Inside the Tennis-Ball-Bounce Economic Recovery [Commentary]

Freight Economy Q3 Rebound Outpaces General Economy

When we drilled into third-quarter GDP to look at the segments of the economy linked to freight demand, the results far exceeded our forecast.

by Avery Vise, FTR

December 1, 2020

The parts of the GDP related to freight out-performed the general economy – but we're still not back to normal freight volumes.

Graph: FTR

3 min to read

Even during widespread lockdowns this spring, we knew the third quarter of this year would post strong economic growth. It was simple math. Following the deepest economic contraction ever in a single quarter, we were bound to see very strong quarter-over-quarter growth if commerce returned to anything approaching normal. When we got the third quarter numbers for U.S. Gross Domestic Product, we saw what we expected. However, when we drilled down to look at the segments of the economy linked to freight demand, the results far exceeded our forecast.

GDP plunged by an unprecedented 31.4% on a quarter-over-quarter seasonally adjusted annualized basis in the second quarter, but it soared by an unprecedented 33.1% in the third quarter. However, keep in mind the realities of math: A gain larger than the loss preceding it does not indicate full recovery. Growth is off a smaller base, so you need a far larger percentage increase than the loss to get back to where you started. FTR does not expect the level of GDP to recover to where we were at the end of 2019 until sometime in the second quarter of 2021.

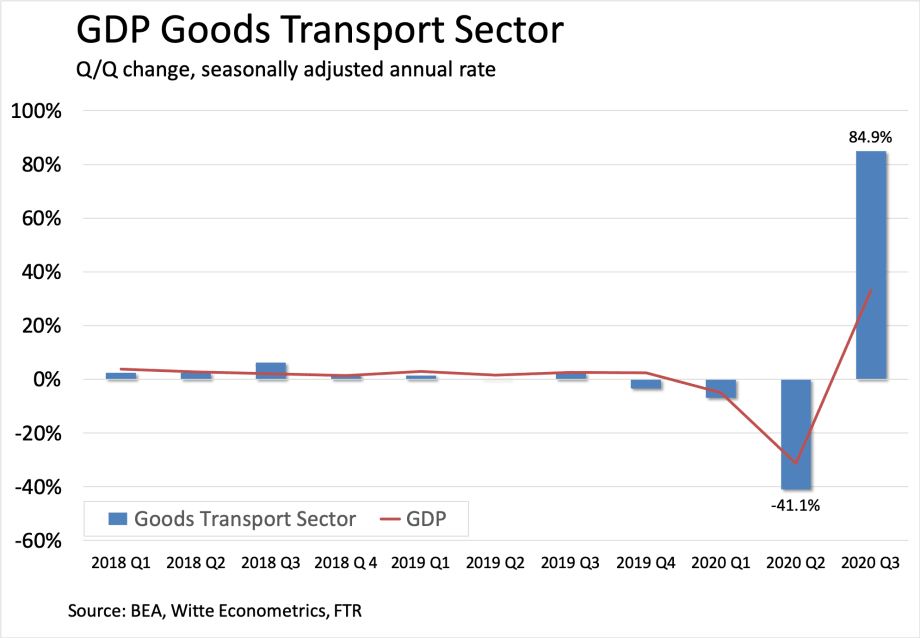

FTR also tracks what we refer to as GDP Goods Transport Sector – the part of the economy that drives freight transportation volume. The goods sector took a slightly deeper hit in the second quarter than the overall economy did, at a drop of 41.1%. One reason is that the sharp reduction in imports during the quarter served to bolster GDP slightly, because GDP counts imports as a negative. However, goods imports count as a positive in the calculation of the GDP Goods Transport Sector.

In the third quarter, GDP Goods Transport surged by an astounding 84.9%. The actual level fell short of the same quarter last year by just 0.5%, and it basically matches Q4 of last year.

Why was growth so extraordinary? One factor is the one noted above: Goods imports surged in the third quarter.

Also, due to the pandemic, consumers have limited opportunity for travel and entertainment, resulting in a shift of spending into goods rather than services. Total consumer spending in September was 2.4% below February, seasonally adjusted, according to the Bureau of Economic Analysis. However, spending on services was 6.3% below February, while spending on goods was 7.7% higher. This substitution of goods for services likely will continue to some degree until a vaccine is widely available, but that does not necessarily mean that goods demand will continue to grow. Surging COVID-19 cases and the lack of more stimulus from Washington are significant risks that could slow that growth.

Another major factor in the strong GDP Goods Transport rebound is extraordinarily lean retail inventories relative to sales. In three of the past four months, the ratio of inventories to sales and retail was the lowest on record. The push for more inventory heightens pressure for freight movements beyond the pressure resulting from higher sales themselves.

The GDP Goods Transport Sector is not the same as actual freight volume, which still has not fully recovered for various reasons. Spot market volumes – especially in dry van and refrigerated – are running at record levels, but much of that pressure results from disrupted supply chains, lagging driver capacity, and the need to rebuild retail inventories. The consumer sector has more than fully recovered, but the industrial sector has not.

More Fleet Management

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →

July Imports Poised to Set Container Record

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

Read More →

HDT Announces 2026 Truck Fleet Innovator Finalists

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Read More →

Van Spot Rates Top Contract Rates for First Time Since 2022

There’s more good economic news for the North American trucking industry according to the latest Truckload Volume Index report from DAT.

Read More →

Carrier Transicold Extends Refrigerated Trailer Life

Fleet Refresh enables refrigerated fleets to replace aging transport refrigeration units instead of entire trailers, while adding Lynx Fleet telematics and BluEdge service coverage.

Read More →

FTR Says Freight Rates Surged in May

FTR's Trucking Conditions Index surged to a record high in May, the analytics firm reports.

Read More →

Meet HDT's Truck Fleet Innovators at Heavy Duty Trucking Exchange

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for HDTX, September 23-25.

Read More →

Sponsored•July 1, 2026

Enhance Fleet Performance with High-Efficiency Auxiliary Power Units

Drive sustainable cost savings while increasing driver comfort during short- and long-haul logistics operations.

Read More →