Many fleets recruiting owner-operators are having a hard time finding enough qualified applicants -- so are turning to grow-your-own tactics with lease-purchase programs. (Read more about such programs in the July issue of HDT.)

Which Drivers Make Good Lease-Purchase Candidates?

While capacity is important, the DOT's new CSA enforcement regime and ever-nosier agencies like the IRS make it clear that you simply can't take people that need to be led by the hand into a lease-purchase program.

July 9, 2013

3 min to read

But who qualifies as a good prospective lease-purchase candidate? If you said anyone who can fog up a mirror, you're out of touch. While capacity is important, the DOT's new CSA enforcement regime and ever-nosier agencies like the IRS make it clear that you simply can't take people that need to be led by the hand into a lease-purchase program. The oversight required to keep them on track would bear a dangerous resemblance to an employer-employee relationship.

Scheider National, for example, maintains that separation through a company called Schneider Finance Inc. It's operated at arm's length from the carrier. Grailing Jones, the small business owner-operator development manager at SFI, calls the program the Schneider Career Path Option.

"We don't recruit and we don't draft people into the program," he says. "We offer it as an option – like the name says – to people with ambitions of starting a small business with a future."

Most of the clients are referrals, Jones says, but the program accepts clients from several streams. Former military drivers, CDL school graduates, current Schneider National company drivers and literally walk-ins. Depending on the individual, Jones is looking for six months to a year's experience as a company driver, or previous owner-operator experience.

"It's not something we offer to everyone," he says. "The individual has to have the desire and then explain to us why they want to be an owner before we'll consider them. We're not being elitist; it's our money. If we're going to take a risk, we're going to do it on our terms."

Jones says it's important that the client fits the company and vice versa. They usually insist on a minimum six-month period for each party to get comfortable with each other – a familiarization period and on-the-job training rolled into one.

"That gives us time to look at them and them to look at us," he says. "We're not in this to make money from leasing trucks; we're in this to provide capacity. The last thing we want to do is waste our company assets on an individual who is not sure."

Both Grailing and David Strand, president of Wholesale Truck & Finance, say one of the traditional barriers to truck ownership, credit scores, isn't critically important, but it is considered.

"We look at what the whole person is about," Strand says. "I can think of a dozen reasons why good people get stuck with bad credit. As long they are not in open bankruptcy, and they don't owe back child support, we'll look at them."

What Strand wants to see is some personal commitment – a $4,000 down payment. When they have some skin in the game, they tend to take ownership more seriously, he says.

"We often have carriers asking if they can make the down payment for the driver, but my very simple answer is it doesn't work. We will take $2,000 from the sign-on bonus, but the driver has to have at least $2,000 of his or her own money in the deal."

Strand also looks at employment history. He won't look at anyone with more than two jobs in the past three years. "We want to see some evidence that they've tried to work with carriers rather than just bailing at the first sign of trouble or anytime the grass starts looking greener somewhere else."

Subscribe to Our Newsletter

More Fleet Management

From Diesel Prices to Cyberattacks: How the Iran War Is Affecting Trucking

The impact of the Iran conflict extends beyond fuel costs, bringing more fraud and cybersecurity risks to the trucking industry.

Read More →

ATA’s Spear Warns Fuel Prices, Trade Policy, and Global Conflict Could Stall Trucking Recovery

Speaking at the TMC Annual Meeting in Nashville, ATA President Chris Spear said trucking faces mounting pressure from rising fuel prices, geopolitical instability, and uncertainty around trade policy.

Read More →

New Entrants, Chameleon Carriers, and Safety: Is It Too Easy to Start a Trucking Company?

More than 100,000 new trucking companies enter the industry each year, but regulators manage to audit only a fraction of them. That churn creates opportunities for inexperienced startups — and for “chameleon carriers” that shut down after safety violations and reappear under new identities. Read more from Deborah Lockridge in this commentary.

Read More →

Fleet Managers Invited to Apply for Exclusive HDT Exchange Event

HDTX is an intimate event that connects heavy-duty trucking fleet managers with industry suppliers through small-group discussions, educational sessions, and structured one-on-one meetings.

Read More →

DAT Launches iPhone Widget to Help Owner-Operators Find Loads Faster

New DAT One feature shows top-paying loads directly on an iPhone’s home screen, helping carriers react faster to spot-market opportunities.

Read More →

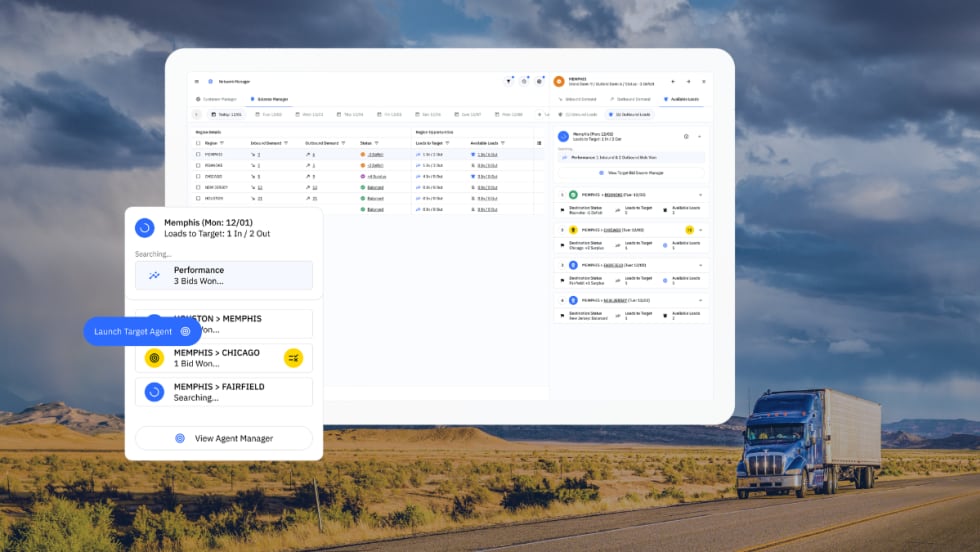

Optimal Dynamics Launches AI System to Help Carriers Choose Better Freight

Optimal Dynamics says its new Scale platform uses AI agents and optimization to help carriers find and secure freight that improves network balance and profitability.

Read More →

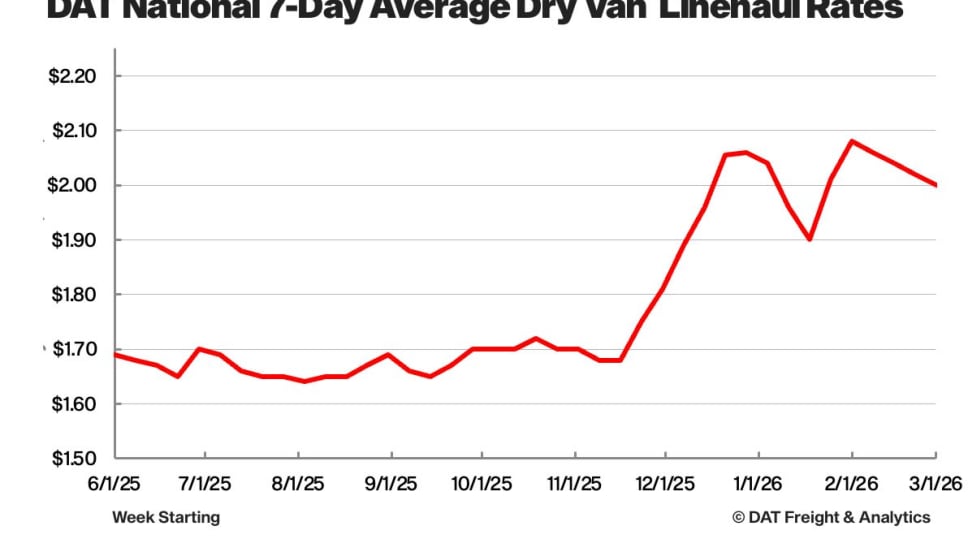

DAT: Flatbed Demand Climbs as Van and Reefer Rates Soften

DAT Freight & Analytics data shows tightening flatbed capacity, easing produce markets, and softening van and reefer rates.

Read More →

Run on Less “Messy Middle” Data Shows Multiple Paths Forward for Truck Powertrains [Watch]

NACFE's Run on Less - Messy Middle project demonstrates the power of data in helping to guide the future of alternative fuels and powertrains for heavy-duty trucks.

Read More →

Federal Court Lets NYC Congestion Pricing Continue

A federal court ruling allows New York City’s congestion pricing program to continue, leaving truck tolls in place for fleets delivering into Manhattan.

Read More →

Fontaine Modification Launches Real-Time Truck Modification Tracking Portal

Fontaine Modification has introduced a new customer portal designed to give fleets real-time visibility into the truck modification process, addressing one of the most common questions fleet managers face: “Where’s my truck?”

Read More →