Does Trailer Order Surge Mean Sold-Out Build Capacity?

A major jump in trailer orders during March will extend OEM commitments through most of the rest of the year, unless manufacturing capacity increases.

March trailer orders of 36,200 units are up 29% compared to a year ago.

Credit: FTR

March trailer orders surged to their highest since December of 2020 – but for dry van orders, that may represent most of the trailer-maker build slots for the rest of the year.

The major jump in trailer orders during March will extend OEM commitments through most of the remainder of the year at current production levels, according to ACT Research.

“Is it a complete sell-out? Not entirely, but it’s getting quite close for many dry van and reefer OEMs,” Frank Maly. ACT’s director of CV transportation analysis and research, told HDT.

“The March surge is a short-term spike, but upcoming order volume will be driven by OEMs’ willingness to accept orders and their willingness to begin to open 2023 order boards,” Maly said, with concerns about setting pricing the major challenge.

“For example, one OEM informed me that their extremely low order volume for the month was the result of them being sold out for the year and they were unwilling to open up 2023 order boards at this time,” Maly said. “Others, accepting higher order volumes, were in the process of filling their remaining production capacity for 2022.”

For vocational trailers, there is more availability of build slots, even though their backlogs generally extend farther than normal, Maly said.

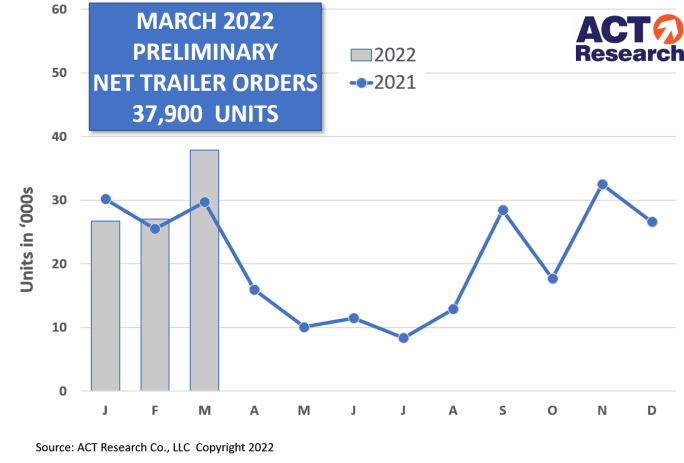

According to ACT and FTR, whose preliminary numbers vary slightly, March trailer orders were 36,200-37,900 units, up 40-41% month over month and 28-29% year over year. Trailer orders for the past 12 months have totaled 252,000 units, according to FTR.

Preliminary U.S. trailer orders of 37,900 in March surged 40% from February.

Credit: ACT Research

FTR said most of the major trailer OEMs showed significant increases versus the past six months, and March’s strong order total is expected to raise backlogs over the 200,000-unit mark for the first time since May 2021.

ACT said final figures for the month will likely reveal total industry backlog now stretching into December at current production rates, heavily influenced by dry van and reefer commitments that basically fill their year.

Trailer Manufacturing Capacity

Both FTR and ACT said the numbers indicate that trailer makers could be optimistic that they will be able to increase their build rates later this year.

“This is great news for the trailer market,” said Don Ake, FTR vice president of commercial vehicles. “Most of the big OEMs were stuck in a holding pattern on orders since the supply chain tightened. The fact they have the confidence now to enter more orders may indicate that supplier deliveries are showing improvement, and labor shortages are abating.”

ACT Research expects that production rates will improve as we move through the year, “so that will likely open some additional, but limited, availability later in 2022,” Maly said. “The wildcards there center around both supply chain support and staffing. We heard last month that staffing seemed to be becoming less of a challenge. This month, comments indicated that the supply chain was beginning to smooth out as well. Obviously, both are positive trends, but likely helping to ease the challenges OEMs have had regarding production planning rather than generating a solid path to significant increases in production levels.”

“Because OEMs had their output limited by the supply chain, we estimate that pent-up demand for trailers could be as high as 100,000 units,” said FTR’s Ake. “It will take an extended time for OEMs to catch up with fleet requirements once the supply chain opens up.”

More Equipment

Historic, Vintage, and Antique Trucks at the 2026 ATHS Convention

More than 500 trucks were on display, indoors and out, at the 2026 American Historical Society annual convention in Springfield, Missouri.

Read More →

DTNA Software Update Gives Truckers More Time Before DEF Derates Take Effect

The changes reflect EPA guidance aimed at reducing downtime caused by emissions-system faults while maintaining compliance requirements.

Read More →

Great American Trucks: The International MaxxPro MRAP

Built from an International WorkStar chassis and powered by a MaxxForce diesel, the MaxxPro MRAP became one of the most important military trucks of the Iraq War era.

Read More →

New Mack Granite Cab Puts Driver Comfort Front and Center

Mack’s next-generation vocational truck features a roomier cab, premium seating, advanced steering technology, and a driver-focused interior designed with direct input from professional operators.

Read More →

Mack Unveils Fan-Selected Patriotic NASCAR Pioneer Wraps

Racing fans picked the patriotic design now featured on three Mack Pioneer trucks hauling NASCAR equipment across the country during the 2026 season.

Read More →

Michelin Expands X Line Grip D Tire Line

Michelin is expanding its X Line Grip D drive tire lineup with a new pre-mold retread and additional sizes, building on what the company says is strong fleet adoption of the tire's traction, mileage, and fuel-efficiency benefits.

Read More →

Engine Technology Forum Launches SCR, DEF Resource Center Amid Emissions Debate

The Engine Technology Forum’s new online hub aims to provide fleets, policymakers, and equipment owners with fact-based information about selective catalytic reduction technology, diesel exhaust fluid and emissions compliance.

Read More →

Prime Inc. to Open $7.9M Flagship Used-Truck Dealership

A new driver-focused facility to sell Prime Inc's used trucks and trailers will be the first purpose-built location in the company's history.

Read More →

Lessons Learned About Alternative Fuels: Start Small, Stay Flexible

Practical advice on adopting alternative fuels and ZEVs from HDT's 2026 Top Green Fleets, from renewable diesel and natural gas to electric trucks.

Read More →

Kenworth Names Peter Ahrens General Manager

Leadership changes at Kenworth take effect July 1 as the OEM promotes two longtime Paccar executives to key management roles.

Read More →