Economic Watch: Manufacturing Pushes Industrial Production Higher Amid Other Reports

The output from the nation's factories, mines and utilities increased in July, the largest gain since November 2014, and there also are improvements in housing and e-commerce. But there is disagreement over what the latest inflation numbers mean for interest rates.

The output from the nation's factories, mines and utilities increased in July, the largest gain since November 2014, and there also are improvements in housing and e-commerce. But there is disagreement over what the latest inflation numbers mean for interest rates.

The U.S. Federal Reserve’s measure of industrial production rose 0.7% in July, better than many analysts expected, after moving up a downwardly revised 0.4% in June from a first reported 0.6% gain.

Manufacturing output rose 0.5% in July for its largest gain since July 2015. The index for utilities rose 2.1% as a result of warmer-than-usual weather in July that boosted demand for air conditioning. Mining moved up 0.7%, another modest increase over the past three months after falling about 17% between December 2014 and April 2016.

Despite the overall gain, total industrial production in July was 0.5% below the same time a year ago, but it's at 104.9% of its 2012 average.

Capacity utilization for the industrial sector increased half a percentage point in July to 75.9%, a rate that is 4.1 percentage points below its 1972–2015 average.

Homebuilding improves

A Commerce Department report shows U.S. housing starts in July rose 2.1% from June’s revised level to an adjusted annual rate of more than 1.2 million, its highest level since February and better than a consensus estimate from economists. Compared to July 2015, the rate is 5.6% better.

“Today’s reported increase leaves July housing starts tracking strongly above their second quarter average, indicating the earlier decline in residential investment [the first in more than two years] is likely to prove temporary,” says Josh Nye, economist at RBC Economics Research. “We look for residential investment to return to making a positive contribution to gross domestic product growth in the third quarter, albeit at more moderate pace relative to the double-digit growth recorded last year.”

The number of homebuilding permits issued in July, an indicator of future homebuilding activity, edged down just 0.1% but remains 0.9% higher than a year earlier.

The report on housing follows one from Monday showing builder confidence in the market for newly constructed single-family homes in August rose two points to 60 from a downwardly revised reading of 58 in July, according to the National Association of Home Builders/Wells Fargo Housing Market Index.

“New construction and new home sales are on the rise in most areas of the country, and this is helping to boost builder sentiment,” said NAHB Chairman Ed Brady.

Two of the three HMI components posted gains in August. The component gauging current sales conditions rose two points to 65, while the index charting sales expectations in the next six months increased one point to 67. The component measuring buyer traffic fell one point to 44.

“Builder confidence remains solid in the aftermath of weak GDP reports that were offset by positive job growth in July,” said NAHB Chief Economist Robert Dietz. “Historically low mortgage rates, increased household formations and a firming labor market will help keep housing on an upward path during the rest of the year.”

E-Commerce Bright Spot in Retail Sales

The Commerce Department released quarterly numbers for e-commerce retail sales showing an increase in the second quarter of 4.5% from the first quarter of the year. This happened as total U.S. retail sales increased at a much slower rate of 1.5%.

When second quarter 2016 figures are compared to a year earlier, the gain by e-commerce was even wider, increasing 15.8% year-over-year while total retail sales improved 2.3%.

The increase comes as little surprise, with Economist Donald Broughton noting in the July Cass Freight Index report that the U.S. is shifting from so-called ‘brick and mortar’ retailing to e‐commerce/omni‐channel distribution of consumer goods.

The report on e-commerce follows disappointing numbers released separately by the Commerce Department on Friday showing U.S. retail sales in July were flat compared to the month before but up 2.3% from a year earlier.

Consumer Prices Stable

Also remaining unchanged in July are prices at the consumer level. The Labor Department reports the Consumer Price Index was flat from June, matching analysts' expectations, following increases of 0.2% each the previous two months.

Over the past 12 months the CPI, the widest measure of inflation, has increased just 0.8% compared to a 1% year ago rate in June.

So-called core prices, which strip out volatile food and energy prices, increased 0.1% in July, with the year-over-year level showing a 2.2% increase after posting a June rise of 2.3%.

Weak inflation at the consumer prices level is one of the main reasons the Federal Reserve has put off increasing interest rates further. However, RBC Economics is forecasting energy prices, which have pushed inflation lower, are set to switch from being a weight on the annual inflation rate to pushing it higher.

"The easing of this base effect should stop driving a wedge between the headline and core rates, and we see both above 2.% in the months ahead," said Dawn Desjardins, deputy chief economist at RBC. "For the Fed, increases in the headline rate will remove one obstacle to a rate hike, given that the labor market is within reach of full employment."

According to Desjardins, the other key factor staying the Fed’s hand is nervousness about international developments. On that front, markets appear to be unconcerned, and while the data point to the United Kingdom sinking fast, most other nations are bearing up.

“[Fed] Chair [Janet] Yellen’s upcoming speech on Aug. 26 at Jackson Hole will provide the Fed with the opportunity to update its outlook,” Desjardins said. “Comments acknowledging an easing in concerns about both the global backdrop and the current low level of inflation may shift market expectations about the timing of the Fed’s next hike.”

However, not all agree with such an assessment. Stifel Fixed Income Chief Economist Lindsey Piegza says inflationary pressures appear subdued as we head further into the third quarter, following little change in the consumer price report and a sizable decline wholesale prices.

“Thanks in part to a retreat in energy prices coupled with cost declines across several other key categories, inflation continues to trend well below the Fed’s longer-term objective,” she said. “At this point, while some analysts continue to make the case of a strong labor market, inflation, or lack thereof, offers no reason for the Fed to continue with an additional removal of accommodation.”

Piegza belives with subdued growth across the first six months of the year, tepid business investment, and lackluster inflation, the Fed is likely to remain sidelined for much longer than expected, keeping interest rates much lower than previously expected.

More Fleet Management

Enhance Fleet Performance with High-Efficiency Auxiliary Power Units

Drive sustainable cost savings while increasing driver comfort during short- and long-haul logistics operations.

Read More →

Is Your Parts Procurement Process Reactive or Proactive?

Ready to revamp your parts procurement process? Learn how now with “Strategic Parts Purchasing: A Process Checklist”

Read More →

What Trucking Events are Happening in 2026?

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

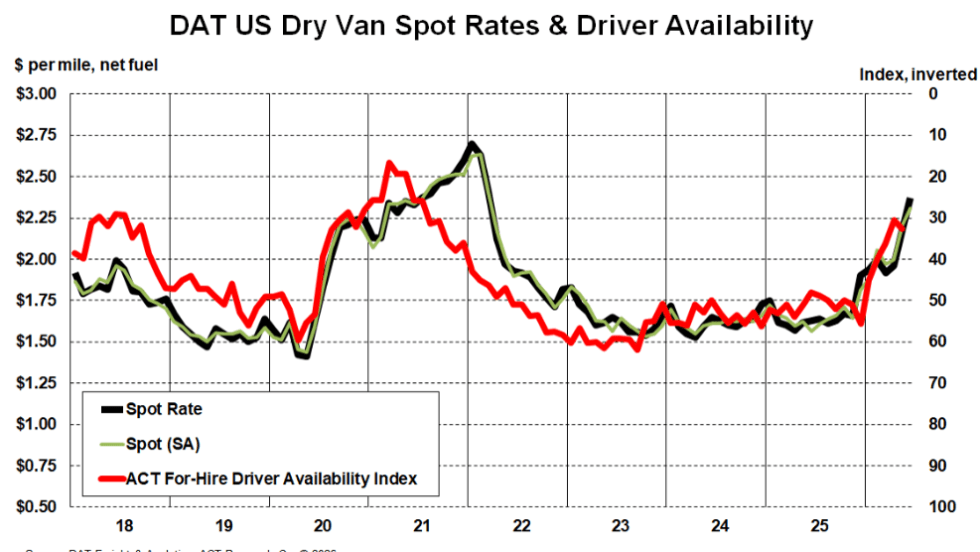

Truckload Rates Keep Rising as Tight Capacity Fuels Freight Market Recovery

Spot and contract rates continued climbing in May and June, not because freight demand is surging, but because fewer trucks and drivers are available.

Read More →

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

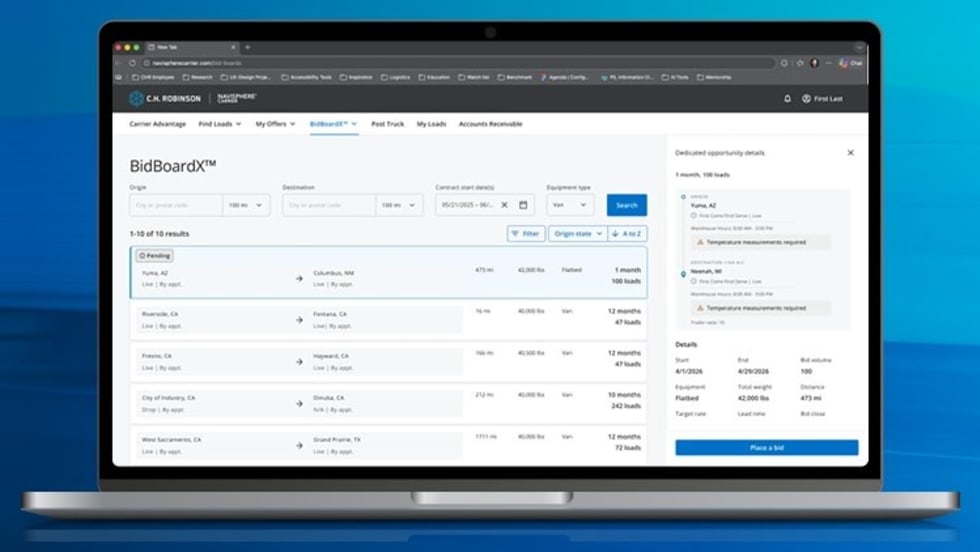

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →