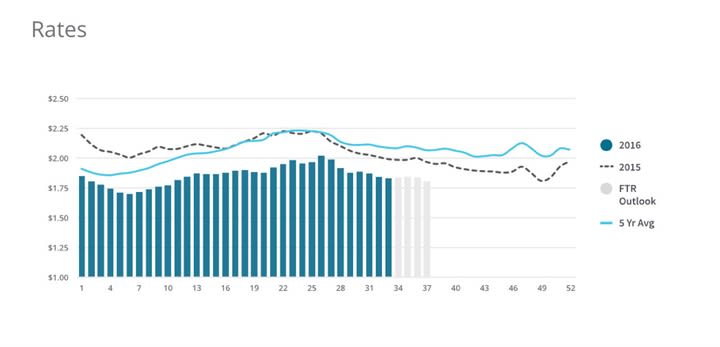

As FTR and Truckstop.com apply "big data" analysis to spot market pricing, Noel Perry, FTR transportation economist, offers some insights into the volatility of spot pricing and how spot prices correlate with contract pricing.

As FTR and Truckstop.com apply "big data" analysis to spot market pricing, Noel Perry, FTR transportation economist, offers some insights into the volatility of spot pricing and how spot prices correlate with contract pricing.

Graph courtesy FTR and Truckstop.com

As FTR and Truckstop.com apply "big data" analysis to spot market pricing, Noel Perry, FTR transportation economist, offers some insights into the volatility of spot pricing and how spot prices correlate with contract pricing.

The data being analyzed starts in the first quarter of 2008, just before the big downturn. Since the bottom of that recession, contract prices have averaged a 1% quarter over quarter growth (annualized). Even with the big decline last year, spot prices have averaged 2%. This is consistent with the big move of random freight from the edges of contracts into the spot market, Perry notes. Volume has built, and so have rates.

"I expect this trend to peak in 2019 with the coming crisis in regulatory drag," Perry says. "After that is unclear."

This is no surprise, Perry says. The spot market is defined as the home of swings in random demand. The capacity pressure indices calculated by Truckstop.com and DAT both swing widely in almost lockstep. It follows that price changes swing widely.

The standard deviation of spot rate changes since the bottom of the last recession is five times larger than that of contract rates. "In case you have forgotten your college stat definitions, that means spot rate growth varies five times more than contract rate growth," he says.

With spot prices, the lags between market events and price response are short, perhaps up to a quarter, Perry says. The response is not instantaneous because truckers and shippers take time to realize that a change is required. There are also some small delays in the statistics. As big data (and forecasting tools) emerge, this lag should be shortened because market decision makers will know that something is happening sooner, he notes.

Contract rates have a much more noticeable lag. They tend to peak two quarters after spot rates move. In part, this is due to the nature of data collection and the schedule for contract renewals. In part, it is the lag in capacity migration between the two segments.

Both customers and carriers work to keep market conditions stable in this segment," Perry explains. Changes, increasingly come from outside forces overwhelming those efforts. Driver supply is one good example of such outside forces. If spot rates rise at some point, drivers serving that market (and carriers) will earn enough to justify leaving dependable contract situations. But rates have to climb and stay high for a while before drivers will take that risk.

"We know from history that strong changes in rate levels tend to last longer than one would expect," Perry said. "Both carriers and shippers get used to market conditions and tend to sustain them for a while after market conditions change. This is human nature.”

He pointed out two recent instances of this. First, the six-month capacity crisis of early 2004 funded a two-year burst in rates. More recently, the 2014 spot rate acceleration lasted until mid-2015 despite the fact that its first accelerant, bad winter weather, subsided by June of 2014, and the second accelerant, hours of service changes, were suspended in December 2014.

The trucking industry has no shortage of cybersecurity reports and cargo crime statistics. What it lacks is timely, operational intelligence that fleets can actually use.

Read More →

ATRI’s latest research points to litigation, social inflation, and soaring claims costs as key drivers behind record-high liability premiums for trucking fleets. But there are things motor carriers can do.

Read More →

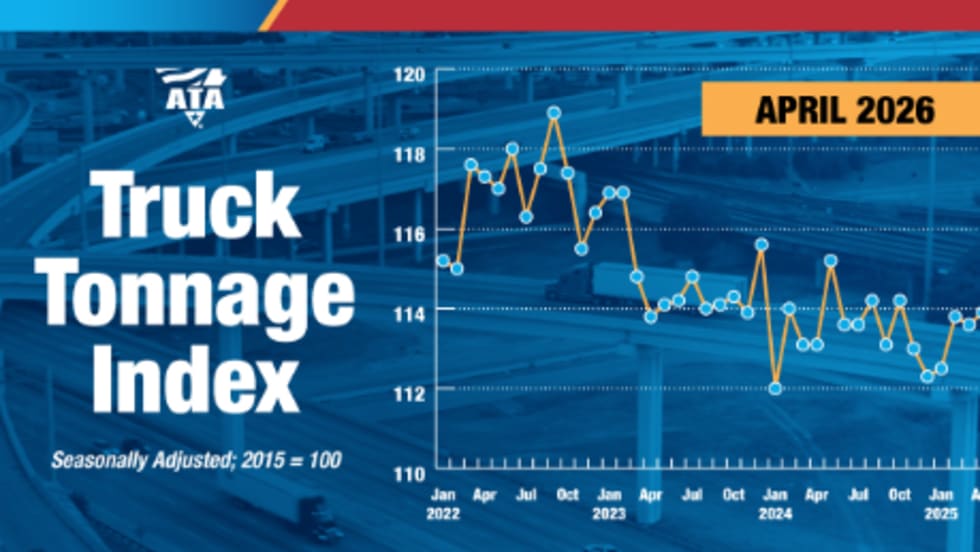

ATA’s For-Hire Truck Tonnage Index was unchanged in April after a strong March gain, with freight volumes remaining at their highest levels since late 2022.

Read More →

Fleetworthy has unveiled three major product launches it says mark a new era in fleet readiness.

Read More →

Transportation attorney Greg Feary breaks down the recent Supreme Court decision that brokers can be held liable for damages in truck accidents and what it means for the trucking industry going forward.

Read More →

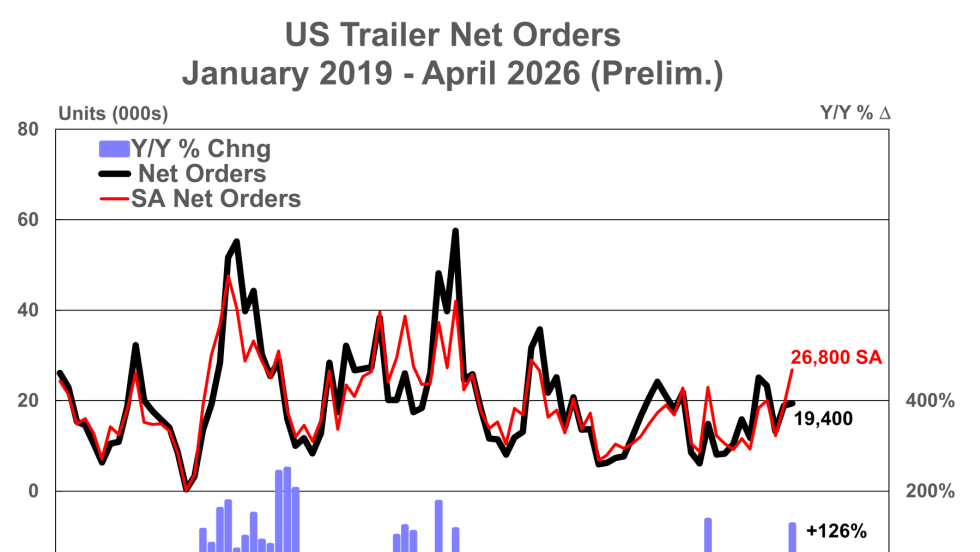

Preliminary net trailer orders rose 3% from March and jumped 126% year over year, signaling stronger-than-expected demand despite typical seasonal softness.

Read More →

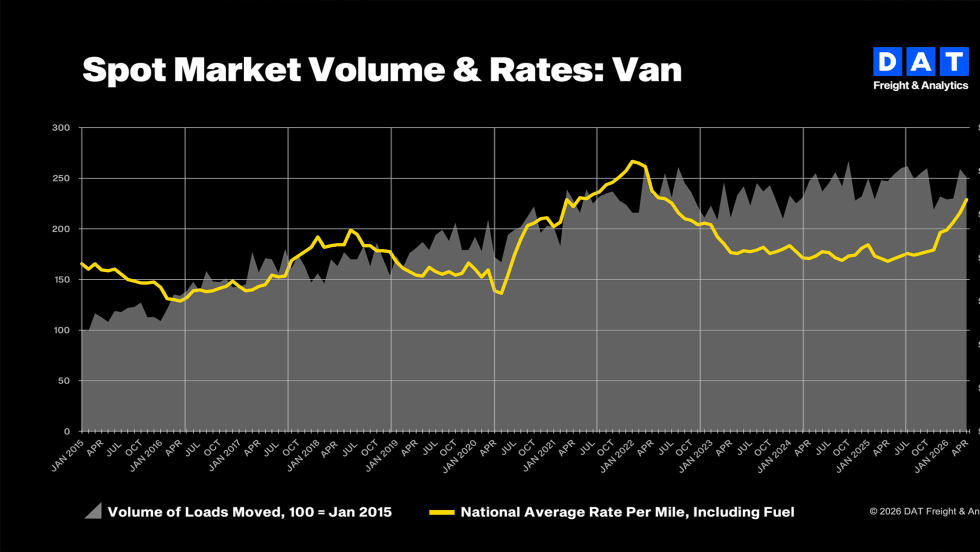

Truckload spot and contract rates climbed in April. But DAT says higher fuel costs -- not stronger freight demand -- were behind most of the increase.

Read More →

Heavy Duty Trucking has extended the deadline for nominations for its Truck Fleet Innovators awards. The deadline has been extended to May 22.

Read More →

The unanimous SCOTUS ruling in the closely watched Montgomery v. Caribe case allows state negligence claims against freight brokers that hire unsafe motor carriers, raising new liability and vetting concerns among brokers.

Read More →

FMCSA's long-awaited registration system promises a single portal — and tighter fraud controls. And there are steps you need to take by May 14.

Read More →