What do Pandemic-Scrambled Retail Inventory Trends Mean for Trucking?

The inventories-to-sales ratio traditionally has been a key indicator for assessing near-term transportation demand. Right now they're very lean, which usually is good news for trucking – but there's a catch.

The largest drivers of freight demand are consumption and production. For the past year, the growth in consumption of has been unprecedented. The four largest month-over-month gains in retail sales have come since April 2020, largely driven by stimulus from Washington.

Production has not matched the trajectory, but the challenge has not been a lack of demand. For example, if you exclude the troubled aircraft industry, orders for durable manufactured goods have been running at record levels. Rather, the issue is supply of materials, components, and labor.

Another significant factor in the demand for freight transportation is inventories – or, more to the point, the relation of inventories to sales. The inventories-to-sales ratio traditionally has been a key indicator for assessing near-term transportation demand. Individual sectors – manufacturing, wholesale, and retail – have different norms for the ratio of inventories to sales, but as the ratio falls, we expect to see pressure for inventory replenishment, which bolsters freight volume beyond the period of initial consumer or manufacturing demand.

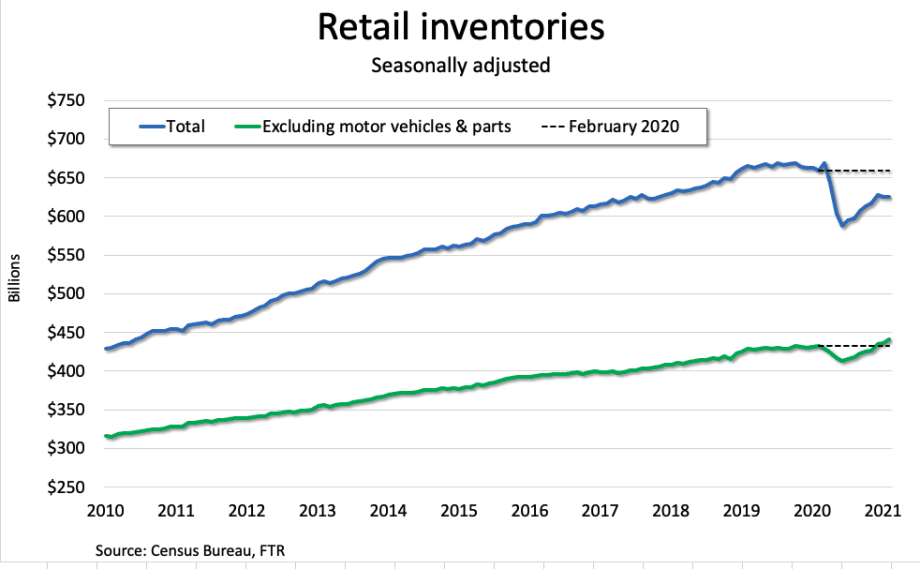

The pandemic produced wild swings in inventories-to-sales ratios due to abrupt changes in consumption and production. As of February, the most recent month for which data is available, the ratios for the manufacturing sector are roughly in line with where they were before the pandemic, and inventories in wholesale are noticeably leaner than they had been.

The most dramatic change has been in retail inventories. February saw an uptick in the ratio of inventories to sales following a record low retail inventories-to-sales ratio in January. With a huge jump in retail sales in March in the wake of the third round of stimulus, the inventories-to-sales ratio likely was as low as or even lower than January.

For trucking companies involved in hauling retail goods, this sounds like great news. It suggests that freight demand will outlive the bursts of consumption we have seen after each round of stimulus.

However, if we dig deeper, we find that a single sector – motor vehicles and parts – skews the data.

Motor vehicles are far more expensive than any other retail item, so changes in inventories or sales of automobiles and light trucks have an outsized effect on total retail inventories and sales, even when changes are small. During the pandemic, those changes have not been small. Sales have been robust, but their growth has been mostly in line with retail sales in general. The distortion comes from inventories.

Total retail trade inventories in February were down 5.1% year over year. However, inventories of motor vehicles and parts were down 17.1%. Excluding motor vehicles and parts, retail trade inventories were up 1.2%. That is not much growth, but it is growth. Of course, retail sales have been so strong that the ratio of inventories to sales is still extraordinarily low. But if sales weaken down the road, we will not necessarily see the same demand for replenishment that we would see if inventories were down on an absolute basis.

Aside from automotive, the only retail sectors with large declines in inventories during the pandemic are clothing stores and department stores – segments where lower inventories might not yield much sales pressure owing to the surge in e-commerce.

Automotive, however, faces a potentially crippling inventory crunch in the near term. While inventories are down quite sharply, retail sales of motor vehicles and parts were the highest on record in March. Meanwhile, automotive production during March was still about 8% below February 2020 (seasonally adjusted), and the near-term outlook for higher production is bleak due to the shortage of semiconductors.

The “glass half full” view of the situation is that extraordinarily tight inventories of cars, trucks, and SUVs could keep automotive production humming for many months beyond the period of very strong retail sales.

More Fleet Management

Enhance Fleet Performance with High-Efficiency Auxiliary Power Units

Drive sustainable cost savings while increasing driver comfort during short- and long-haul logistics operations.

Read More →

Is Your Parts Procurement Process Reactive or Proactive?

Ready to revamp your parts procurement process? Learn how now with “Strategic Parts Purchasing: A Process Checklist”

Read More →

What Trucking Events are Happening in 2026?

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

Truckload Rates Keep Rising as Tight Capacity Fuels Freight Market Recovery

Spot and contract rates continued climbing in May and June, not because freight demand is surging, but because fewer trucks and drivers are available.

Read More →

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →