Economic Growth to Continue Throughout 2012

Economic growth is expected to continue in the United States throughout the remainder of 2012, say the nation's purchasing and supply executives in their spring 2012 Semiannual Economic Forecast

Economic growth is expected to continue in the United States throughout the remainder of 2012, say the nation's purchasing and supply executives in their spring 2012 Semiannual Economic Forecast.

Expectations for the remainder of 2012 continue to be positive in both the manufacturing and non-manufacturing sectors.

These projections are part of the forecast issued by the Business Survey Committee of the Institute for Supply Management.

Manufacturing Summary

Almost two-thirds (66%) of respondents from the panel of manufacturing supply management executives predict revenues will be 9.5% greater in 2012 compared to 2011, 15% expect a 12.1% decline, and 19% foresee no change.

This yields an overall average expectation of 4.5% revenue growth among manufacturers in 2012, which is a modest reduction of 1 percentage point from December 2011 when the panel predicted a 5.5% increase in 2012 revenues.

Manufacturing is an important economic indicator for truck freight.

With operating capacity at 81.6%, an expected capital expenditure increase of 6.2% and prices paid expected to increase a modest 0.4% from now through the end of 2012, manufacturers are positioned to grow revenues and contain costs through the remainder of the year.

"With 16 out of 18 industries within the manufacturing sector predicting growth in 2012 over 2011, manufacturing continues to demonstrate its strength and resilience in the midst of global economic uncertainty and volatility," says Bradley J. Holcomb, chair of the ISM Manufacturing Business Survey Committee. "Capacity utilization is at historically typical levels and manufacturers are continuing to invest in their businesses. The positive forecast for revenue growth and modest price increases will drive a continuation of the recovery in the manufacturing sector."

The 16 industries reporting expectations of growth in revenue for 2012 - listed in order - are:

- apparel, leather & allied products;

- machinery

- primary metals

- petroleum & coal products

- plastics & rubber products

- furniture & related products

- electrical equipment, appliances & components

- nonmetallic mineral products

- transportation equipment

- printing & related support activities

- textile mills

- miscellaneous manufacturing

- food, beverage & tobacco products

- chemical products

- paper products

- fabricated metal products

Non-Manufacturing

More than 50% of non-manufacturing purchasing and supply executives expect their 2012 revenues to be greater by 9.9% than in 2011. Overall, respondents currently expect a 4.8% net increase in overall revenues, which is greater than the 3.1% increase that was forecast in December 2011.

"Non-manufacturing will continue to grow for the balance of 2012," says Anthony S. Nieves, chair of the ISM Non-Manufacturing Business Survey Committee. "Non-manufacturing companies reflect strong capacity utilization coupled with forecasted revenue growth. This indicates that non-manufacturing companies are streamlined and efficient. Overall costs have been contained despite strong increases for fuel and petroleum-based products. Slow employment growth continues to be a challenge for the non-manufacturing sector."

For the full report, go to www.ism.ws.

More Fleet Management

Jamie Hagen Gets Real About Running a Small Fleet in an Uncertain Economy

Small fleet owner Jamie Hagen says new legal risks, volatile fuel prices, and a changing freight market are forcing small carriers to rethink how they operate -- and what they can afford.

Read More →

Jamie Hagen Gets Real About Freight, Fuel Prices, Safety, and Small-Fleet Survival

Running a small trucking fleet right now isn’t easy, especially right now. And Jamie Hagen doesn’t sugarcoat it.

Read More →

Jamie Hagen Gets Real About Freight, Fuel Prices, Safety, and Small-Fleet Survival

Running a small trucking fleet right now isn’t easy, especially right now. And Jamie Hagen doesn’t sugarcoat it.

Read More →

Data Lock‑In or Integration Lock‑Out?

Data fragmentation is costing dealerships, OEMs, fleets, and upfitters millions. Here’s why interoperability may be the fix the trucking industry needs.

Read More →

What Trucking Fleets and Brokers Need to Know About This Supreme Court Case

In May, the U.S. Supreme Court ruled that freight brokers can be held liable for damages if a truck they have contracted with is involved in an accident. Listen as this transportation attorney breaks down the ruling and its implications for the trucking industry.

Read More →

The Trucking Industry’s Threat Intelligence Gap

The trucking industry has no shortage of cybersecurity reports and cargo crime statistics. What it lacks is timely, operational intelligence that fleets can actually use.

Read More →

Truck Crash Rates Are Down. So Why Do Insurance Costs Keep Rising?

ATRI’s latest research points to litigation, social inflation, and soaring claims costs as key drivers behind record-high liability premiums for trucking fleets. But there are things motor carriers can do.

Read More →

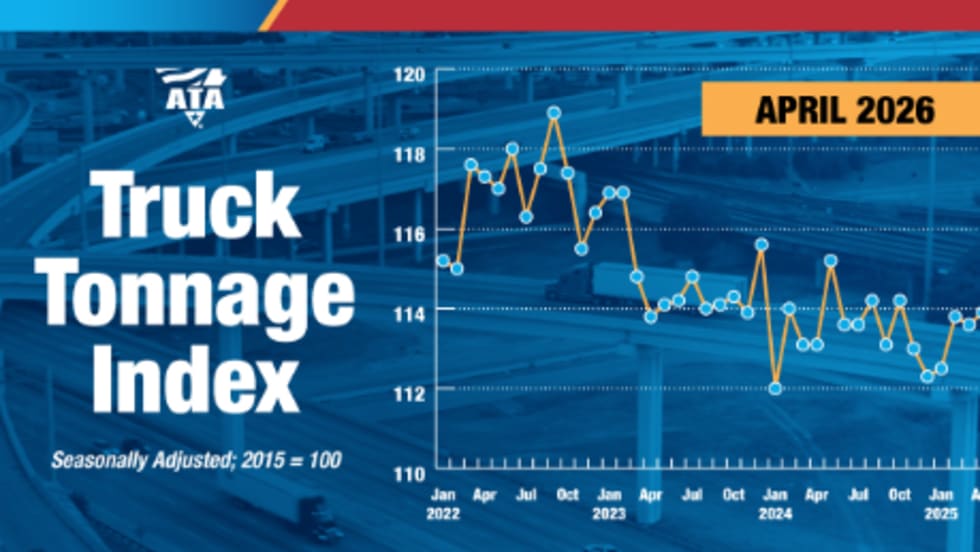

ATA Truck Tonnage Holds Steady in April at Highest Levels Since 2022

ATA’s For-Hire Truck Tonnage Index was unchanged in April after a strong March gain, with freight volumes remaining at their highest levels since late 2022.

Read More →

Fleetworthy Launches Connected Platform for Fleet Readiness Across Safety and Compliance, Toll Management, and Weigh Station Bypass

Fleetworthy has unveiled three major product launches it says mark a new era in fleet readiness.

Read More →

Behind the SCOTUS Broker Ruling Part 1

Transportation attorney Greg Feary breaks down the recent Supreme Court decision that brokers can be held liable for damages in truck accidents and what it means for the trucking industry going forward.

Read More →