How Did Wild Third-Quarter Swings Affect Fleet Earnings?

How did publicly traded trucking fleets perform financially as the roller-coaster year of 2020 headed back uphill in the third quarter?

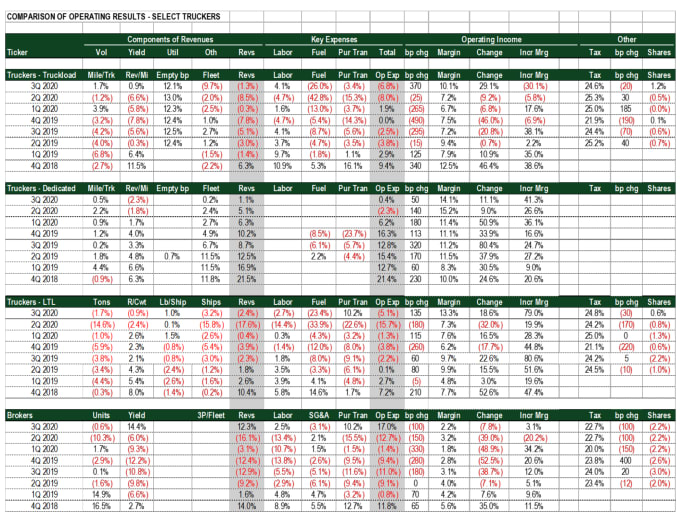

On average, less-than-truckload companies in the third quarter showed impressive margin improvement.

Photo: Deborah Lockridge

The third quarter of 2020 marked a turn in fundamentals for many freight companies. After a second quarter saw real gross domestic product plunge 31.4%, the 33.1% increase in the third quarter resulted in a year-over-year GDP figure closer to 2.6%.

The quarter saw an aggressively rebounding freight volume environment, likely the result of carrier capacity reductions, inventory restocking by retailers, and a surge in necessity shipping of food, beverage and healthcare-related items. Business inventory levels appeared to be coming down at a 6% rate as of the end of the third quarter, but retail inventories were declining at a rate closer to 12%.

Despite some of the most dramatic short-term third-quarter swings in freight demand, financial results for most freight and logistics companies were better than expected. Even with lower revenue, the publicly traded companies we track saw better operating margins, largely the result of lower fuel, labor and purchased transportation costs, and a sharp rebound in volumes caused in part by an inventory build among retailers.

Jeff Kauffman

Photo: Jeff Kauffman

In the pure truckload segment, we saw profits consistently beating expectations for the second consecutive quarter. Average operating profit margins for the companies we’ve tracked in the accompanying table jumped to 10.1%, the highest we have seen since 2018. There was an average 1.3% revenue decline (the average fleet dropped by 9.7%, but drove more miles per truck, and was paid 0.9% more in terms of average revenue per mile). But revenue per mile improved, fleet growth slowed, truck utilization improved meaningfully from last quarter, and empty mile ratios improved by 0.9% to 12.1% — better than we would have expected, given the wild swings in the economy.

In dedicated truckload, although the data is not robust, there are some interesting observations. Median revenue growth was the strongest among trucking segments, at 1.1%, but it continued to slow while other areas improved. Average operating profit margin of 14.1% was only a 0.5% improvement. Fleet growth slowed to 0.2%, so there is still a shift in capacity occurring, but the trend has slowed.

Less-than-truckload showed impressive margin improvement and a meaningful bounce-back in revenues, despite a still-slow industrial marketplace. Average operating margins improved to 13.3%, the result of some dramatic cost-cutting, lower fuel prices, and nearly 13 percentage points improvement in tonnage over the second quarter. Top-line revenues were down an average of 2.4%, an improvement from being down 17.6% in the second quarter. We saw a decline in shipments (3.2%), tonnage (1.7%), and yields (0.9%). However, costs fell more, with labor costs down 2.7% and fuel costs 23.4% lower. A leading indicator, weight per shipment, improved 100 basis points — a positive sign.

The operating environment for brokers was challenging, given the swings in spot rates and volumes. A 25% increase in trucking spot rates from the previous quarter resulted in a revenue increase of 12.3%, driven by shipment levels only 0.6% lower as shippers scrambled for capacity amongst 25%+ tender rejection rates, implying a 14.4% improvement in yields. To put the difficulty in managing this swing in perspective, revenues were down 16.1% last quarter. Despite the positive news on revenue and yield, spot rates drove the cost of purchased transportation up faster, leading to a 17% increase in operating expenses and a drop in operating margins to 2.2%. However, many brokers expect contractual rates to begin to improve relative to spot market rates in the coming quarters.

Looking ahead, near term, a surge in COVID-19 infections may lead to another round of slowdowns in commerce this winter. What is encouraging heading into the new year is that tighter capacity and rising volumes are driving spot market rates higher. We are hearing via anecdotes that this is leading to stronger contract rates. Another sign of this is the way truck and trailer orders have been racing upward in recent months.

More Fleet Management

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →

July Imports Poised to Set Container Record

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

Read More →

HDT Announces 2026 Truck Fleet Innovator Finalists

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Read More →

Van Spot Rates Top Contract Rates for First Time Since 2022

There’s more good economic news for the North American trucking industry according to the latest Truckload Volume Index report from DAT.

Read More →

Carrier Transicold Extends Refrigerated Trailer Life

Fleet Refresh enables refrigerated fleets to replace aging transport refrigeration units instead of entire trailers, while adding Lynx Fleet telematics and BluEdge service coverage.

Read More →