Related – Report: 3PL Market Moving Downward

Logistics Costs Climb as Supply-Chain Capacity Tightens

With much thanks to the booming economy, logistics costs incurred by U.S. businesses jumped 11.4% last year, reaching $1.64 trillion– or 8% of the $20.5 trillion gross domestic product of the entire United States in 2018.

June 18, 2019

A.T. Kearny's Michael Zimmerman discusses latest State of Logistics Report at National Press Club in Washington, D.C.

Photo: CSCMP

7 min to read

With much thanks to the booming economy, logistics costs incurred by U.S. businesses jumped 11.4% last year, reaching $1.64 trillion-- or 8% of the $20.5 trillion gross domestic product of the entire United States in 2018.

That’s per the Council of Supply Chain Management Professionals’ 30th annual State of Logistics Report, which was introduced June 18 at the National Press Club in Washington, D.C. Sponsored by Penske Logistics, the report is authored each year by consultancy A.T. Kearney.

The report is subtitled “Cresting the Hill,"a description that reflects that the “logistics industry is a new crossroads,” Michael Zimmerman, A.T. Kearney partner and co-author of the new report said in a press release. “It has overcome a tough and exhausting year. Now, demand has softened and growth is in doubt— but not to the point where a steep decline is visible.”

“At the crest of this hill, we see both hope and evidence of a better road being taken,” the report’s authors write. “Leading shippers looking to control logistics costs have leaned more in the direction of constructive engagement and innovation than ever before, and carriers have been pleased with the new collaboration while themselves opening up to startups and new technologies for novel solutions to transportation challenges.”

The report states that supply chain capacity is now so tight, “a number of major companies have reported in their Securities and Exchange Commission filings that they exceeded their 2018 supply-chain budget spending,” noted CSCMP.

In a nutshell, what happened last year was that rising economic activity fueled a strong job market and pushed up wages, which motor carriers and warehouse operators passed on to shippers as higher prices.

What’s more, shipping activity was “especially intense” in the fourth quarter, as American business began dealing with heightened U.S.-China trade tensions and the business inventory here reached an all-time high of $2.75 trillion, as businesses brought in goods ahead of expected tariffs. That drove up inventory carrying costs to where they eclipsed increases in transportation costs.

As many economic headlines have shouted of late, the report found that the “growth of e-commerce— in both volume and scope— helped fuel modes such as motor carrier, intermodal, third-party logistics, air freight, and freight forwarding as the rest of retail sought to rise to the occasion. Supply could not keep up with booming demand.”

The response to rising demand varied “by situation and strategy, but included shipper of choice programs, increasing captive, fleets, forward-deploying to warehouses, and crafting longer-term agreements.”

Why logistics costs are up

The report found that logistics costs are rising due to these key factors:

The retooling of supply chains to accommodate more e-commerce sales (online purchasing increased by 14.2% last year), including a spike in the need for smaller, more costly warehouses.

“Extremely high” utilization of existing truck fleets limits available freight capacity and drives up rates.

Increasing driver hours-of-service regulations are “causing smaller trucking firms to cease operations, consolidate or be acquired by larger transportation companies.”

Tight U.S. labor market is driving up wages for truck drivers and warehouse workers. Attracting and retaining labor in general “remains challenging” for transportation and logistics companies.

The report not only reveals the cost of logistics in the U.S., said Rick Blasgen, president and CEO of CSCMP, it also “discusses technology and other forward-thinking applications for leaders to use as they improve their overall supply chain performance.”

CSCMP said these innovations especially are driving development of state-of-the-art supply chains:

“Silicon Valley has devoted time, energy and resources to automation and robotics with inventions like automated trucks and automated warehouses.”

Vehicle electrification will “lead the way to a more sustainable transportation network.”

The coming upgrade to a 5G communications network in the U.S. will improve the execution of logistics operations; the planning and management of them; and the high-security encryption needed to protect them.

Seeking new logistics solutions

Diving into the report, there’s lots of food for thought for truck fleet operators to munch on while crunching their numbers as the second half of 2018 looms ahead.

“As we predicted over the last two years,” say the authors, “uncertainty became a steep grade. Carriers and shippers faced a choice: to either slog through it with conventional tactics or engage with opportunities to do something different, something better. More and more are trying the latter approach and are reaping the rewards. As this latest hill is crested and the players in the industry can see forward to how the next ones will test them, the rewards will go to those that seek bold new solutions.”

Among the “remedies that are being adopted today” explored in the report are:

Implementing shipper of choice programs “to improve the carrier experience and the efficient deployment of their assets.”

Investing in position-sensing technologies that enable “more effective allocation and utilization of assets by logistics operators and the software that supports them.”

Deploying artificial intelligence and machine-learning algorithms to make brokerages more efficient at serving their customers and matching drivers to loads

Advancing “collaborative optimization techniques” in logistics sourcing and network design that “fully leverage the power of early carrier and 3PL consultation.”

Signing “collaborative contracts between shippers and carriers seeking to increase the sustainability and utilization of the assets in use.”

Using “shared economy concepts and applications that make better use of last-mile drivers and contract logistics spaces."

The authors see last year as a very good year for truckers. “Carriers enjoyed a higher rate environment in 2018, driving improvements in profitability (as measured by operating ratios) and productivity (as measured by revenue per truck). Carriers were able to capitalize on higher freight rates without sustaining significant increases in driver or fuel costs as a percentage of revenues. They achieved these results despite a generally inflationary driver cost environment… This shows how much carriers were able to exercise market power for price increases in 2018.”

Also of note is that in addition to dedicated fleets and “shipper of choice” designations, shippers are “placing more emphasis on understanding total cost of ownership.”

That’s to say they’re evaluating not only contractual freight costs, but also exposure to spot market rates and accessorial charges. “Large shippers have noted that they have had success in mitigating irregular operations and out-of-plan shipments by raising base rates, thereby minimizing their exposure to spot rates,” state the authors. “This strategy, however, becomes less advantageous as spot rates fall and capacity increases.”

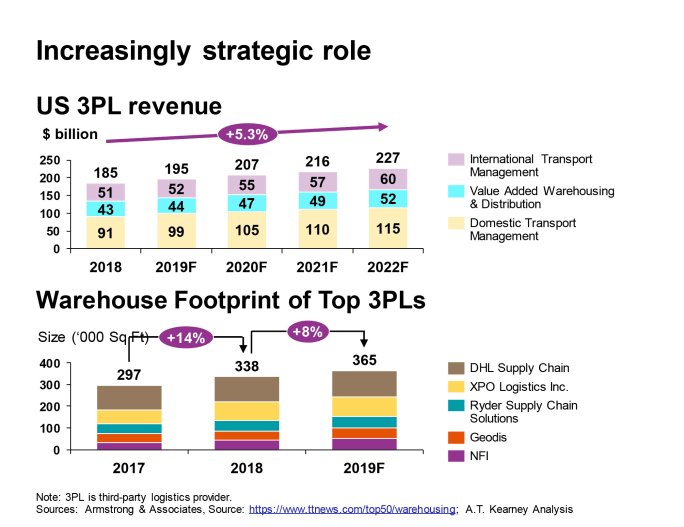

The rise of 3PLs

Among other insights, the report also highlights the rise of third-party logistics providers.

“For all shippers, talent and specialized insight can be hard to find, the right IT infrastructure may not be cost-effective or implementable, and an agile culture is often difficult to adopt,” the authors contend. “Thus, gaps between external requirements and internal capabilities are increasingly being fulfilled by third-party logistics providers.”

The report’s view is that retail shippers want 3PLs “to deliver speed and innovation in nontraditional service lines, and industrial shippers want 3PLs to deliver a seamless and cost-effective supply chain. “In both flavors, 3PLs are expected to rise above operational support activities to a strategic role that’s expected to have a steadily increasing demand, specifically in the domestic transportation and value-added warehousing segments.”

“At the midpoint of 2019,” the report contends, “many experts expect the economy’s momentum to slow, due to the potential for trade tensions to accelerate, global economies to deteriorate, or climate-related risks to materialize.”

On the other hand, such trends as e-commerce growth, lower fuel prices, and technology-driven efficiency gains “could bode well for logistics. Historically, slowing growth and rising capacity have caused shippers to aggressively seek lower rates, causing suppliers to respond by slashing costs and investments— a boom-bust cycle beginning anew.”

According to CSCMP, the authors, sponsors, and interviewees in this latest logistics report “have cause for optimism because at the crest of this hill, neither shippers nor suppliers seem satisfied with business as usual and the opportunity to leverage technology and collaborative practices is driving tangible efficiencies and shared gains.”

Or, in short, when it comes to logistics — at least for this year— too much of a good thing may not be at all a bad thing.

CSCMP offers the report for sale to nonmembers.

More Fleet Management

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →

July Imports Poised to Set Container Record

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

Read More →

HDT Announces 2026 Truck Fleet Innovator Finalists

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Read More →

Van Spot Rates Top Contract Rates for First Time Since 2022

There’s more good economic news for the North American trucking industry according to the latest Truckload Volume Index report from DAT.

Read More →

Carrier Transicold Extends Refrigerated Trailer Life

Fleet Refresh enables refrigerated fleets to replace aging transport refrigeration units instead of entire trailers, while adding Lynx Fleet telematics and BluEdge service coverage.

Read More →