Related: Spot Rates Recede from Record Highs

Is the Capacity Crunch Slowing?

Market numbers point to a turning point in the capacity crisis, says Noel Perry.

August 6, 2018

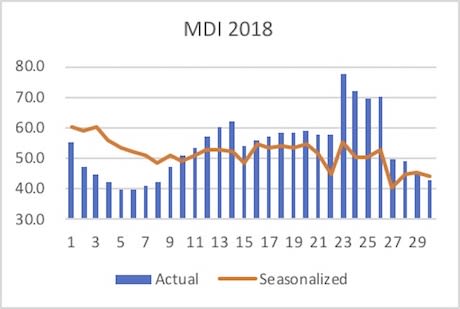

Graph courtesy Transport Futures

3 min to read

Market numbers point to a turning point in the capacity crisis, says Noel Perry.

In two recent entries in his Transport Navigator blog, he tells subscribers that changes in the spot and contract market tracked by Truckstop.com is a leading indicator of changing market conditions.

Perry has been consulting on the freight market since 2008 and has provided insight and forecasts in the past for firms such as FTR and Schneider.

A few weeks ago, on July 10, Perry wrote about the four consecutive weeks of elevated numbers for dry vans in Truckstop.com’s Market Demand Index.

“The change has been coincident with the normal spring safety enforcement period, suggesting a strong enforcement effect. While there is likely some fire to go with that smoke, we need to look more carefully before concluding that the market has moved to a new and more dramatic level of tightness.”

Consulting rate statistics, he explained, did not show the same type of dramatic movement. While “one must conclude that prices are quite high, almost fifty cents per mile above a year ago…They are not, however, moving farther upward in a convincing fashion.” In fact, he said, “one can justifiably suggest that most of the 2018 movement in rates has been seasonal.”

And in fact, he said, if you “seasonalize” the dry van spot rates, the “capacity crisis” actually peaked in January.

Looking at contract rates, which lag behind spot rates, Perry noted that after rising only modestly for much of 2017, contract rates have taken off in 2018 and apparently have not peaked yet. Such double-digit increases have occurred only one other time since 2000: in 2004, the other great capacity event.

By last week, on August 3, Perry said looking at the seasonalized Market Demand Index, he could see three distinct periods for the year. The first featured falling readings as the market settled down, after peaking at the time of the beginning of the electronic logging device (ELD) mandate. The market established a new, roughly flat trend through the middle spring as participants were testing the effects of ELD enforcement.

However, since Week 20, roughly Memorial Day, there has been a new and declining trend. (The bump-ups in weeks 23 and 26 have to do with the timing of holidays, not sustained market dynamics.) Since the current trend started 10 weeks ago, the Index has lost almost 20% of its value, he said.

“I conclude that we have reached a turning point in the current capacity crisis," he wrote. "Ten weeks and the 20% drop are more than enough to substantiate that conclusion. This development is entirely consistent with the cessation of new regulation. Only the very strong economics in the second quarter have kept the decline from being more dramatic.”

Of course, spot market data is a leading indicator.

“History tells us that spot prices lag capacity measures by three to six months. We should also conclude that same downward pressure will eventually impinge on contract pricing, perhaps with a further lag of six months,” he wrote. “Things will happen in contract pricing, caused by the same market forces, but not until later.”

The upshot? Perry predicts that “pricing will remain strong even though the capacity fundamentals are softening. This means that short-term operating plans, still dealing with robust pricing, will be at odds with planning, which must account for weaker pricing (and volumes).”

Perry's Transport Navigator blog is written under the banner of his Transport Futures consultancy firm and is available by subscription only.

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →