HDT Fact Book 2022: Supply Chain Keeps Truck Makers from Overbuilding

Check out this year's HDT Fact Book, which dives into the industry's most important numbers on truck orders, trade cycles, the used-truck market and more.

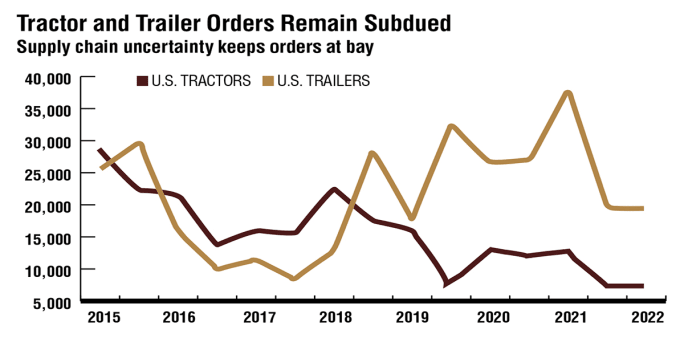

It was the same story every month for Class 8 orders: supply chain constraints affected volumes, and will probably continue to. Reporting on industry analysis of the order numbers each month, HDT’s headlines included words such as: frozen, weak, subdued, moderate, cautious, controlled… and the most optimistic? “Modest gain.”

ACT Research’s Class 8 Tractor Dashboard, a report that paints a comprehensive picture of trends impacting the industry, suggests a “gradual erosion” of the Class 8 market demand into the second half of 2022.

But, Kenny Vieth, ACT’s president and senior analyst, says this is not a “cliff event.”

“With a recession in 2023 now our base case, we think the dashboard reading, while negative, still suggests a better outcome for Class 8 than was the case in our last two recessions [COVID 2020 and the 2008-09 Great Recession], as supply constraints have kept the industry from overbuilding in the leadup to the downturn,” Vieth wrote in a July press release.

Class 8 truck orders continue to be subdued this year, as 2023 build slots remain restricted due to limited visibility into future conditions surrounding material costs and lead times. OEMs are carefully controlling Class 8 orders while still working to increase build rates. Semiconductors, tires, and other key components remain in short supply and continue to limit production.

Source: Act Research

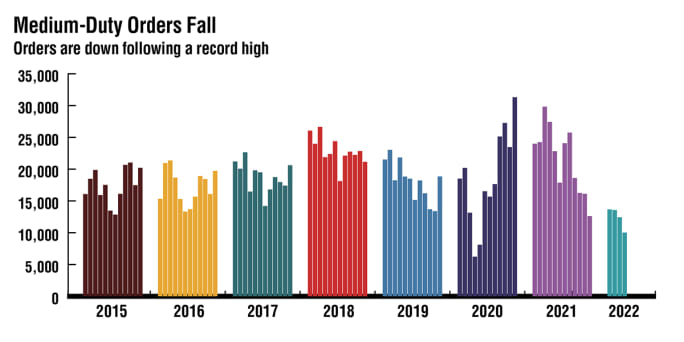

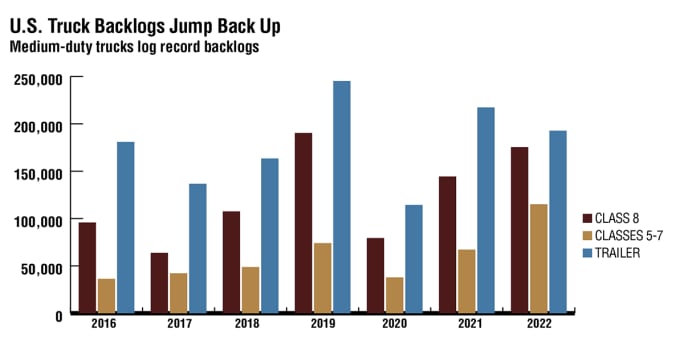

Like their larger counterpart, U.S. net orders for medium-duty (Class 5-7) vehicles have been impacted by supply chain disruptions. However, preliminary net orders in June show a bright spot for the segment. “Classes 5-7 orders rose sequentially, and when seasonally adjusted, data represents the third highest seasonally adjusted total of the year, thus far," according to ACT Research. Note: Available data for 2022 includes February-May.

Source: Act Research

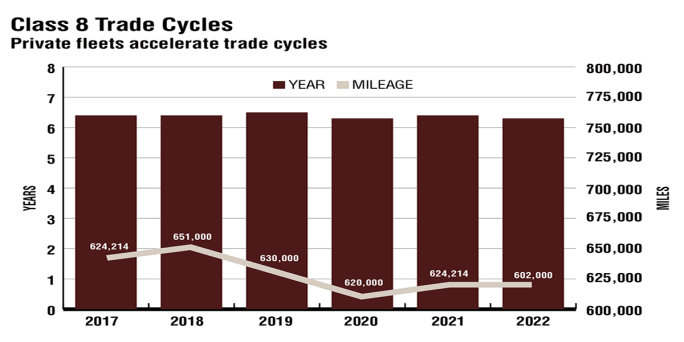

Respondents in the National Private Truck Council benchmarking survey accelerated their heavy-duty equipment trade cycles to a brisk 6.3 years, tied for the fastest equipment turns in the history of the survey. This, combined with lower annual mileage, produced the quickest trade cycles as measured by mileage. This year’s survey reveals trade cycles accelerated from last year’s 6.4 years and 620,000 miles for the average Class 8 tractor. The peppier trade cycle figures would seem to contradict the equipment shortages, which forced private fleets to extend their equipment replacement cycles.

When fleets that lease the majority of their equipment are removed, the trade cycles lengthened slightly to 6.9 years and 662,440 miles. That compares to the 6.6 years and 656,000 miles achieved last year. For comparison purposes, in 2015, trade cycles for this same class averaged 8.74 years and 717,000 miles reported last year.

Source: National Private Truck Council’s Benchmarking Survey Report

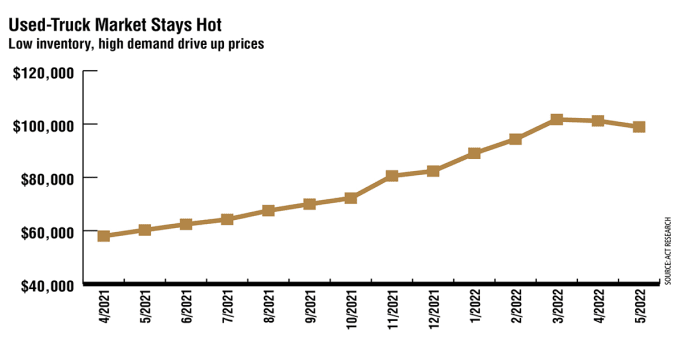

As backlogs surged in 2021 and 2022, prices for Class 8 used trucks have been rapidly escalating. For the first time since 2015*, the price of used trucks reached over $100,000. In March 2022, the average retail selling price for a Class 8 used truck was $101,716. In the first 5 months of 2022, that average for a used truck was about $97,000. In 2021, the average was about $64,000. By comparison, between 2015 and 2020, the average price remained below $57,000. *Available used truck price data begins January 2015.

Source: ACT Research

Autonomous Vehicle Rules

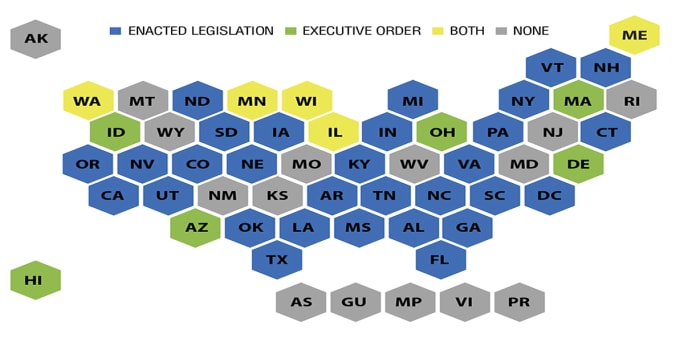

As the technology for autonomous vehicles continues to develop, it may be necessary for state and municipal governments to address the potential impacts of these vehicles on the road. Each year, the number of states considering legislation related to autonomous vehicles has gradually increased. Since 2012, at least 41 states and Washington, D.C., have considered legislation related to autonomous vehicles. Currently, 21 states have enacted legislation regarding it.

Source: National Conference of State Legislatures, Autonomous Vehicles Legislative Database

According to analysts, such as FTR, OEMs were not confident this year that the supply chain would improve in the short term, so they began carefully controlling the number of official Class 8 orders. This was to keep creeping backlogs to a manageable level, and not overbook production schedules. Note: 2022 reflects backlog numbers from February-May (the latest data available at the time of publication.)

Source: ACT Research

This data and analysis first appeared in the August 2022 special Fact Book issue of Heavy Duty Trucking.

2022 Fact Book

The Trucking Industry Numbers Impacting the Bottom Line

Heavy Duty Trucking’s annual Fact Book is designed to provide a snapshot of the current state of the industry, where it’s been, and where it’s going. 2022 is the eighth year for the HDT Fact Book. Dive into the other topics:

America was founded on revolutionary ideas, but it was built by movement. For 250 years, the nation has depended on ever-better ways to move people, products, and prosperity across a vast continent. No machine has carried that mission further — or more faithfully — than the truck.

Kenny Ziglar II of Rawlins, Wyo., captured Best of Show honors for the second consecutive year with his 2007 Peterbilt 379, nicknamed “Scrapin By,” at the 44th Annual Shell Rotella SuperRigs competition held June 25-27 at Bristol Motor Speedway in Bristol, Tenn.

Waabi says its AI-powered virtual driver successfully transferred to Volvo Autonomous Solutions' Volvo VNL Autonomous platform without retraining or additional data, a milestone the companies say could dramatically accelerate commercialization of autonomous trucks.

After a public-road drive through eastern Pennsylvania, one thing became clear: Mack's new Pioneer isn't simply packed with technology -- it's been engineered around the driver in ways that could redefine long-haul trucking.