The U.S. manufacturing industry kicked off the year with its strongest performance in two years, according to a new report, while a separate one about the sector plus others regarding employment, personal spending and incomes all points to increased economic growth.

Economic Watch: Manufacturing, Employment Help Launch Strong 2017

The U.S. manufacturing industry kicked off the year with its strongest performance in two years, according to a new report, while a separate one about the sector plus others regarding employment, personal spending and incomes all points to increased economic growth.

Evan Lockridge・Former Business Contributing Editor

5 min to read

The final U.S. Manufacturing Purchasing Managers’ Index for January, released Wednesday by financial information services provider IHS Markit, showed both output and new order growth accelerating since the end of last year.

Improving business conditions were also reflected in a sustained upturn in payroll numbers and the steepest rise in stocks of finished goods since the index began in 2007. Meanwhile, manufacturers reported that confidence regarding the year-ahead business outlook was the strongest since March 2016, which was mainly linked to hopes of a continued upturn in domestic economic conditions.

All this pushed the index to a reading of 55 in January, up from 54.3 in December and little changed from the preliminary January reading of 55.1. A reading above 50 indicates expansion while one below 50 signals contraction.

January data revealed a renewed acceleration in output growth among manufacturing firms, with the rate of expansion reaching its strongest for 22 months.

According to Chris Williamson, chief business economist at IHS Markit, despite exports being subdued by the strong dollar, order books are growing at the fastest pace for over two years on the back of improved domestic demand.

“With optimism about the year ahead at the highest since last March, the outlook has also brightened,” he said. “Production is consequently growing at the strongest rate for almost two years and inventories are rising at a rate not seen for nearly a decade as firms respond to higher demand, suggesting the goods-producing sector will make a decent contribution to first quarter GDP.”

Williamson cautioned that with input costs also rising at the steepest rate for over two years, and hiring sustained at an encouragingly solid pace as firms expand capacity, all of the survey indicators point to the Federal Reserve hiking interest rates again soon, most likely in the late spring or early summer.

Meantime, a separate report on manufacturing for January from the Institute for Supply Management showed economic activity in the sector expanded once again with its Purchasing Managers’ Index (PMI) registering 56%, an increase of 1.5 percentage points from the seasonally adjusted December reading of 54.5%. Like the Markit index, a reading above 50% indicates expansion.

Also, its New Orders Index, part of the larger reading, increased for the fifth straight month while the Production Index also increased for the fifth consecutive month. Both these and the overall index hit their highest levels since November 2014.

Of the 18 manufacturing industries surveyed, 12 reported growth in January.

"The past relationship between the PMI and the overall economy indicates that the PMI for January corresponds to a 4% increase in real gross domestic product on an annualized basis,” said Bradley J. Holcomb, chair of the ISM Manufacturing Business Survey Committee.

Such a figure for the GDP is slightly more than double the annual rate reported in the fourth quarter last year by the Commerce Department last week.

Overall Employment Pushes Higher Again

Also released Wednesday was a report on private sector, nonfarm employment showing it increased by 246,000 jobs from December to January, according to payroll processor ADP.

Its National Employment Report showed the biggest monthly increase since last June and came before federal numbers about employment and unemployment for January are set to be released Friday.

“2017 got off to a strong start in the job market,” said Mark Zandi, chief economist of Moody’s Analytics. “Job growth is solid across most industries and company sizes. Even the energy sector is adding to payrolls again.”

There was a 46,000 jobs gain in the goods producing sector, including 15,000 in manufacturing, while the rest in January were in the service sector.

“The U.S. labor market is hitting on all cylinders and we saw small and midsized businesses perform exceptionally well,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “Further analysis shows that services gains have rebounded from their tepid December pace (151,000 job additions), adding 201,000 jobs. The goods producers added 46,000 jobs, which is the strongest job growth that sector has seen in the last two years.”

Job Growth Leading to Higher Spending and Incomes

This follows a report from earlier in the week from the Commerce Department that showed personal spending in December increased 0.5% from the month before while personal income increased 0.3%.

These figures were included in the first estimate of the fourth quarter U.S. gross domestic product (GDP) released last week showing the economy grew 1.9% in October through December. That was down from the 3.5% pace in the third quarter of 2016, and less than a 2.2% increase expected by a poll of analysts.

While the overall GDP figure was disappointing, the result was due largely to a wider trade deficit, which are a subtraction to the GDP, and not to weakness here at home.

“The strong finish [in personal spending] to the end of the quarter bodes well for another strong gain in the first quarter of 2017, according to Nathan Janzen, senior economist at RBC Economics.

“We expect household spending will remain a support to economic activity going forward reflecting strong labor markets, rising consumer confidence, and low interest rates,” he said. “We expect overall GDP to increase at an above-trend 2.3% rate in first quarter of 2017 to build on a 1.9% Q4 gain and 3.5% jump in third quarter.”

More Fleet Management

Trucker Path, Truckstop.com Expand Load Access Partnership

An expanded Trucker Path and Truckstop.com integration brings more freight opportunities into the TruckLoads app while emphasizing security and network quality.

Read More →

Truckload Rates Hit Two-Year Highs as Diesel Costs Surge, DAT Says

Strong March freight demand combined with a spike in fuel costs pushed both spot and contract truckload rates to their highest levels in more than two years.

Read More →

The AI Conversation You Need to Have with Your TMS Provider

Everyone’s talking about AI — but is your transportation management system actually built for it?

Read More →

Kriska Buys Fellow Canadian Carrier Sharp Transportation Systems

Being part of KTG will allow Sharp to expand and improve its services.

Read More →

Bill in House Would Raise Minimum Insurance for Motor Carriers to $5 Million

The Fair Compensation for Truck Crash Victims Act would increase insurance requirements for interstate motor carriers by nearly seven times.

Read More →

FTR Trucking Conditions Index Hits Four-Year High in February

Strong freight rates push TCI to 10.2, but FTR expects fuel-price volatility to skew March results.

Read More →

C.H. Robinson Offers Carriers Relief as Diesel Prices Surge

C.H. Robinson is waiving fees on fuel cards and cash advances for April and May, aiming to help carriers offset rising diesel costs tied to geopolitical instability.

Read More →

What Trucking Events are Happening in 2026?

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

Volvo’s Quiet Confidence Turns into a Full-Throated Bet on the Future

After years of steady, methodical progress, Peter Voorhoeve says the OEM’s latest lineup isn’t just evolutionary. It’s delivering real, measurable gains for fleets right now.

Read More →

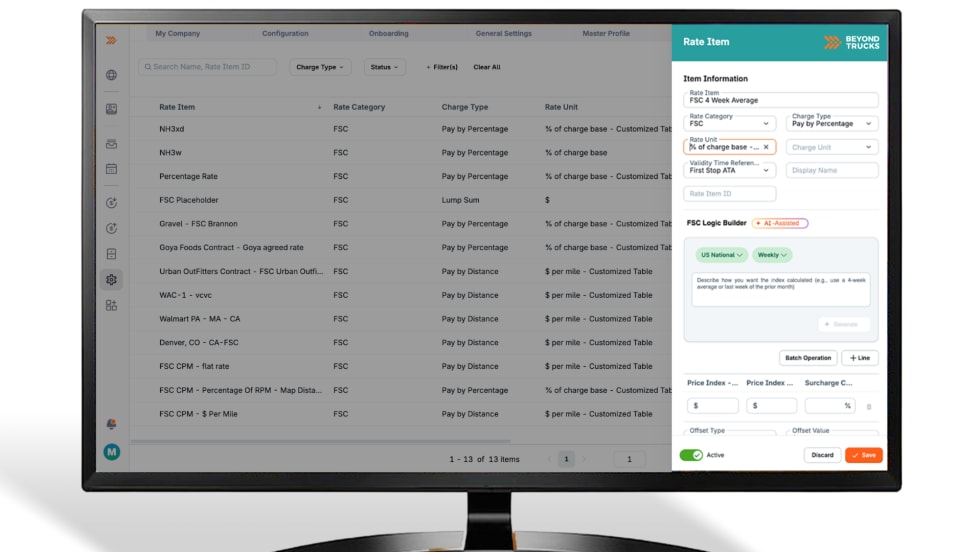

BeyondTrucks Targets Rate Complexity with New AI RateAgents

BeyondTrucks says its new RateAgents can turn plain-language rate logic into working code, starting with fuel surcharges — a critical but notoriously complex piece of carrier revenue.

Read More →