More from Avery Vise:

Pent-up Demand Bolsters Industrial Freight Volumes

Industrial production and manufacturing output are strong. FTR's Avery Vise explores what this could mean for industrial freight volumes.

by Avery Vise, FTR

April 26, 2022

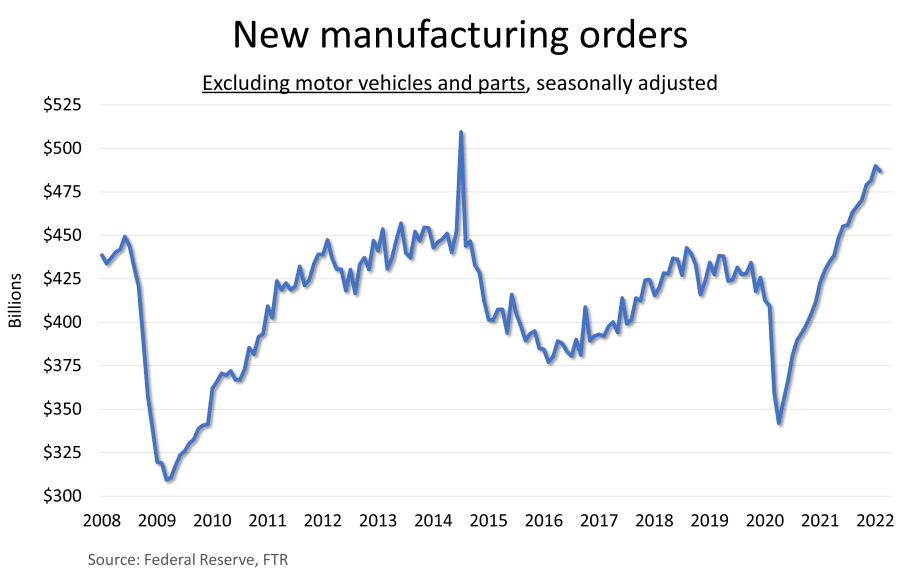

Manufacturing output excluding motor vehicles and parts was 4.6% ahead of February 2020, seasonally adjusted, but new orders for manufactured goods in the latest month were 19% ahead of February 2020.

Source: FTR

3 min to read

Over the past several months, FTR’s Hotline articles for HDT have mostly addressed the consumer sector, including the freight risks associated with inflation and inventories. While we have reasons to be concerned about the potential for weaker consumer spending, we have yet to see data indicating that spending truly is falling.

Some analysts have interpreted the cooling of spot market metrics for dry van and refrigerated as a sign that consumer spending is down. However, that cooling appears to be linked mostly to a recovery in capacity among larger truckload carriers, which is serving to shift volumes back to the contract market and away from the spot market.

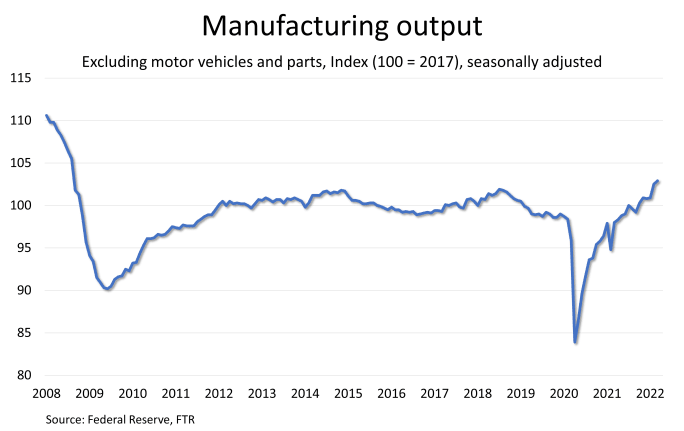

Manufacturing output is the strongest since August 2008.

Source: FTR

Freight associated with the industrial sector is not without risks, but industrial activity appears to have a much higher floor than the consumer sector. Industrial production and manufacturing output are strong. In March, the Federal Reserve’s industrial production index was at its highest level ever, and that data dates to 1919. Manufacturing output is the strongest since August 2008.

Of course, strong production is no guarantee of continued strength. After all, August 2008 was the month before the financial collapse that led to the worst period of the Great Recession. Manufacturing output plunged nearly 16% until it bottomed out in June 2009.

Unlike the situation in 2008, however, the manufacturing sector faces huge pent-up demand due to supply chain and labor challenges. If you have tried to buy new trucks over the past year or so you probably found that it takes far longer than usual. Everyone knows about the global semiconductor shortage that is significantly curtailing production of cars, light trucks, SUVs, and, of course, heavy-duty and medium-duty trucks.

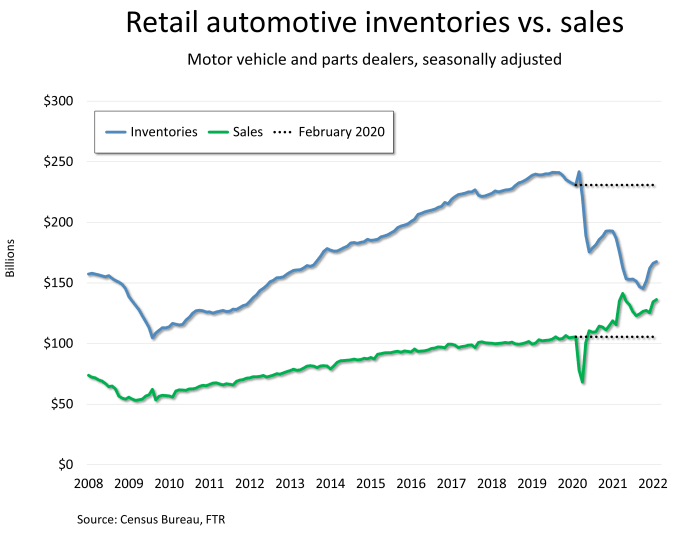

Despite some recent improvements, retail inventories of motor vehicles and parts are still more than 27% below pre-pandemic levels even though vehicle and parts retail sales are running about 29% ahead of pre-pandemic levels. Even if sales fall off, auto makers still will need to push production as much as the semiconductor supply will allow for at least the rest of this year and probably longer.

Although the supply chain issues for vehicle production might be easier to isolate than in the rest of manufacturing, the entire sector is experiencing the same basic problem: Higher demand than production can satisfy. Manufacturing output excluding motor vehicles and parts was 4.6% ahead of February 2020, seasonally adjusted, but new orders for manufactured goods in the latest month were 19% ahead of February 2020.

Auto makers will need to push production as much as the semiconductor supply will allow for at least the rest of this year and probably longer.

Source: FTR

Some of that manufacturing demand obviously would disappear if the broader economy stalls, but a significant of that production would be needed to replace worn-out or obsolete equipment. The broader manufacturing sector is not unlike commercial vehicles. Demand for additional trucks and trailers might fade, but the industry still needs to replace older equipment.

For more information, visit www.FTRintel.com/HDT or call FTR at 888-988-1699. This article appears in the May 2022 issue of Heavy Duty Trucking.

Subscribe to Our Newsletter

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →