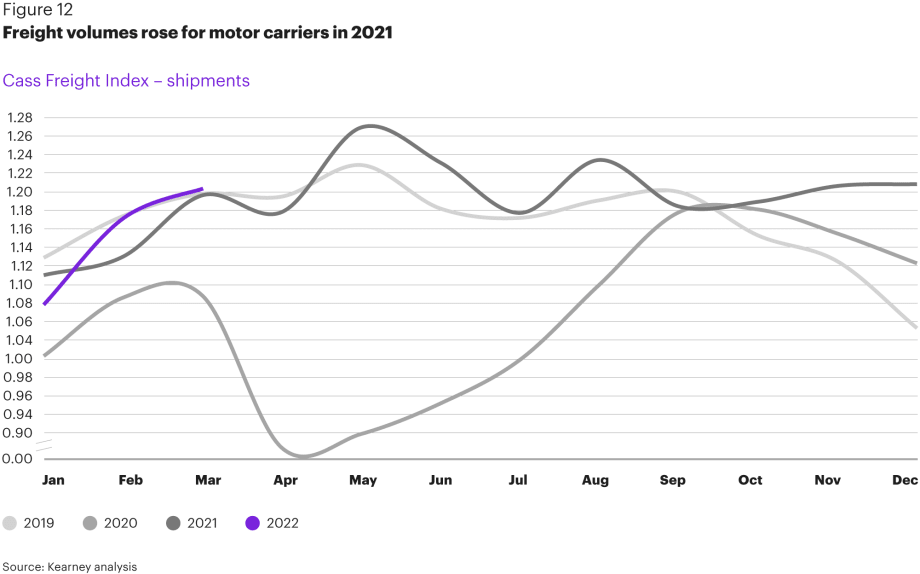

Freight volumes for motor carriers rose in 2021.

Source: State of Logistics Report

6 min to read

U.S.-based supply chains remain “out of sync” in 2022, according to the latest annual State of Logistics Report. On the plus side, the report indicates that the logistics sector has begun to adapt to short-term changes, doing so in a way that may well reveal long-term solutions to the disruptions afflicting supply chains. But there are challenges ahead for both fleets and shippers.

The report found that U.S. business logistics costs climbed in 2021 by 22.4% to $1.85 trillion, representing 8% of 2021's $23 trillion GDP. By contrast, last year’s State of Logistics Report saw those costs fall by 4%, driven down by the impact of the pandemic on business and consumer spending.

The 33rd annual State of Logistics Report, titled “Out of Sync,” was released June 21 by the Council of Supply Chain Management Professionals. Presented by Penske Logistics, the report is authored each year by consultancy firm Kearney.

"It's not surprising that we are continuing to see ongoing disruptions related to the pandemic, but the scope and impact of disruptions continue to weigh heavily on the minds of logistics providers — as they do for all companies contributing to the U.S. economy,” said Balika Sonthalia, partner at Kearney and lead author of the 62-page report.

“What is notable for 2021, however, is that the logistics sector has begun to enable changes which should benefit manufacturers, retailers and consumers alike,” she continued. “We're especially heartened by the progress the sector has made in rebuilding supply chain resilience via multi-shoring, automation, and optionality in last-mile distribution. This will also improve customer service and bring efficiencies for all parties."

Logistics Challenges Ahead

However, that positive outlook is balanced in the text with a gimlet-eyed view of what’s at stake.

“There are certainly more challenges ahead. Barely into the new year, Russia invaded Ukraine and fuel costs spiked; China Section 301 tariffs were set to expire or perhaps renew mid-summer 2022; and the U.S. Fed started a round of aggressive rate hikes.

“As this report goes to print in June,” its five authors advise, “prices for road, air, and ocean have declined from all-time highs with demand taming, but oil prices are holding far above historical averages, and supply chains remain vulnerable to COVID flare-ups. The longed-for relative certainty and stability have yet to appear.”

Key report findings for 2022 include:

Business inventories dropped to near-historic lows, but the costs associated with storing, handling and financing these items rose considerably. Inventory-carrying costs rose by 25.9% in 2021, and transportation costs jumped 21.7%. This led to uneven supply chains and inconsistent product availability for consumers (both in-person and online).

Efforts to increase “multi-shoring” are expected to accelerate. Companies are seeking to have operations move closer to the U.S. so they can respond faster to fluctuating market demands.

Residual challenges of the pandemic remain, with some disruptions continuing to deliver damaging effects on capacity.

Last-mile delivery volume is trending upward. The 2022 report notes that e-commerce sales grew 10% last year (to $871 billion), accounting for 14% of U.S. retail sales.

Trucking freight continues to see more volume and opportunities. With road freight accounting for the largest segment of the U.S. supply chain spend, it expanded by 23.4%, to a lofty $831 billion spend.

“Turbulent circumstances and rising cost pressures were the story of 2021 in all major logistical sectors,” the authors stressed. For example, air freight costs increased by 19.2%, as demand continued to exceed supply throughout the year. Meantime, rail costs in the U.S. were up 18.8% overall, but network speeds and service levels worsened due to the same kinds of disruptions seen by other modes, including port congestion, chassis shortages, and tight labor markets.

With the logistics segment still facing the headwinds of disruption, shippers increasingly turned to third-party logistics (3PLs) “to address scarce capacity, supply chain complexity, service disruptions, and surging customer demands.”

2021 was a good year for third-party logistics providers.

Source: State of Logistics Report

High Freight Rates Prompt Shippers to Turn to 'Captive' Fleets

Road freight — the biggest segment of U.S. logistics expenditure — climbed high in 2021, growing by 23.4% to $831 billion, and freight rates were a boon to carriers.

“Carriers that had cut or delayed capacity early in the pandemic went into overdrive, spending at unprecedented levels to attract new hires and buy new trucks,” the report finds.

In addition, “shippers worried about lost sales proved more than willing to pay ever-increasing spot rates. This sustained high demand as high prices powered profits, with top U.S. carriers seeing profits rise by 50%, 100%, or more even as their own costs of operation continued to surge.”

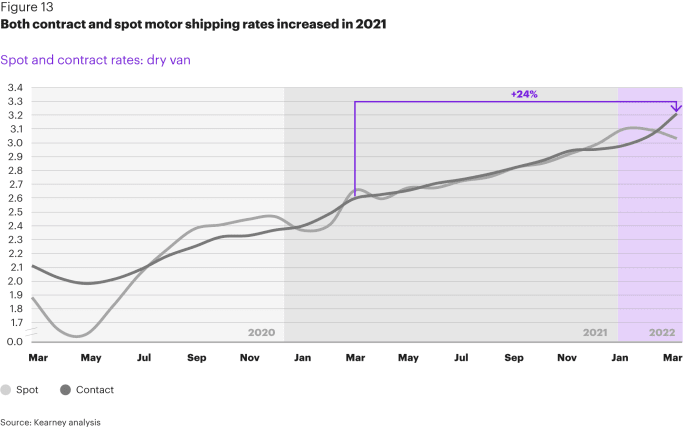

While spot and contract rates both rose in 2021, the first part of 2022 saw spot rates start to soften.

Source: State of Logistics Report

But, just as the road rises, so it goes downhill eventually. Or, in the authors’ words, “Troubles may be looming.” They explain that shippers “miffed by low service levels” increasingly developed their own “captive” truck fleets as a more reliable alternative, which also become more affordable. When shippers increasingly turned to private and dedicated fleets, they had to pay more for their drivers and trucks, which drove captive fleet costs up 39.3%.

What’s more, the drop in demand and rates underway in the second quarter of 2022 will squeeze carrier margins. Andy Moses, SVP sales and solutions at Penske Logistics, observed, “Captive fleets rose to the occasion as they became more valued, driving an accelerated adoption that remains with us today. We’ve seen shippers that have gone 10 years without a private or dedicated fleet get into them.”

Overall truck freight also was boosted by the “explosive growth” of last-mile delivery volumes, “driven by the increased popularity of work-from-home and other social-distancing behaviors.” E-commerce grew by 10% to $871 billion — 13% of all U.S. retail sales.

“The parcel sector was a direct beneficiary, growing by 15.6% and turning in the highest five-year compound annual growth rate of any of the cost components, at 11.4%. However, there is evidence that e-commerce growth has begun slowing a bit as shoppers return to stores.”

Reshoring, Nearshoring, and 'Shippers of Choice'

The authors argue that “the expansion of capacity and the development of new value propositions are among the most urgent imperatives for motor carriers.” The report holds that market forces and ongoing supply chain challenges “should fuel sustained motor carrier growth and create numerous opportunities for trucking networks to evolve.”

Of note is the authors’ view that “reshoring and nearshoring could raise demand for North American regional and long-haul trucking substantially.” They point to a March 2021 Kearney survey of U.S. manufacturing executives that found that 41% had reshored at least a portion of their manufacturing operations to the U.S. over the past three years, while another 22% said their company plans to reshore some manufacturing within the next three years. It was noted that in personal interviews for that report, “some executives voiced a strong intent to reduce dependence on manufactured imports from any one country, particularly China.”

As for value propositions, going back to the future is a significant one. The report explains that many shippers are seeking to become a “shipper of choice” by establishing partnerships with carriers and “offering customers something resembling a truly turnkey logistical service.” The authors recommend shippers “begin by initiating more in-person meetings to strengthen their personal bonds with carriers, and by engaging in mutual site visits to develop a better shared understanding of what shippers need, and what carriers might provide.”

Truck Drivers Wanted

But there’s no value, let alone any freight getting hauled, if there are not enough drivers. While the report concedes that “the future of self-driving trucks is not a question of if, but when,” more immediately the authors encourage motor carriers to invest more proactively in recruiting, training, and compensating drivers. “As those efforts take hold, they can move to retain drivers by offering more flexible scheduling, larger appointment-time windows, better driver facilities along long-haul routes, and quicker payment terms.”

In one statement, the authors neatly sum up the report’s theme and findings: “Relative stability may or may not return, so the logistics sector must invest now in controlling what factors it can.”

More Fleet Management

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →

July Imports Poised to Set Container Record

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

Read More →

HDT Announces 2026 Truck Fleet Innovator Finalists

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Read More →

Van Spot Rates Top Contract Rates for First Time Since 2022

There’s more good economic news for the North American trucking industry according to the latest Truckload Volume Index report from DAT.

Read More →

Carrier Transicold Extends Refrigerated Trailer Life

Fleet Refresh enables refrigerated fleets to replace aging transport refrigeration units instead of entire trailers, while adding Lynx Fleet telematics and BluEdge service coverage.

Read More →