Trailer Orders Hold Steady in January as Backlogs Rebuild

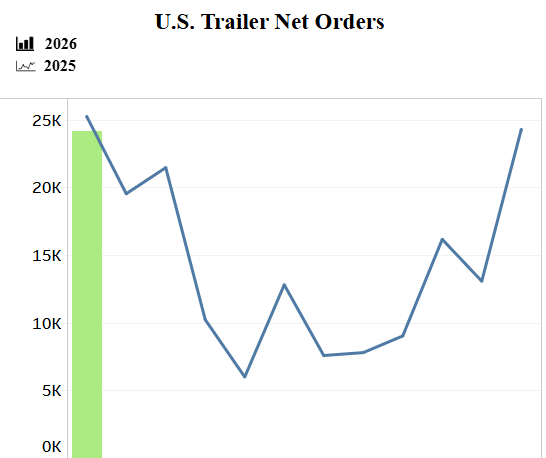

FTR says net trailer orders are flat month over month at 24,206 units, with 2026 orders still trailing last year.

U.S. trailer orders remain flat, according to FTR and Associates.

FTR and Associates

U.S. trailer net orders were essentially flat month over month in January, totaling 24,206 units. Still, according to FTR, those numbers are sustaining the stronger trailer market momentum that emerged late last year.

FTR reported that January orders were down 4% year over year and trailed the 10-year January average of 26,340 units. The analyst firm said the steady pace reflects a market that has found firmer footing after much of 2025’s volatility.

Even so, FTR noted, the 2026 order season -- spanning September 2025 through January 2026 -- remains down 16% compared to the same period a year earlier.

Some Signs of Recovery

FTR attributed January’s performance to several converging factors. These include the ongoing release of deferred orders from September through November and improving carrier fundamentals.

The firm noted its Trucking Conditions Index reached its strongest level since February 2022 in December, signaling healthier operating conditions for fleets.

Firmer freight rates and tighter capacity utilization also supported trailer demand. Spot rates posted outsized increases in December and again in January, driven in part by weather disruptions.

At the same time, some fleets appear to be advancing equipment purchases ahead of potential tariff-related cost pass-throughs and amid improved capital planning visibility tied to greater regulatory clarity in the Class 8 market.

Production rose in line with seasonal expectations in January but remained subdued, hovering near the lowest levels since the fourth quarter of 2010.

Net orders exceeded build by a wide margin, pushing backlogs higher sequentially. However, backlogs were still substantially below January 2025 levels.

“Positive indicators from the truck freight market and improved regulatory clarity are much-needed boosts to the U.S. trailer market,” said Dan Moyer, senior analyst, commercial vehicles at FTR. “But manufacturers and fleet purchasers still must deal with cost inflation and trade uncertainty that continue to shape pricing and demand.”

Trade Issues Complicate Matters

Moyer pointed to ongoing trade developments as a key variable in boosting trailer sales.

The Trump administration reportedly is considering a narrower approach to certain Section 232 steel and aluminum tariffs. That move could ease cost pass-through pressures at the margin. No formal policy change has been announced.

However, on Feb. 20, the United States Supreme Court struck down President Trump’s tariffs as unconstitutional.

Meanwhile, Moyer noted that trade risk in the van segment has become more tangible with the advancement of an antidumping and countervailing duty investigation being conducted by the U.S. Department of Commerce and the International Trade Commission.

That investigation is looking into allegations of unfair trade practices by foreign trailer manufacturers from Canada, China, and Mexico. The American Trailer Manufacturers Coalition and other industry groups allege that foreign trailer manufacturers are selling units at less than fair value and receiving government subsidies, which are harming the U.S. trailer industry.

The ITC is expected to issue preliminary determinations regarding the investigations, which could lead to duties being imposed on imports from these countries.

Although any resulting changes would likely be months away, Moyer said the investigation is already influencing sourcing strategies and pricing decisions.

Overall, FTR said existing metals tariffs and the advancing van investigation are likely to keep costs elevated and demand selective, even as freight conditions show signs of sustained improvement.

More Equipment

EPA Proposal Could Ease 2027 Truck Costs and Buying Uncertainty

The proposal doesn't change the tougher NOx standard, but it would revise key implementation requirements that manufacturers say have driven up costs and complicated fleet purchasing decisions.

Read More →

Cummins, Paccar Ease DEF Derates After EPA Guidance

Updated diesel engine software gives truck operators more time to address emissions-system issues while staying compliant with EPA emissions standards.

Read More →

America at 250: How the Truck Helped Connect a Continent

America was founded on revolutionary ideas, but it was built by movement. For 250 years, the nation has depended on ever-better ways to move people, products, and prosperity across a vast continent. No machine has carried that mission further — or more faithfully — than the truck.

Read More →

Mack Unveils America 250 Tribute Truck to Celebrate Nation's Semiquincentennial

Just in time for the Fourth of July! Mack unveils a brand-new patriotic, limited-edition, red, white, and blue truck wrap.

Read More →

Enhance Fleet Performance with High-Efficiency Auxiliary Power Units

Drive sustainable cost savings while increasing driver comfort during short- and long-haul logistics operations.

Read More →

Rush Expands Gulf Coast Peterbilt Network With Louisiana Acquisition

The expanded Rush network gives fleets additional sales, service, leasing and collision repair support across Louisiana's major trucking markets.

Read More →

Photos: Shell SuperRigs Light Up Bristol Tennessee

Kenny Ziglar II of Rawlins, Wyo., captured Best of Show honors for the second consecutive year with his 2007 Peterbilt 379, nicknamed “Scrapin By,” at the 44th Annual Shell Rotella SuperRigs competition held June 25-27 at Bristol Motor Speedway in Bristol, Tenn.

Read More →

Waabi, Volvo Claim Breakthrough in Scaling Autonomous Trucking

Waabi says its AI-powered virtual driver successfully transferred to Volvo Autonomous Solutions' Volvo VNL Autonomous platform without retraining or additional data, a milestone the companies say could dramatically accelerate commercialization of autonomous trucks.

Read More →

Why the Mack Pioneer Signals a New Era in Class 8 Truck Design

After a public-road drive through eastern Pennsylvania, one thing became clear: Mack's new Pioneer isn't simply packed with technology -- it's been engineered around the driver in ways that could redefine long-haul trucking.

Read More →

Mack Defense Secures $47 Million to Continue Military Dump Truck Production

President Trump visited Mack Defense’s Macungie, Pennsylvania, facility on June 23 to tout a $47 million Heavy Dump Truck order.

Read More →