Read more from Jeff Kauffman's Behind the Numbers column.

What Q2 Earnings Tells Trucking About Market Trends

Transport companies delivered largely better-than expected second-quarter earnings, but we are starting to see weaker trends developing in consumer-facing industries.

September 27, 2022

Graphic: HDT

3 min to read

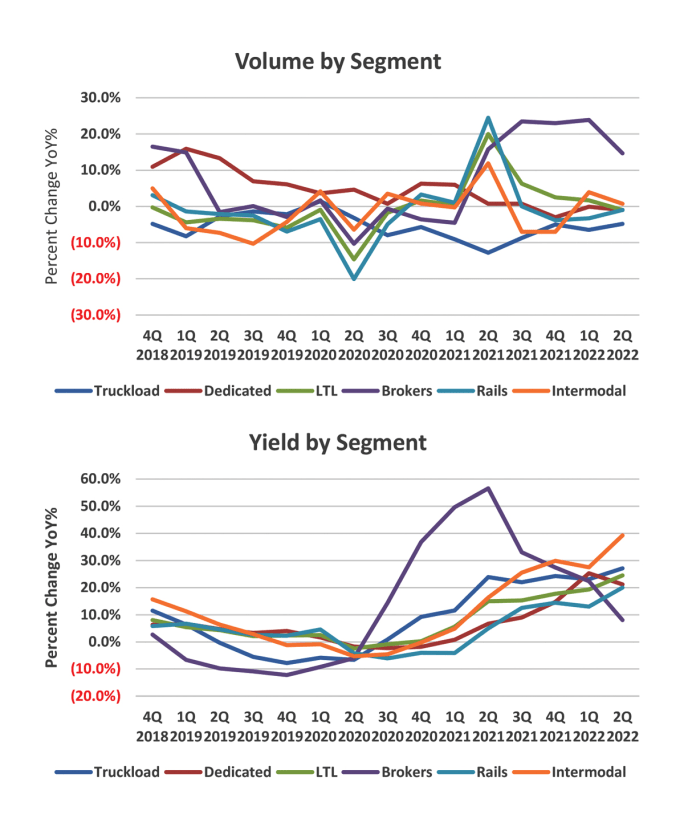

In the second quarter of 2022, less-than-truckload improved 4.7 percentage points in year-over-year margins, followed by intermodal with a 3.9 percentage point improvement. Railroads were the underperforming segment, down 2.6 percentage points.

Source: Company Reports, Tahoe Ventures LLC

Transport companies delivered largely better-than expected second-quarter earnings, but we are starting to see weaker trends developing in consumer-facing industries.

Overall, earnings-per-share outlooks remained flat for 2022, a deceleration from the 3% rate in the first quarter. In less-than-truckload and dedicated, yields (pricing + fuel surcharge + mix) largely came in ahead of expectations and volumes were stronger, but brokerage, intermodal and truckload showed decelerating growth.

Labor costs are rising, but at a slower rate, and purchased transportation costs are now declining. Customers are not yet pushing back hard on rate increases, and demand appears to be weaker in housing and large-ticket furnishings/DIY retailers. While retailers have struggled from stocking up on the wrong kind of inventory, the right inventory continues to be tight. Supply chain bottlenecks are easing, and ocean and air rates globally are moderating, but supply chain challenges are not yet over and rates still remain at elevated levels.

The big winners this quarter were less-than-truckload, with a 4.7 percentage point improvement in year-over-year margins, followed by intermodal with a 3.9 percentage point improvement.

The big underperformer this quarter was railroads, down 2.6 percentage points. Service problems caused rail carriers to scramble for extra people, equipment, and in some cases, revive closed rail yards.

Truckload and dedicated showed similar margin improvement but are headed in different directions. Dedicated margins improved 0.4 percentage points, much improved from declines of 2.5 points in the fourth quarter of 2021. Truckload operating margins improved by 0.3 percentage points, but that is down meaningfully from a 2.4-point improvement at the end of last year.

In the pure truckload segment, miles declined by 5% on flat fleet growth, but yields (including fuel) increased by about 27%, resulting in 20% revenue growth. Operating expenses were led by a 70% increase in fuel costs, resulting in margins being 0.3% better at 12%. Knight-Swift’s 17.4% operating margin edged out Heartland’s 17%.

More companies are breaking out dedicated truckload, although the data is not robust. The dedicated fleets saw 1% fewer miles on 4.9% fleet growth, and yields improved to about 21%, resulting in 27% revenue growth. Dedicated’s net fleet adds were among the largest we have seen in two years, as margins improved 0.4 percentage points to about 7.7%, still well below the 13% range in 2020.

The less-than-truckload space showed impressive margin improvement, despite a still-slow industrial marketplace. Tonnage and shipment growth were largely below expectations with a decline of 1% on more difficult comparisons, and weight/shipment was flat. Old Dominion Freight Line warned that July tonnage growth was negative, which bears watching. LTL yields continued to improve, up 24.5%, resulting in 23.3% revenue growth. The overall LTL margin hit a record high of 17.4%, up 4.7 points from a year ago. There were two notable firsts — Old Dominion broke a 70% operating ratio at 69.5%, and FedEx Freight broke 80% at 78.2%.

The brokerage and logistics group showed the largest revenue and volume deceleration but benefitted from margin expansion as spot rates fell more quickly than contract rates. Volumes dropped from 24% growth rates to 15% and yields fell from 22% to 8%, resulting in revenue growth of 26%. We believe this growth could trend toward negative in the second half of the year. Margins are expanding about 2.8 percentage points versus the prior year, but we expect this to moderate toward year-end as contracts are repriced.

This column first appeared in the September 2022 issue of Heavy Duty Trucking.

Subscribe to Our Newsletter

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →