Also of interest: How to Maximize Trailer Space

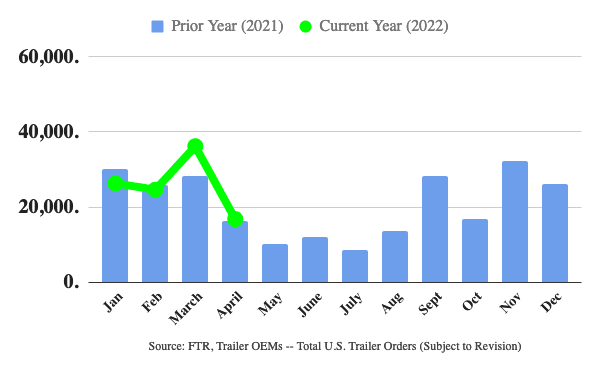

Trailer Orders Plummet in April Amidst Supply-Chain Concerns

The pent-up demand for trailers is estimated at over 100,000 units, with an average backlog-to-build ratio of just over eight months for the total industry.

May 13, 2022

“There is no reason for trailer OEMs to overbook, with increasing uncertainties regarding the supply chain,” said Don Ake, FTR vice president of commercial vehicles.

Source: FTR

2 min to read

Trailer orders in April were down substantially from March, although up slightly over a year ago, as lockdowns in China and the war in Ukraine prompted caution in the market.

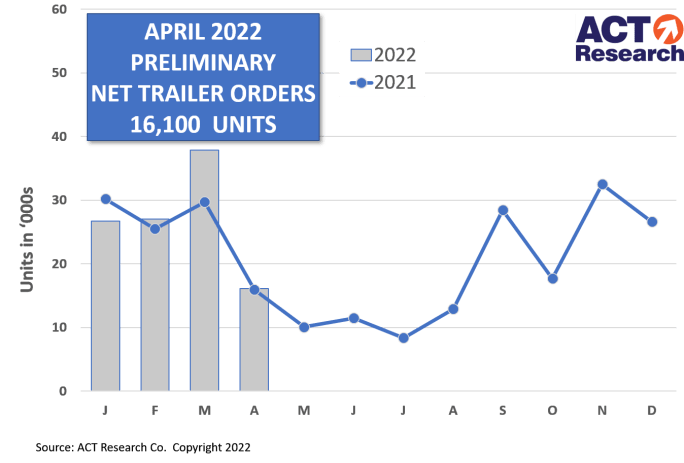

FTR reports preliminary trailer orders fell in April to 16,800 units, 53% below March order activity and up 4% year over year. Trailer orders for the past 12 months have totaled 252,000 units. ACT Research numbers put April numbers at 16,100 units, down almost 60% from the previous month and up slightly from the same month last year.

This followed a month when March trailer orders surged to their highest since December of 2020, representing most of the trailer-maker build slots for dry vans for the rest of the year.

While seasonal patterns typically see a drop in trailer orders in April, preliminary reports indicate that volumes fell more than might have been expected, according to Frank Maly, director of commercial vehicle research at ACT Research.

March trailer orders were significantly higher than a year ago, making the April drop from the previous month look even worse.

Source: ACT Research

“While some may think recent economic challenges could be a contributing factor to the sequential decline, it’s more likely that a reluctance to push the orderboard horizon into next year is responsible, as OEMs continue to closely control order acceptance,” Maly said.

“There is no reason for trailer OEMs to overbook, with increasing uncertainties regarding the supply chain,” said Don Ake, FTR vice president of commercial vehicles.

The situation in Shanghai, which has been locked down due to a COVID-19 outbreak, he explained is going to delay some components that are needed to make trailers, while the war in Europe is creating shortages of aluminum.

“These and other doubts have delayed OEMs from issuing quotes for 2023 requirements,” Ake said. “So, the low order volumes reflect OEMs filling in the months of the 2022 production schedule they feel more confident about.”

ACT’s Maly said their discussions indicate that active negotiations between OEMs and fleets continue, as fleets prepare to make commitments for 2023 production, when that opportunity becomes available.

The pent-up demand for trailers is estimated at over 100,000 units, according to FTR. ACT said the lower order levels for April will still result in an average backlog-to-build ratio of just over eight months for the total industry.

Pandemic-triggered supply chain difficulties the world has been experiencing are now expected to extend into 2023. “OEMs will then have to build at high rates for an extended time to catch up to demand,” Ake said. “The short-term prospects are subdued, but the long-term outlook remains bright.”

More Equipment

EPA Proposal Could Ease 2027 Truck Costs and Buying Uncertainty

The proposal doesn't change the tougher NOx standard, but it would revise key implementation requirements that manufacturers say have driven up costs and complicated fleet purchasing decisions.

Read More →

Cummins, Paccar Ease DEF Derates After EPA Guidance

Updated diesel engine software gives truck operators more time to address emissions-system issues while staying compliant with EPA emissions standards.

Read More →

America at 250: How the Truck Helped Connect a Continent

America was founded on revolutionary ideas, but it was built by movement. For 250 years, the nation has depended on ever-better ways to move people, products, and prosperity across a vast continent. No machine has carried that mission further — or more faithfully — than the truck.

Read More →

Mack Unveils America 250 Tribute Truck to Celebrate Nation's Semiquincentennial

Just in time for the Fourth of July! Mack unveils a brand-new patriotic, limited-edition, red, white, and blue truck wrap.

Read More →

Sponsored•July 1, 2026

Enhance Fleet Performance with High-Efficiency Auxiliary Power Units

Drive sustainable cost savings while increasing driver comfort during short- and long-haul logistics operations.

Read More →

Rush Expands Gulf Coast Peterbilt Network With Louisiana Acquisition

The expanded Rush network gives fleets additional sales, service, leasing and collision repair support across Louisiana's major trucking markets.

Read More →

Photos: Shell SuperRigs Light Up Bristol Tennessee

Kenny Ziglar II of Rawlins, Wyo., captured Best of Show honors for the second consecutive year with his 2007 Peterbilt 379, nicknamed “Scrapin By,” at the 44th Annual Shell Rotella SuperRigs competition held June 25-27 at Bristol Motor Speedway in Bristol, Tenn.

Read More →

Waabi, Volvo Claim Breakthrough in Scaling Autonomous Trucking

Waabi says its AI-powered virtual driver successfully transferred to Volvo Autonomous Solutions' Volvo VNL Autonomous platform without retraining or additional data, a milestone the companies say could dramatically accelerate commercialization of autonomous trucks.

Read More →

Why the Mack Pioneer Signals a New Era in Class 8 Truck Design

After a public-road drive through eastern Pennsylvania, one thing became clear: Mack's new Pioneer isn't simply packed with technology -- it's been engineered around the driver in ways that could redefine long-haul trucking.

Read More →

Mack Defense Secures $47 Million to Continue Military Dump Truck Production

President Trump visited Mack Defense’s Macungie, Pennsylvania, facility on June 23 to tout a $47 million Heavy Dump Truck order.

Read More →