Commentary: What Tonnage, Carloads and PMI Mean for Freight Demand

Understanding the relationship between truck tonnage and railroad carloads, as well as the importance of the Purchasing Managers’ Index in forecasting the direction of truck tonnage.

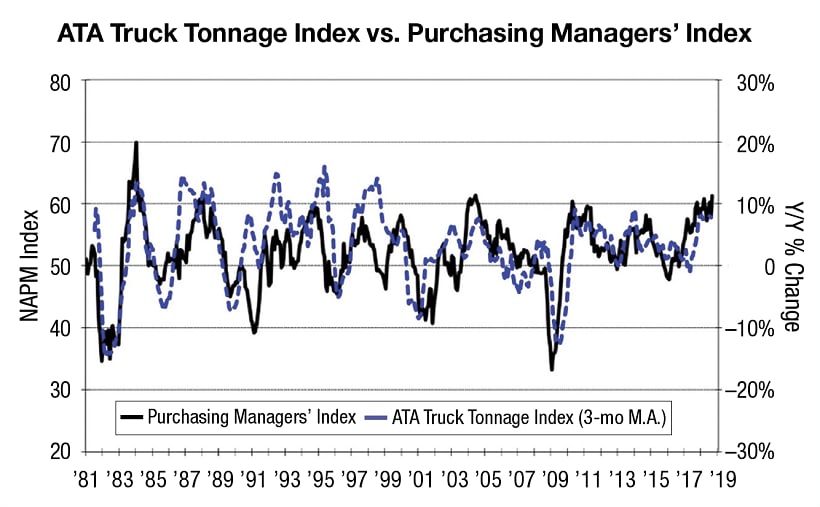

Source: Association of American Railroads and American Trucking Associations

Last month, we introduced the importance of corporate profits as a driver of equipment demand, and the ability of industrial production statistics to help give us a view of where those profits were headed. We also introduced the importance of railroad car loading reports as a real-time read on industrial production trends. This month, given the uncertainty in the stock market about the staying power of this freight market, we’re putting off the “where are we in the cycle update” and will instead talk more about the relationship between truck tonnage and railroad carloads, as well as the importance of the Purchasing Managers’ Index (PMI) in helping forecast the trending direction of truck tonnage.

The American Trucking Associations’ monthly truck tonnage index (non-seasonally adjusted) seems to have reasonably strong predictive value on a two- to three- month lag on where rail carloads may be headed. This makes sense when you consider that truck-related movements tend to represent final sales, while rail carloads tend to be part of the intermediate manufacturing process.

However, what we note in the graph below is that truck tonnage growth tends to be a follower of changes in the Institute for Supply Management’s PMI. What can the ISM’s monthly reports tell us about potential demand for truck services? Plenty! ISM also goes so far as to discuss regional economic strength, industry strength, and also measures interest in new order activity, inventories, and prices – all important factors in determining freight-related demand.

In the ISM’s September report (released Oct. 1), the headline figure was 59.8%. What is important to understand is that this is a sentiment index. It’s a monthly survey sent to more than 400 freight executives, focusing on five areas: new orders, inventory levels, production, supplier deliveries, and employment. The survey asks its respondents if business conditions are getting better, worse, or the same. These responses are graded to an index of 0 to 100, with a reading of 50 representing “no change.” The headline PMI is rarely above 60 or below 40, and we consider the 49 to 51 range to be middling growth. Above 52 we consider growth expectations improving, and below 48, contracting.

So back to 59.8%. This is a strong number historically, and coincides with freight tonnage growth in the mid-to-high single digits (see graph above), but the details of the report paint a broader and more helpful picture of the health of demand for freight services.

Looking behind the numbers, comments from the panel seemed to reflect continued expanding business strength. Demand remains strong, with the New Orders Index at 60 or above for the 17th straight month, and the Customers’ Inventories Index remaining low. The Backlog of Orders Index continued to expand, but at lower levels compared to the previous month. Consumption improved, with production and employment continuing to expand, despite shortages in labor and materials. Continued supply chain inefficiencies are leading to an increased consumption of inventory and a slight expansion of imports. Lead-time extensions, steel and aluminum disruptions, supplier labor issues, and transportation difficulties continue to limit potential activity levels. Respondents noted concerns about tariff-related activity.

Of the 18 manufacturing industries, 15 reported growth in September, with Textile Mills; Miscellaneous Manufacturing; and Plastics & Rubber Products leading the way. The only industry reporting contraction in September was Primary Metals.

Next month: Where we are in the cycle and the third quarter freight earnings update.

Jeff Kauffman has been a recognized transportation authority for almost 30 years, most notably heading freight transportation research for Merrill Lynch. Currently he is managing director for Loop Capital Markets and also heads Tahoe Ventures, a transportation consulting company. He can be reached at jkauffman@truckinginfo.com.

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →