ATRI Report Takes on Rising Trucking Insurance Costs

Despite strategies motor carriers are using to reduce premiums, most still reported rising insurance costs. One report says a more holistic strategy is needed.

Trucking insurance costs have been on the rise for a number of reasons, many outside the carrier's control.

Graph: ATRI

A new report analyzing the effect of the rising costs of insurance on trucking fleets found that despite strategies companies are using to reduce premiums, most motor carriers still faced rising insurance costs.

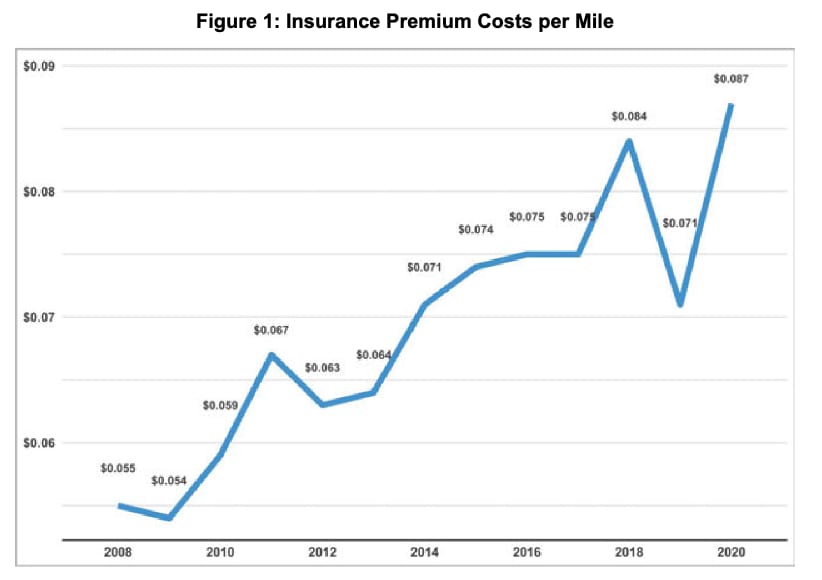

The American Transportation Research Institute notes that volatile and increasing insurance premiums have been a major industry concern. Its Analysis of the Operational Costs of Trucking report found that insurance premium costs per mile increased overall by 47% over the last 10 years, from 5.9 cents to 8.7 cents.

A new ATRI report, “The Impact of Rising Insurance Costs on the Trucking Industry,” found despite reductions in insurance coverage, rising deductibles, and improved safety, almost all motor carriers experienced substantial increases in insurance costs from 2018 to 2020.

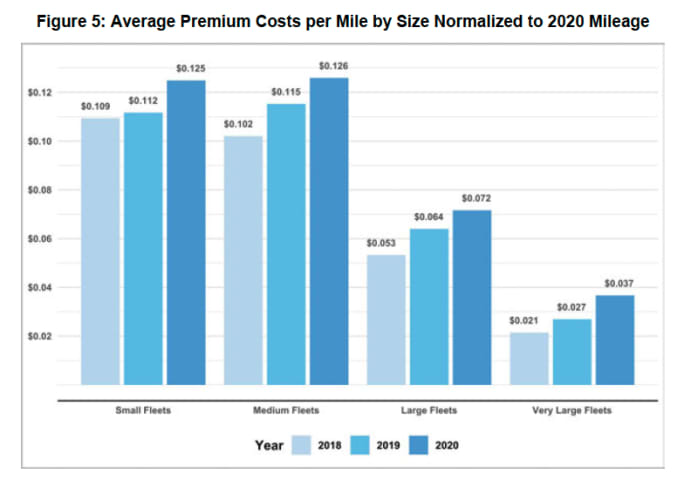

Premiums increased across all fleet sizes and sectors, with small fleets paying more than three times as much as very large fleets on a per-mile basis. Small fleets continue to pay more than twice as much per mile in premiums as large fleets, which pay almost twice as much per mile as very large fleets, ATRI reports.

Small fleets pay more for insurance than large fleets.

Graph: ATRI

One-third of respondents reported cutting wages or bonuses due to rising insurance costs, and 22% cut investments in equipment and technology — potentially creating future safety and driver shortage concerns.

However, in the short term, crash data confirms that carriers that raised deductibles or reduced insurance coverage were generally incentivized to reduce crashes in the subsequent year.

The report also describes a process for calculating the “Total Cost of Risk” in order to evaluate the scale and impact of rising insurance costs on a carrier’s long-term safety and financial viability, including safety investments in drivers, programs and technologies.

What’s Behind the High Cost of Trucking Insurance?

While truck-crash frequency and severity were on the rise from 2009 to 2018 (the time period used in ATRI’s analysis), the rate of insurance cost increases during this same period far exceeded the nominal rate increase in crashes.

Litigation also puts financial pressures on insurers, which are then passed on to motor carriers. And it's not just "nuclear verdicts." ATRI’s report on The Impact of Small Verdicts and Settlements in the Trucking Industry found that this category of litigation resulted in an average payment of between $406,386 and $449,792.

Economic conditions within the insurance industry have contributed to rate increases as well. Incurred losses for insurers of commercial vehicles grew annually between 2015 and 2019, for an overall increase of 50%. Losses for insurers parallel a general rise in claims, despite the fact that premiums have consistently risen at a higher rate. In response, some insurers are leaving the market altogether and others are reducing offered coverage limits.

“ATRI’s study corroborates the Triple-I’s research on rising insurance costs and social inflation: that increased litigation and other factors dramatically raise insurers' claim payouts,” noted Dale Porfilio, chief insurance officer of the Insurance Information Institute. “External factors that go well beyond carrier safety force commercial trucking insurance costs to increase, which then requires carriers to redesign their business strategies. The higher premiums ultimately tend to be passed along to consumers in the form of higher prices for goods and services.”

Trucking Fleet Responses to Higher Insurance

The report found that motor carriers’ most common response to increasing insurance rates was to decrease coverage levels in excess of $1 million, especially in very large fleets. While cutting back on excess coverage can reduce premium costs in the short run, it can also increase carriers’ exposure to nuclear verdict cases.

Higher deductibles are another tactic to reduce premium costs, but carriers that do so also expose themselves to higher out-of-pocket costs.

By covering a larger portion of losses per incident with higher insurance deductibles or self-insurance retention, carriers can secure lower premiums. The trend of rising deductibles and SIR suggests that medium, large and very large carriers have likely calculated that their out-of-pocket costs will be lower than net insurance cost increases.

For small fleets, however, many of these tactics are not an option. Small carriers with smaller profit margins may prefer to pay slightly higher premium costs over time rather than risk significantly higher out-of-pocket incident costs in the case of an incident, which could bankrupt a small fleet. With less available capital, smaller carriers also have fewer alternatives (such as self-insurance) to traditional deductible policies. And many insurers do not offer higher deductible options to small carriers in order to reduce excess risk that the carrier may not be able to handle.

ATRI’s research concluded that decreases in total coverage levels, or increases in deductibles or SIR, are unlikely to lower premiums meaningfully, unless the increase is substantial or occurs in conjunction with other unique carrier- or policy-specific changes.

Safety Technology

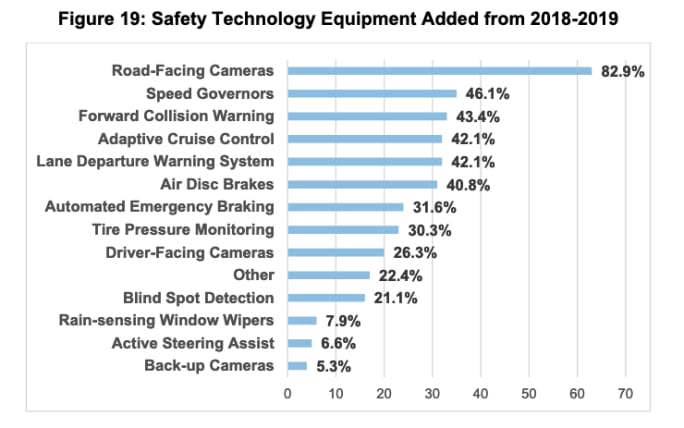

ATRI reported that 92% of its respondents adopted new safety technology in the last three years. It added that 56% implemented three or more new safety technologies. Road-facing cameras were reported with the highest frequency, followed by speed governors and forward-collision warning. However, the study found no significant correlations between newly adopted safety technologies and insurance premiums.

Forward-facing cameras are a technology that directly addresses insurance costs.

Graph: ATRI

Road-facing cameras have become a strategic tool for insurers, carriers and drivers, ATRI says, providing irrefutable safety documentation, thus lowering claims and defense costs.

All other safety technologies only indirectly influence insurance premiums. Theoretically, safety technologies lead to more favorable insurance rates by reducing crashes, but they do not directly improve rates in themselves.

Insurance industry experts said a carrier’s pursuit of safety technology in general was more important than implementing any particular technology. This is because investment in safety technology in general demonstrates that a carrier recognizes and proactively prioritizes the importance of reducing crashes.

ATRI concludes that industry experts as well as the findings in this report suggest that carriers should consider all safety-related matters and expenses — in addition to insurance — as part of a total cost of risk. This allows carriers to organize costs more effectively for the long term by emphasizing the impacts that all cost centers have on safety and the relationships between them.

A copy of the full report is available through ATRI's website.

Corrected: A misplaced decimal in an earlier version of this story led to a report of insurance costs rising from 59 cents per mile to 78 cents per mile; the correct figure is that it increased from 5.9 cents to 8.7 cents.

More Fleet Management

Enhance Fleet Performance with High-Efficiency Auxiliary Power Units

Drive sustainable cost savings while increasing driver comfort during short- and long-haul logistics operations.

Read More →

Is Your Parts Procurement Process Reactive or Proactive?

Ready to revamp your parts procurement process? Learn how now with “Strategic Parts Purchasing: A Process Checklist”

Read More →

What Trucking Events are Happening in 2026?

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

Truckload Rates Keep Rising as Tight Capacity Fuels Freight Market Recovery

Spot and contract rates continued climbing in May and June, not because freight demand is surging, but because fewer trucks and drivers are available.

Read More →

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →