Earnings Watch: Hub, C.H. Robinson, Wabash National, Rush Enterprises

The second quarter earnings season continued on Tuesday with companies ranging from a fleet and 3PL to a trailer maker and mega-dealer, with all but one reporting higher earnings than the same time last year.

The second quarter earnings season continued on Tuesday with companies ranging from a fleet and 3PL to a trailer maker and mega-dealer, with all but one reporting higher earnings than the same time last year.

Hub Group Profit Increases 12%

The multi-modal freight transportation provider Hub Group Inc. (NASDAQ: HUBG) reported net income increased to $20.7 million, or 61 cents per share, compared to $18.5 million, or 51 cents per share, in the second quarter of 2015. The per share performance beat a consensus estimate by 4 cents.

The hike in profit came despite revenue falling 5% to $856 million, which the Illinois-based company attributed primarily to lower fuel surcharge revenue. Operating income improved to $34.3 million from $29.5 million a year earlier.

Hub’s trucking segment revenue fell 6% to $649 million, which it mainly attributed to a drop in fuel surcharge revenue. Second quarter intermodal revenue dropped 6% to $438 million as volume fell 2%. Truck brokerage revenue fell 11% to $83 million, while Unyson Logistics revenue dropped 1% to $127 million.

The segment's operating income was $27.2 million, an increase of 24% compared to the prior year period.

Hub’s third party logistics operation, known as its Mode segment, saw revenue decrease 1% to $232 million. Operating income was $7.1 million compared to $7.5 million in the prior year period.

C.H. Robinson Records Higher Profit Despite Lower Revenue

Third-party logistics provider C.H. Robinson Worldwide Inc. (NASDAQ: CHRW) reported its profit increased 4.3% despite a 6.9% drop in total revenue.

The Minnesota-based company reported net income of $143.1 million, or $1 per share that met a consensus expectation, versus 94 cents a year earlier, as revenue was nearly $3 billion. This also led to operating income improving to $233.7 million from $229.1 million a year earlier.

The company reported truckload net revenues dropped 1.4% in the second quarter of 2016 compared to the second quarter of 2015, while total truckload volumes increased approximately 3% percent. North American truckload volumes also increased approximately 3% over the same period.

“In North America, excluding the estimated impacts of the change in fuel prices, our average truckload rate per mile charged to our customers decreased approximately 7.5% in the second quarter of 2016 compared to the second quarter of 2015,” C.H Robinson said in a statement. “In North America, our truckload transportation costs decreased approximately 8%, excluding the estimated impacts of the change in fuel prices.”

Less-than-truckload net revenue increased 9% in the second quarter while LTL volumes increased approximately 7%.

In contrast, intermodal net revenues fell 21.8% in the second quarter, primarily due to decreased volumes and net revenue margin declines, according to the company, which said “intermodal opportunities were negatively impacted by the alternative lower cost truck market.”

C.H. Robinson also reported increases of 1.7% and 2.7%, respectively, for its ocean and air transport net revenues along with a 5.8% hike in customs net revenue.

Other logistics services net revenues, which includes managed services, warehousing, and small parcel, increased 24% in the second quarter, primarily from growth in managed services, according to the company.

Wabash National Profit Improves, Increases Forecast

For trailer maker Wabash National Corp (NYSE: WNC), profit improved in the second quarter despite lower trailer sales.

The Indiana-based company (which also makes other products), reported net income for the second quarter was $35.5 million, or 53 cents per share, which beat a consensus forecast. This compares to second quarter 2015 net income of $28.6 million, or 41 cents per share.

Revenue for the second quarter fell 8% to $471 million, while operating income increased 40% to $58.9 million.

During the second quarter, Wabash shipped 15.350 trailers compared to 16,100 a year earlier. Although this figure was close to previous guidance of 15,500 to 16,500 trailers, commercial trailer products segment net sales fell 7% to $382.2 million. However, despite the lower revenue, gross profit and gross profit margin increased $20 million.

The company’s diversified products segment reported net sales decreased 12% to $92.9 million, primarily the result of lower tank trailer shipments and lower sales of non-trailer truck mounted equipment. It was partially offset by increased demand for process systems and composite products. Gross profit and operating income were comparable to the prior year period, while gross profit margin and operating margins improved.

“A healthy backlog of $860 million, overall trailer market projections well above replacement levels for the remainder of 2016 and outstanding operational execution across the business, have put us on pace to deliver another record year in 2016, our fifth consecutive year of record performance,” said Dick Giromini, president and CEO. “As such, we are increasing our full-year adjusted earnings guidance to $1.80 to $1.90 per diluted share, representing a year-over-year improvement of 24% at the midpoint of this range.”

Rush Profit Sinks By Nearly Half

In contrast, the mega-size truck dealer Rush Enterprises (NASDAQ:RUSHA, RUSHB), saw a big drop in its second quarter profit, falling nearly 45%.

The Texas-based operation reported a profit of $10.8 million, or 27 cents per share, down from 48 cents per share a year ago, but 1 cent better than a consensus estimate. Revenue also declined, but at a lesser 22.8% margin, falling to $1.026 billion.

"As expected, continued softness in the energy sector, a choppy freight environment, excess Class 8 fleet vehicle capacity, and declining used truck values plagued the industry and negatively impacted our Class 8 new and used truck sales and parts and service revenues in the second quarter," said W.M. "Rusty" Rush, chairman, president and CEO.

He said to help offset current market conditions, the company has implemented significant and broad-reaching expense reductions, including the consolidation of truck center locations in eight states that were operating in close proximity to other dealerships. However, the company does not expect to realize the full results of this effort until later this year.

Rush's Class 8 truck sales dropped 45% compared to the second quarter of 2015 and accounted for 4.9% of the U.S. Class 8 truck market.

"Our Class 8 new truck sales in the second quarter were severely impacted by reduced demand from several of our large fleet customers and from the sluggish Class 8 truck market," Rush said. “Due to the current economic climate, an uncertain freight environment, reduced order intake, excess capacity and depressed used truck values, we expect new Class 8 truck sales will remain at current levels through the end of 2016.”

The company’s Class 4-7 medium-duty truck sales dropped 4% compared to the second quarter of 2015, accounting for 4.9% of the total U.S. market.

"Our medium-duty truck sales remained solid during the second quarter, though down slightly due to the timing of deliveries to several large fleets earlier this year," Rush said. “We expect our medium-duty truck sales will remain flat with our second quarter performance through year end.”

Parts, service and body shop revenues for Rush were $328.7 million in the second quarter of 2016, compared to $353.3 million in the second quarter of 2015.

The company delivered 2,592 new heavy-duty trucks, 2,792 new medium-duty commercial vehicles, 386 new light-duty commercial vehicles and 1,750 used commercial vehicles during the second quarter of 2016. This compares to 4,702 new heavy-duty trucks, 2,902 new medium-duty commercial vehicles, 457 new light-duty commercial vehicles and 2,009 used commercial vehicles during the second quarter of 2015.

More Fleet Management

HDT Announces 2026 Truck Fleet Innovator Finalists

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Read More →

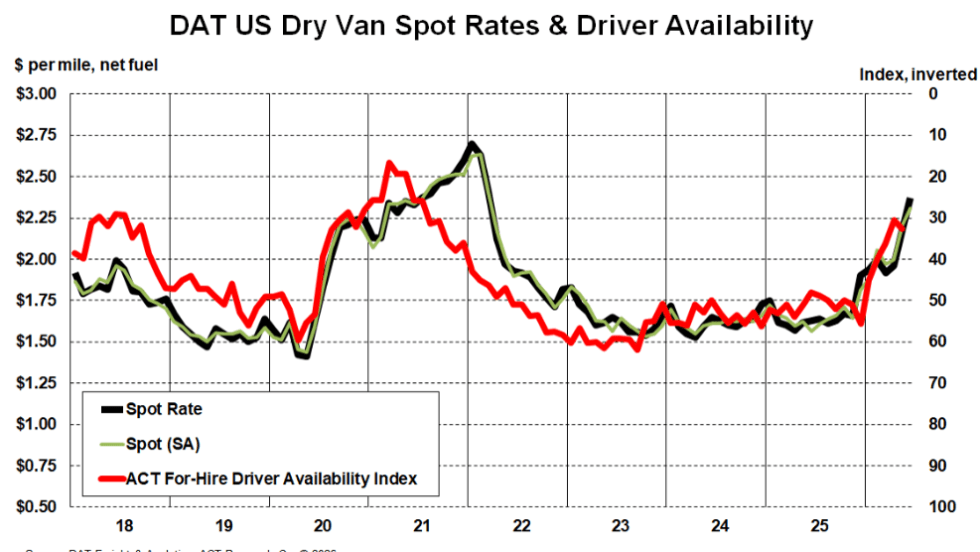

Van Spot Rates Top Contract Rates for First Time Since 2022

There’s more good economic news for the North American trucking industry according to the latest Truckload Volume Index report from DAT.

Read More →

Carrier Transicold Extends Refrigerated Trailer Life

Fleet Refresh enables refrigerated fleets to replace aging transport refrigeration units instead of entire trailers, while adding Lynx Fleet telematics and BluEdge service coverage.

Read More →

FTR Says Freight Rates Surged in May

FTR's Trucking Conditions Index surged to a record high in May, the analytics firm reports.

Read More →

Meet HDT's Truck Fleet Innovators at Heavy Duty Trucking Exchange

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for HDTX, September 23-25.

Read More →

Enhance Fleet Performance with High-Efficiency Auxiliary Power Units

Drive sustainable cost savings while increasing driver comfort during short- and long-haul logistics operations.

Read More →

Is Your Parts Procurement Process Reactive or Proactive?

Ready to revamp your parts procurement process? Learn how now with “Strategic Parts Purchasing: A Process Checklist”

Read More →

What Trucking Events are Happening in 2026?

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

Truckload Rates Keep Rising as Tight Capacity Fuels Freight Market Recovery

Spot and contract rates continued climbing in May and June, not because freight demand is surging, but because fewer trucks and drivers are available.

Read More →

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →