Related: How Will Election Affect the Quagmire in Washington?

Indicators Point to Strengthening Trucking Market

COVID-19 brought on the worst recession in U.S. history, but the recovery is underway and economic conditions should return to pre-COVID levels by late next year.

by James Menzies, Today’s Trucking

September 16, 2020

Source: ACT Research

3 min to read

COVID-19 brought on the worst recession in U.S. history, but the recovery is underway and economic conditions should return to pre-COVID levels by late next year.

Jim Meil, industry analyst and principal of ACT Research, pointed out the economic recovery has been strong in the third quarter, after the bottom fell out and the U.S. posted its worst Q2 ever. The recovery is taking place around the globe, with exceptions being Japan and Mexico. However, until a COVID-19 vaccine is discovered, or herd immunity achieved, Meil said “the risk remains high going forward.”

The freight markets were somewhat protected from the economic disaster, as goods continued to move while the services sector tanked.

Overall consumer spending fell about 20% in April, but has climbed back to just 4.5% off pre-COVID levels from January. In fact, durable goods spending on products such as cars and auto parts are actually now above January levels, Meil said, as are spending on furniture, appliances and household goods. But spending on transportation (ie. flights) and recreational services (concerts, bars, etc.) is still down 25% and 36%, respectively.

“The big story here is, if people are spending their money on stuff instead of services, that actually goes into the sweet spot for truck transportation,” Meil pointed out.

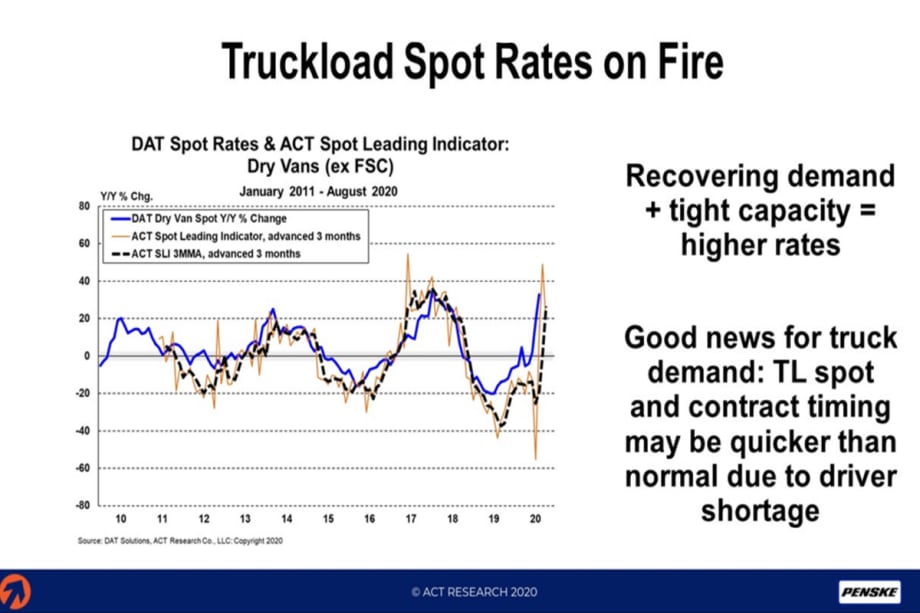

Tim Denoyer, ACT Research’s vice-president and senior analyst, pointed to a bright future for trucking in the near term. He said dry van spot market rates are at record highs, even though volumes are flattish year-over-year. Improving rates are being driven by a tight driver market.

“There are too many drivers on the couch,” he said, pointing to generous federal government subsidies that, when combined with state unemployment benefits, could see the unemployed fetching about $1,000 a week. That has disincentivized some drivers from returning to work, and the shortage is exacerbated the closure of training schools that churn out new CDL holders, and retirements by older drivers looking to protect their health. Denoyer said it could be 2021 before drivers return en masse.

Source: ACT Research

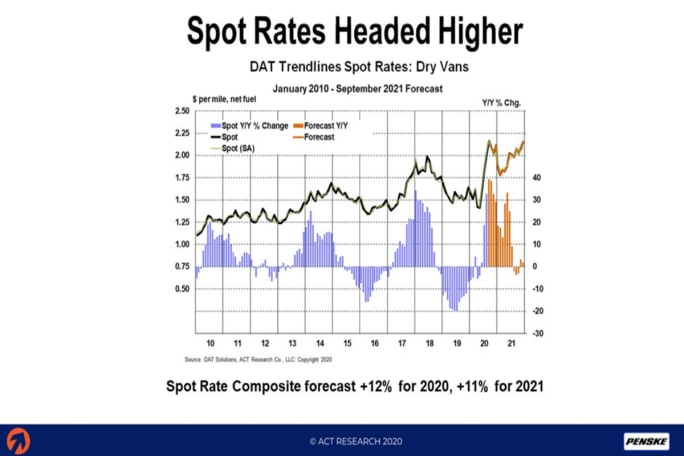

In August, dry van spot market rates in the U.S., net of fuel surcharge, were up 33% year-over-year, and up by about 39% so far in September.

“The short-term outlook is very positive,” Denoyer said. This should eventually translate into higher contract rates, as well.

Kenny Vieth, president and senior analyst with ACT, said for every 2% increase in spot market rates, contract rates tend to rise about 1% five months later.

“If the economy doesn’t fall apart from here, this is an extremely bullish sign for carrier profitability,” Vieth said.

Citing rail volumes, Denoyer said the freight recession that stretched back seven quarters is ending. Import volumes at U.S. West Coast ports are high, and intermodal volumes are strengthening as those goods are pushed inland. Intermodal spot market rates have gone “parabolic,” said Denoyer, with rail capacity effectively sold out for the remainder of the year, which should further boost trucking rates through the holiday shipping season. Retail inventories are being replenished, and for them to return to traditional levels would require about US$200 billion in goods to be restocked, or about a 3% boost to freight volumes over the next six months.

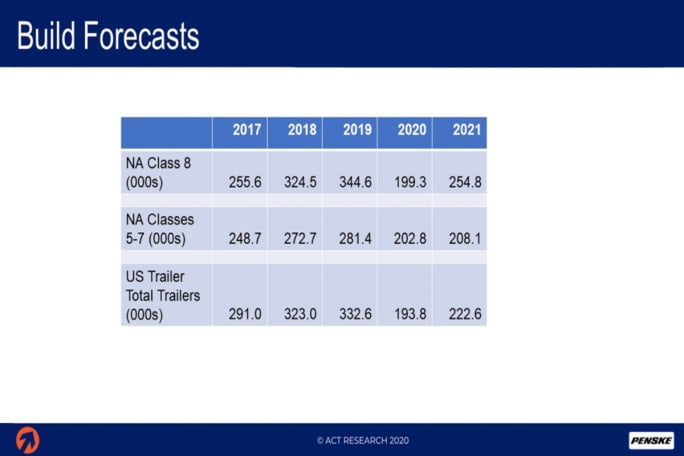

Vieth pointed out Class 8 order activity is picking up, but there remain about 5% more trucks in the market than needed to meet current freight demands. A lack of drivers is what’s driving the capacity shortage and forcing up rates.

“There’s an extremely strong case to be made for the driver shortfall to continue through 2021,” Vieth said. ACT is forecasting the North American Class 8 build to total 250,000 units in 2021, reflecting a more normalized year.

James Menzies is the editor of Today's Trucking, where this article originally appeared. This content was used with permission from Newcom Media as part of a cooperative editorial agreement.

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →