More from Jeff Kauffman's Behind the Numbers: What Can Trucking Expect from Inflation and Interest-Rate Numbers? [Analysis]

What Do Q1 Freight Volumes Tell Us?

Given the uncertainty in the larger economy, what do the various volume lead indicators for trucking telling us? HDT's Contributing Economic Analyst explores the numbers.

March 26, 2023

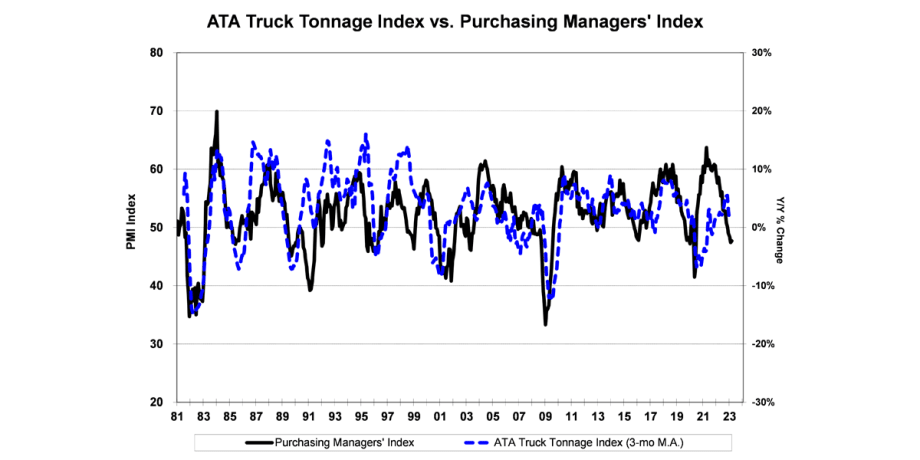

When you compare the Purchasing Managers’ Index with the American Trucking Associations’ tonnage numbers, you can see the PMI tends to lead truck tonnage in a fairly accurate direction.

Source: American Trucking Associations, Institute of Supply Management

3 min to read

In mid-March, many less-than-truckload carriers reported quarter-to-date tonnage and yield results that had volumes down about 6.2%, below expectations.

While the gross of fuel yields are up about 6.2%, roughly in line with our view, we thought it would be helpful to discuss various volume lead indicators for trucking as a whole. Given the uncertainty in the larger economy, what are these numbers telling us?

Freight Volumes

Volumes were slightly above expectations in January and below expectations in February, which we attribute to better-than-expected winter weather across much of the country in January. Cass shipments declined 3.2% in January from the previous month, but normal December-to-January drops are about 8% — so shipments improved versus normal seasonality.

Meanwhile, spot truck rates were relatively stable, even as winter came back with a fury on the West Coast and the northern states.

Rail volumes have been a tale of two cities, with commodity volumes (excluding coal, grain and intermodal) showing surprising strength (up 2.3% through February). But intermodal volumes were down about 8.2% year-to-date, owing largely to the inventory-reduction efforts going on with retailers. We also have seen weakness in chemical volumes on inventory destocking (although that is improving in recent weeks), lumber (on housing), corrugated boxes (destocking) and coal (warmer winter).

We believe much of what we have seen so far is not the weakening economy, but a meaningful inventory destocking of the large inventory builds a year ago.

Looking Forward

So, what should the go-forward view be? Normally, March makes the first quarter. This year, the drop in inbound container shipments (down 25% in February) is likely to leave that push lacking.

Nonetheless, many retailers have been reporting that their inventory adjustments are close to complete, and some of the retail-facing trucking companies we speak with believe more normal seasonality will begin to kick in sometime during the second quarter.

In our view, we haven’t really seen a meaningful slowdown in the economy yet related to the Fed’s interest rate increases. Is that still ahead of us?

The Purchasing Managers’ Index from the Institute of Supply Management, while not a perfect correlation, tends to lead truck tonnage in a fairly accurate direction. We get a similar graph if looking at the leading economic indicator index or the Cass Shipment Index. However, the PMI tends to lead truck tonnage with the greatest predictive value. The continued weakening of this index suggests that we could be in for slower truck tonnage in the quarters ahead.

Meanwhile, although the retail destocking may be nearing an equilibrium, manufacturing inventories overall remain bloated. We are starting to see layoff announcements beginning in industries other than technology.

Lower Demand, Lower Rates

Along with this, we expect to see a further weakening in used-vehicle prices as truck OEMs ramp up new-truck production. ACT Research says used Class 8 vehicle prices could weaken another 40% this year. This means buyers of truck equipment won’t have as much in collateral to trade, in addition to facing rising interest rates.

The point is, despite retail reports that we could be getting closer to the end of the big inventory destocking, these lead indicators for truck volumes continue to predict lower demand. And lower freight rates indicate that demand has not yet recovered.

In our view, growth risk remains to the downside, as the Federal Reserve continues to raise rates to battle inflation and the cost of equipment continues to rise. We expect comparisons to improve from destocking-related weak levels, but perhaps the weaker economy remains ahead of us.

This analysis appears in the April 2023 issue of Heavy Duty Trucking.

Topics:Fleet Management

Subscribe to Our Newsletter

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →