HDT Fact Book 2022: Out-of-Sync Supply Chains & Logistics Transformation

The U.S.-based supply chains remain out of sync. HDT collected the logistics data you need to know to adapt to short- and long-term industry changes.

August 31, 2022

2 min to read

Continued supply chain disruptions, scarce capacity, surging customer demand and the continued growth of e-commerce has driven freight rates higher, but also has pushed shippers to depend more on third-party logistics companies and develop private or dedicated fleets.

As the inflation rate has hit record highs so far in 2022, sectors that were booming, such as durable goods, retail, housing, home improvement, and e-commerce, saw a slowdown — although hospitality, restaurants and airlines were still recovering strongly.

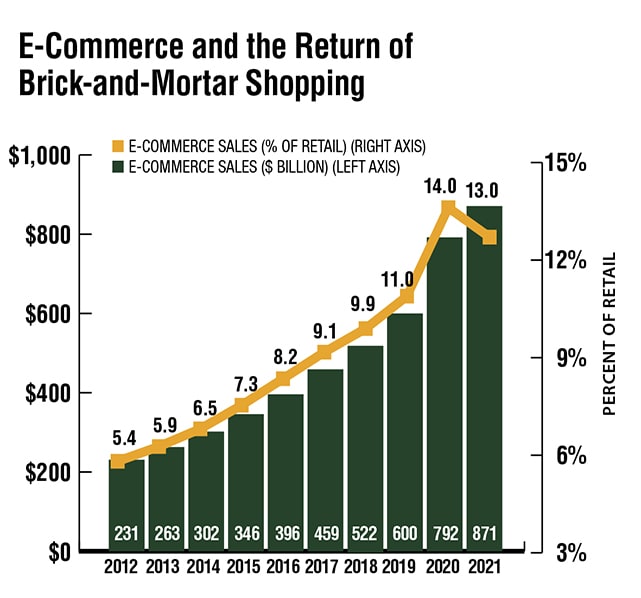

E-commerce grew by 10% to $871 billion – 13% of all U.S. retail sales. The resulting demand for last-mile delivery benefited the parcel sector, which grew by 15.6%. However, there is evidence that e-commerce has begun slowing as shopper return to brick-and-mortar shopping, with e-commerce sales as a percent of retail dropping for the first time in a decade.

Source: CSCMP State of Logistics Report 2022/Kearney

Some modes and nodes, such as e-commerce and the last-mile delivery capacity it requires, will retain structurally high demand, according to the latest annual State of Logistics Report from the Council of Supply Chain Management Professionals. However, some supply bottlenecks, such as congested port capacity and the driver shortage, are not easily solved.

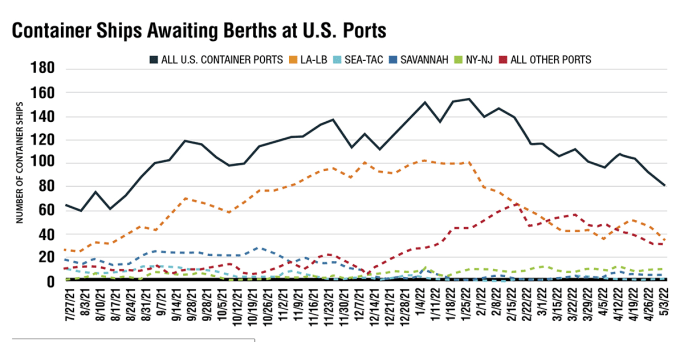

In late 2021 and early 2022, the number of container ships waiting for a dock at a U.S. port more than doubled, peaking at more than 150 in early February. Levels have declined since then, but are still higher than historical levels for many ports. This chart depicts the total number of container ships waiting for an available dock at U.S. ports overall (solid line) and select major port complexes (dashed lines).

Source: USDOT Supply Chain Tracker

The result is that U.S.-based supply chains remain “out of sync” in 2022, according to the report, presented by Penske Logistics and authored by consultancy firm Kearney. And that has led to higher costs for shippers. The report found that U.S. business logistics costs climbed in 2021 by 22.4% to $1.85 trillion, representing 8% of the $23 trillion GDP. By contrast, in 2020, those costs fell by 4%, driven down by the impact of the pandemic.

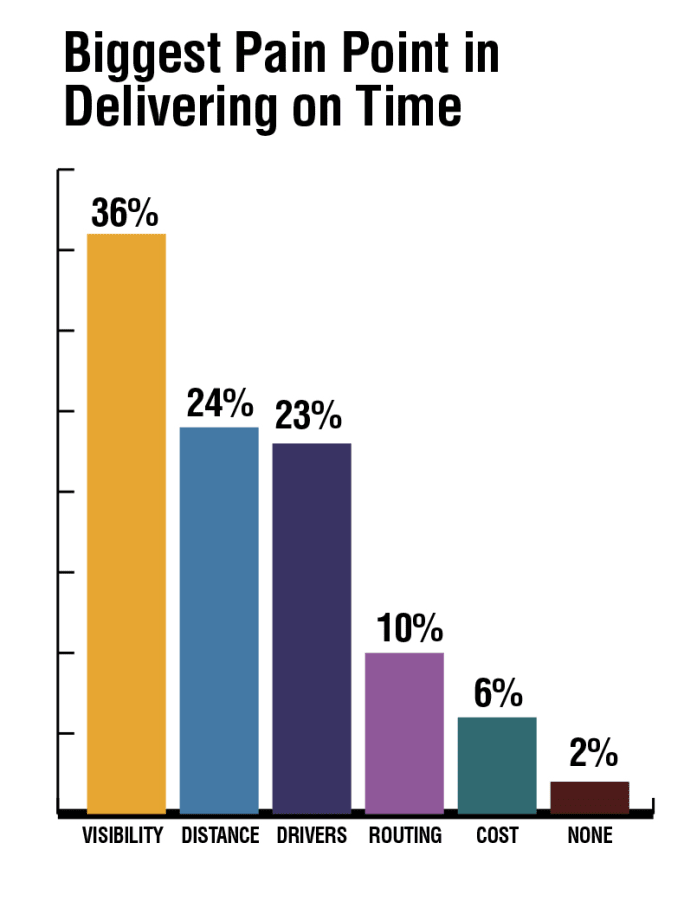

A survey of 500 retailers in late 2021 turned up opportunities for fleet and logistics companies in last-mile delivery. 98% of respondents to the survey, commissioned by data-led delivery and fulfillment cloud platform provider Bringg, admitted to having pain points when it comes to delivering on time. The biggest was real-time order visibility tracking, at 36%, which was almost triple the year before. While cost was not a big pain point, among respondents who were highly satisfied by the delivery/fulfillment options they provide, the challenge of cost rises to 42%. Almost one in four companies struggle to meet delivery times because of travel distance. This challenge, along with a lack of visibility, points to delivery operations that are not set up for hyperlocal delivery.

Source: 2022 Bringg Barometer: The State of Retail Delivery & Fulfillment

The report found that the logistics sector has begun to adapt to short-term changes, in ways that may reveal long-term solutions to the disruptions afflicting supply chains.

For instance, a window of opportunity has opened for 3PLs to become more full-fledged, consultative partners to shippers. Last year was a huge year of growth for 3PLs, as well as what Armstrong & Associates called an “astounding” number of mergers and acquisitions. However, the firm said, “the true leaders were those 3PLs with strong carrier management skills that have technologically innovated, allowing them to efficiently tap long-standing carrier relationships to cover shipper demand, versus being over-reliant on using load boards or traditional means to buy capacity at spot market rates.”

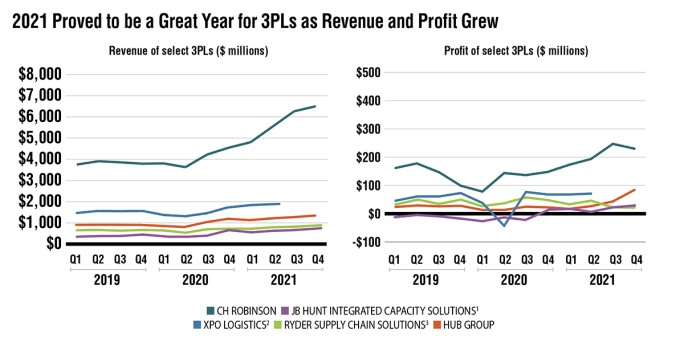

Third-party logistics providers earned robust revenues and profits in 2021. The big players who were able to invest in additional capacity and automation, as well as offer integrated solutions built around data insights, benefitted the most from the tumultuous supply chain.

Notes: 1 Profit shown is operating income; 2 Profit shown in operating income. Note XPO spun off logistics segment in August 2021 (GXO Logistics); 3 Profit shown is EBIT.

Source: Capital IQ; Kearney Analysis

The M&A surge wasn’t limited to 3PLs, according to the State of Logistics report, with deals made to reposition companies to better serve the demands of e-commerce — especially in less-than-truckload shipping. UPS Freight, AAA Cooper, and Midwest Motor Express were LTLs that changed hands last year. Another driver for M&A activity was technology-driven consolidation, such as Uber Freight’s acquisition of Transplace.

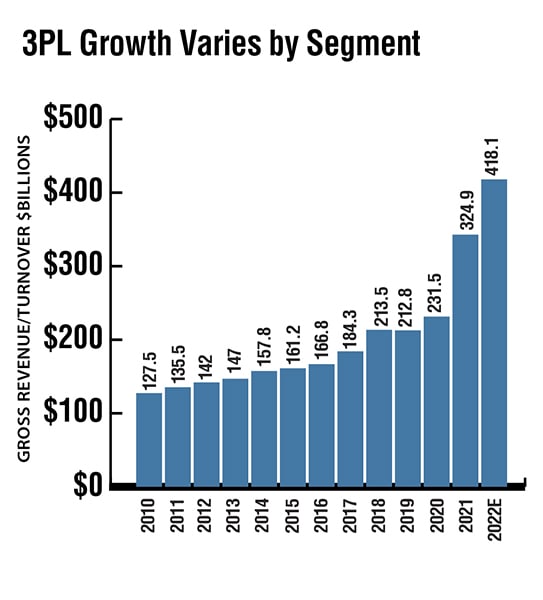

Year-over-year, 2021 saw the fastest 3PL growth since Armstrong & Associates began estimating the market size in 1995, but growth differed by segment. While the Dedicated Contract Carriage and Value-Added Warehousing and Distribution segments had a great year with 15% and 17% gross revenue growth respectively, most of the overall growth came from International Transportation Management, with 75% year-over-year growth, and Domestic Transportation Management with 52.4% growth.

Source: Armstrong & Associates

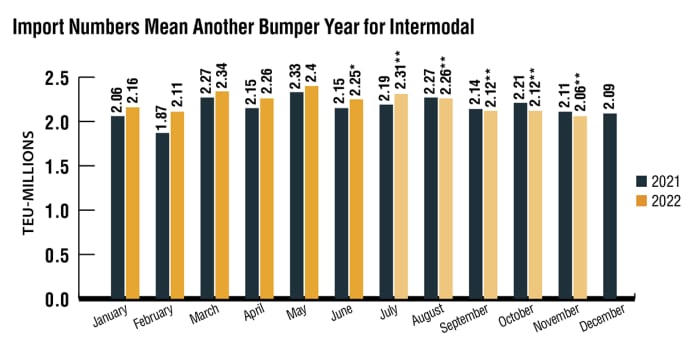

Imports at the nation’s major retail container ports were at near-record volume for the first half of 2022 as retailers worked to meet still-strong consumer demand and protect themselves against potential disruptions at West Coast ports, according to the Global Port Tracker from the National Retail Federation and Hackett Associates. The first six months of 2022 are expected to total 13.5 million TEU (Twenty-Foot Equivalent Units – one 20-foot container or its equivalent), up 5.3% year over year. Imports for all of 2021 totaled 25.8 million TEU, a 17.4% increase over 2020’s previous annual record of 22 million TEU. The report authors see the beginnings of a decline in the growth rate of imports in the second half of the year as the economy responds to the anti-inflation policy measures taken by the Federal Reserve. Despite this, the report points to continued shipping capacity constraints. * Estimated. ** Forecast.

Source: National Retail Federation

This data and analysis first appeared in the August 2022 special Fact Book issue of Heavy Duty Trucking.

Subscribe to Our Newsletter

More Fleet Management

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →

July Imports Poised to Set Container Record

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

Read More →