Fitch: Weak Demand in '08 Pressures Freight Transportation

The past year proved challenging for the freight transportation industry in the United States, and 2008 will likely remain difficult, at least through the first half, according to Fitch Ratings. Fitch is a global rating agency providin

The past year proved challenging for the freight transportation industry in the United States, and 2008 will likely remain difficult, at least through the first half, according to Fitch Ratings. Fitch is a global rating agency providing

credit markets with independent credit opinions.

Following three years of strong demand growth that led to higher volumes and pricing power for both the railroad and trucking industries, demand began to wane in the latter half of 2006 and weakened further over the course of 2007. The hoped-for up tick in demand that many expected in the second half of this year never materialized, and demand in the peak season has been about as weak as the lackluster period last year.

The effect of weak demand has not been seen equally across the railroad and trucking industries as excess truck capacity in both the truckload and less-than-truckload sectors has forced truckers to choose between price and volume.

Among railroads, volumes have been weak in those market sectors influenced by the housing and automotive industries, but strong demand for less-cyclical commodities like coal and grain has helped to limit declines in overall volume.

Looking toward 2008, continued weakness in housing, potential tightness in the credit markets and high energy prices are expected to restrain economic growth in the United States.

Fitch is currently expecting real gross domestic product (GDP) growth of 1.7 percent in 2008, down slightly from a forecast of 1.8 percent for full-year 2007 and well below the long-term average projection of 3 percent. This slow growth rate will continue to weigh on the financial performance of both industries, blunting demand growth and restraining pricing. Railroads are expected to perform better overall than their trucking peers as relatively tighter rail capacity and less exposure to cyclical shipments will continue to support pricing.

From a credit perspective, there is generally a greater risk of negative outlook revisions or downgrades in the trucking industry, although railroad credit profiles could also weaken if issuers in that industry take a more-aggressive stance toward returning cash to shareholders through debt-financed stock buybacks.

Demand for the goods shipped on U.S. highways and rails declined in 2007 as compared with very strong demand levels in 2005 and the first half of 2006. This decline in demand over the past year has been largely due to the slowing U.S. economy, as weakness in the residential construction and auto manufacturing industries, falling home prices, increasing energy costs and, more recently, tightness in the credit markets have put increasing pressure on consumers.

The resultant weakness in retail sales has led to reduced industrial production, which has, in turn, driven declines in demand for both raw materials and finished goods. Railroads have fared better than trucks in this slowing demand environment, in part due to the higher percentage of non-cyclical commodities shipped by rail. Recently, the weakening of the U.S. dollar has also spurred an increase in exported commodities, which also has helped to support rail volumes. On the other hand, the trucking industry, which is more closely tied to retail and manufacturing demand, has experienced a more significant decline in volume as the economy has cooled.

The trucking industry's problems have not only been the result of waning demand, however. The industry also suffered in 2007 from a rapid increase in capacity that was partly the result of the U.S. Environmental Protection Agency's (EPA's) change in emission regulations for heavy-duty truck engines that took effect in January.

Many truckers, concerned about the potential costs associated with new technology, opted to 'pre-buy' tractors in 2006, purchasing far more tractors last year than they would have in a 'normal' year. This growth in tractors led to an increase in trucking capacity just as demand was cooling. Through 2007, this unfavorable combination of increased capacity and reduced demand has had the predictable result on industry pricing, forcing truckers to reduce unit rates or see volumes decline materially.

Although the GDP growth rate is expected to continue slowing in 2007, the rate of deceleration is expected to moderate, which could help to slow the rate of decline in demand for economically-sensitive goods. As truck volumes are more closely tied to these goods than rail volumes, this could be more important for truckers, who could see the rate of decline in demand moderate in 2008.

Challenges will remain, however, as even moderating demand will still be relatively weak. Pricing in the truck sector will remain competitive, although the steep decline in truck deliveries in 2007 combined with normal equipment retirements should help to improve the capacity situation somewhat. Fitch also expects capital spending in the trucking industry to decline in 2008, perhaps significantly, from 2007 levels, which should further help to alleviate some of the industry's overcapacity.

Just as the railroads are expected to generally perform better than the truckers in an economic environment characterized by slow growth, they are also better positioned to weather a potential recession. Although Fitch is not currently expecting the U.S. economy to fall into recession in 2008, the risk of a near-term recession has increased over the past several months. The commodity nature of many of the products shipped by rail makes the industry more recession-resistant than the trucking industry.

By contrast, shipments carried by truck tend to be more economically sensitive, with trucking volumes more closely tied to shipments of materials and components used in manufacturing, as well as the shipment of retail items and other finished goods. In addition, with railroads entering a potential recessionary period financially stronger than most truckers, with robust liquidity and free cash flow margins, the rail industry is better positioned to withstand a prolonged recession-driven downturn in demand than the relatively weaker trucking industry.

More Fleet Management

What Trucking Events are Happening in 2026?

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

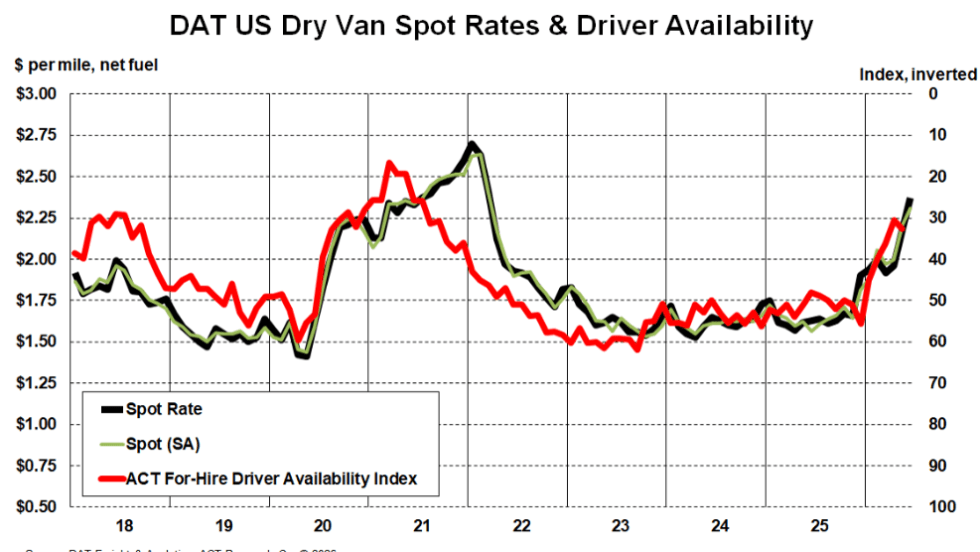

Truckload Rates Keep Rising as Tight Capacity Fuels Freight Market Recovery

Spot and contract rates continued climbing in May and June, not because freight demand is surging, but because fewer trucks and drivers are available.

Read More →

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

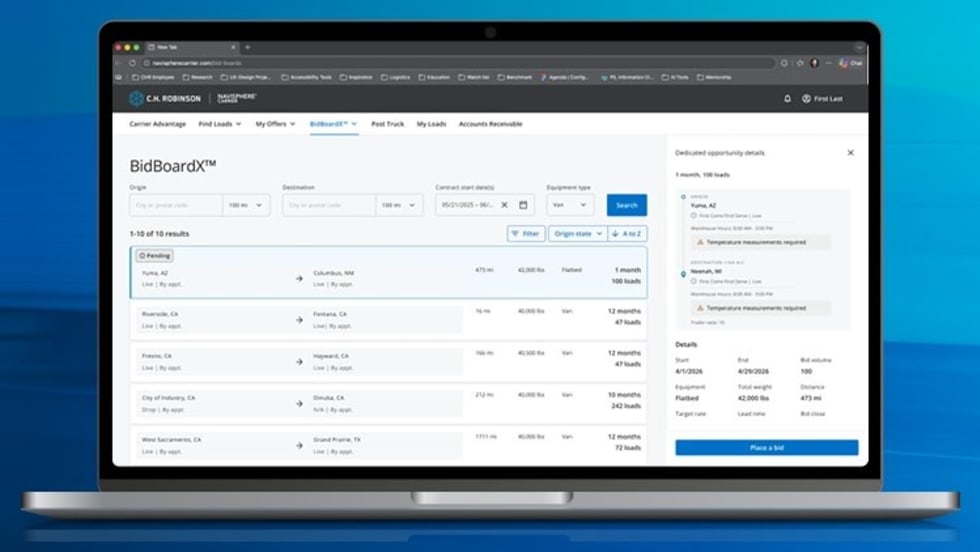

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →

Import Cargo Volume to See Year-Over-Year Gain Again in June, Then Remain Below 2025 Levels Into Fall

After July, the report predicts a weakening in import volume as consumer uncertainty remains high and the impact of increasing inflation takes its toll.

Read More →

AUCTION OF EQUITY INTEREST IN HEAVY HAUL TRUCKING COMPANY!!

Mark your calendar: June 30, 2026 (10:00 a.m. PDT). A 37.5% ownership interest in MagnaTrans, LLC, a California limited liability company doing business as Magna Transportation Group, will be sold in an in-person and online auction to the highest bidder or bidders under Article 9 of the Uniform Commercial Code. The Rancho Cucamonga-based heavy haul and over-dimensional trucking company operates across California, Oregon, and Arizona.

Read More →