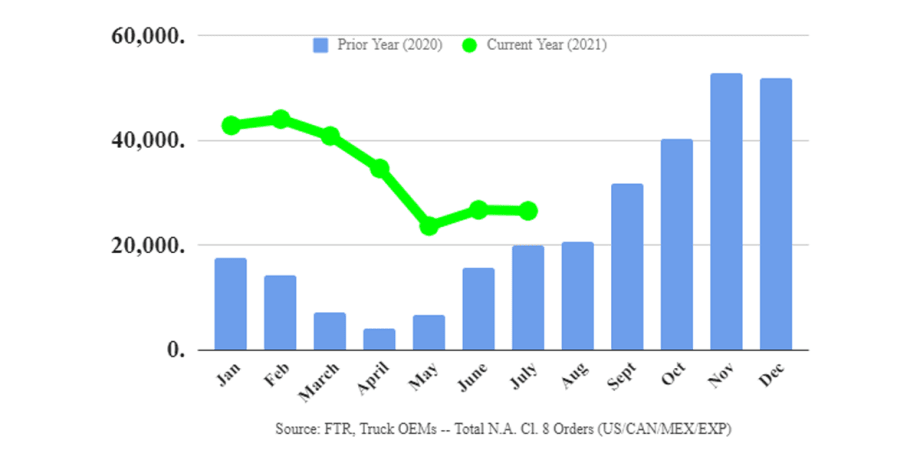

Class 8 Orders Remain Steady in July

North American Class 8 orders in July were between 25,800 to 26,500 units, virtually unchanged compared to June’s orders.

The July Class 8 order total is essentially equal with June, as the industry is in a holding pattern at the bottom of this order cycle.

Graph: FTR

North American Class 8 orders for July were between 25,800 to 26,500 units, down about 1% month over month and virtually unchanged compared to June’s orders.

Orders improved 25% year over year, FTR reported, with Class 8 orders now totaling 394,000 units for the previous 12 months.

The July order total is essentially equal with June, as the industry is in a holding pattern at the bottom of this order cycle. Ordering for 2022 has commenced at most OEMs but remains delayed some due to cost uncertainty and the possibility of enduring supply chain bottlenecks, FTR officials said in a press release.

“July ordering was similar to June in that OEMs took a limited number of orders for delivery in 2022,” said Don Ake, vice president of commercial vehicles for FTR. “Fleets need a significant number of new trucks right now and they perceive this need will continue throughout next year. However, OEMs are having difficulty establishing reasonable 2022 pricing, with commodity and other costs elevated. It is uncertain if current higher production costs are transitory or will persist into 2022.”

Also complicating the situation is that shortages of semiconductors have limited Class 8 production, Ake said.

“It is estimated that supply of trucks is falling approximately 25% behind market demand,” he said. “We are running out of time for OEMs to catch up. Most of the unproduced orders will roll into the first quarter of 2022. If those months are already booked solid, it creates even more headaches for the industry. Things won’t approach any degree of normalcy for months. Until semiconductors begin flowing into the OEMs in sufficient qualities, we will be playing catch up.”

ACT President and Senior Analyst Kenny Vieth said: “Underlying drivers of commercial vehicle demand are considerably hotter than they were three summers back, with 6-plus percent GDP growth, capacity constraints across multiple shipping modes, at/near-record trucking freight rates, surging carrier profits and record used equipment valuations providing deep support for Class 8 demand.”

More Equipment

Great American Trucks: The International MaxxPro MRAP

Built from an International WorkStar chassis and powered by a MaxxForce diesel, the MaxxPro MRAP became one of the most important military trucks of the Iraq War era.

Read More →

New Mack Granite Cab Puts Driver Comfort Front and Center

Mack’s next-generation vocational truck features a roomier cab, premium seating, advanced steering technology, and a driver-focused interior designed with direct input from professional operators.

Read More →

Mack Unveils Fan-Selected Patriotic NASCAR Pioneer Wraps

Racing fans picked the patriotic design now featured on three Mack Pioneer trucks hauling NASCAR equipment across the country during the 2026 season.

Read More →

Michelin Expands X Line Grip D Tire Line

Michelin is expanding its X Line Grip D drive tire lineup with a new pre-mold retread and additional sizes, building on what the company says is strong fleet adoption of the tire's traction, mileage, and fuel-efficiency benefits.

Read More →

Engine Technology Forum Launches SCR, DEF Resource Center Amid Emissions Debate

The Engine Technology Forum’s new online hub aims to provide fleets, policymakers, and equipment owners with fact-based information about selective catalytic reduction technology, diesel exhaust fluid and emissions compliance.

Read More →

Prime Inc. to Open $7.9M Flagship Used-Truck Dealership

A new driver-focused facility to sell Prime Inc's used trucks and trailers will be the first purpose-built location in the company's history.

Read More →

Lessons Learned About Alternative Fuels: Start Small, Stay Flexible

Practical advice on adopting alternative fuels and ZEVs from HDT's 2026 Top Green Fleets, from renewable diesel and natural gas to electric trucks.

Read More →

Kenworth Names Peter Ahrens General Manager

Leadership changes at Kenworth take effect July 1 as the OEM promotes two longtime Paccar executives to key management roles.

Read More →

Hino Adds Electric Class 6/7 Truck

Hino says the Le Series is an important step in the company's efforts to reduce environmental impact and support its customers’ sustainability goals.

Read More →

ACT Expo 2026: Highlights in Photos

The 2026 Advanced Clean Transportation Expo featured a broad range of commercial vehicle technologies, from EVs to autonomous trucks to the latest diesel and alternative-fuel engines.

Read More →