Truck Sales Drop: We've Seen The Worst of It

Freightliner’s 3,745 layoffs last week bring the total over the past few months to over 6,000 in North American heavy truck factories, including earlier layoffs by Volvo, Paccar and Navistar. More layoffs are likely this fall. Manufacturers

Freightliner’s 3,745 layoffs last week bring the total over the past few months to over 6,000 in North American heavy truck factories, including earlier layoffs by Volvo, Paccar and Navistar. More layoffs are likely this fall.

Manufacturers are reacting to dealer resistance to add to their already bloated inventory of Class 6-8 trucks, up more than 20,000 units so far this year. Last year’s production levels were boosted above sales to build up inventory in a rapidly expanding market. Then manufacturers were too slow to reduce production when sales began to decline. Retail sales are only 1% lower so far this year compared to the same period last year, but sales fell to 30,329 in July, seasonally adjusted, compared to a peak of 41,487 last November. Sales trends for classes 3-5 are very similar.

Sales have weakened because the price for a new truck, net of trade in, has increased by a third. Last year a $100,000 truck cost $50,000 with a late model trade in. Today, the same truck costs $67,000 because the supply surplus has cut the trade-in value to $33,000. Dealers are losing sales to fleets and owner-operators who have to wait for used equipment prices to return to normal before they can afford to trade.

What’s happening now is entirely consistent with the usual changes in sales trends over the very volatile truck equipment business cycle. Sales trends during 1998-2001 are nearly identical to those in 1993-1996. To refresh your memory: Seasonally adjusted monthly sales hit a low of about 19,000 in early 1993, rose to 30,000 in early 1995 and then fell to 22,000 in late 1996. The driver shortage and the sharp rise in diesel fuel prices are both part of the usual baggage that comes at the peak of a business cycle. They have happened before at the same point in the cycle. And they will ebb during the slowdown phase of the business cycle.

So what’s next for truck sales? That depends on how the current business cycle plays out. The early evidence is that the current phase of slowing economic growth will be exceptionally mild. So far only the housing market has declined, although the motor vehicle market is no longer growing. The better performance of the economy is because the electronics industry is growing at about a 30% annual rate due to technological innovation and exports. The rest of the economy has slowed to below average growth.

With the business cycle outlook for an exceptionally mild slowdown, the outlook for truck sales in 2000 and 2001 is for much higher sales than would normally occur at the bottom of a business cycle. Monthly sales will average 33,000-34,000 through the end of next year, although sales will be mostly below that level for the next six months until excess inventory has been absorbed.

Why have heavy truck production and sales fallen so sharply this summer? Is the falloff due to weakening in the economy, to the usual business cycle in the truck market or to other problems in the truck market such as the driver shortage, the plunge in used truck prices or the sharp increase in diesel prices?

Freightliners’ announcement this week of 3,745 layoffs in North American facilities brings the total job reduction to over 6,000, including earlier announcements by Navistar, Paccac and Volvo.

US retail sales of class 6-8 trucks fell, seasonally adjusted, to 30,329 in July, the lowest sales total since August, 1998. Monthly sales averaged 37,808 in the last half of 1999 and 36,239 in the first half of this year. Medium duty, class 3-5, sales have fallen similarly.

Slower economic growth has contributed to this problem but it is mostly due to the slowness of truck manufacturers to keep production in line with the sales outlook. The driver shortage and the higher diesel prices have also made small contribution to the problem.

Beginning in May, the pace of economic growth has dropped lower. Employment gains have been very small compared to the previous few years after the hiring of temporary Census workers is removed. Factory production growth has slowed to only a 4% annual rate and the growth of consumer spending has been halved. But the economy is still growing at a 3-4% pace.

Year to date, manufacturers have added more than 20,000 trucks to dealer inventories. June’s inventory addition was 1,159 trucks. Production cuts since then probably means that sales now exceed production. It will take at least six months to absorb excess inventory at current sales and production levels.

Dealers lost several thousand sales because the supply surplus has depressed the trade in value of used trucks.

More Fleet Management

Is Your Parts Procurement Process Reactive or Proactive?

Ready to revamp your parts procurement process? Learn how now with “Strategic Parts Purchasing: A Process Checklist”

Read More →

What Trucking Events are Happening in 2026?

Looking for trucking-related conventions, expos, and other events? Heavy Duty Trucking has developed this list of national and larger regional trucking shows and events.

Read More →

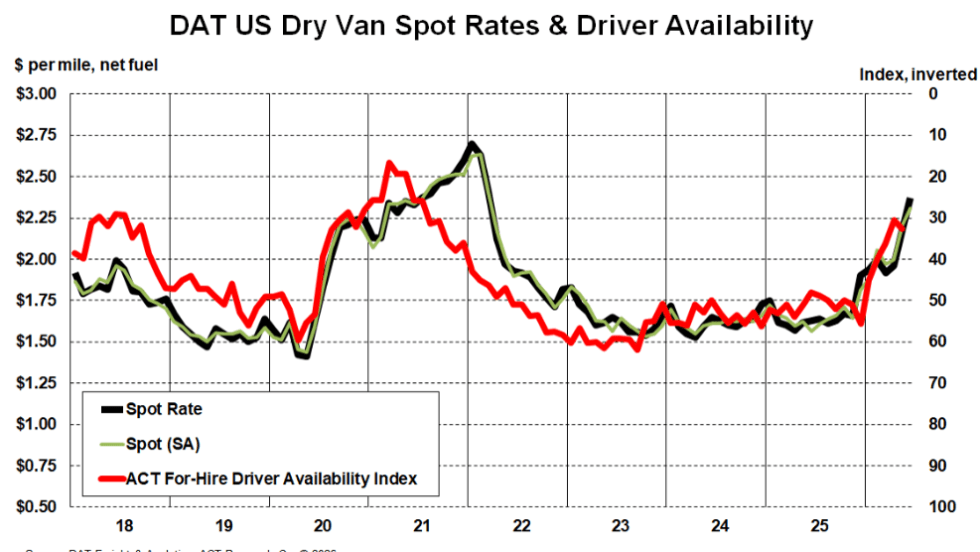

Truckload Rates Keep Rising as Tight Capacity Fuels Freight Market Recovery

Spot and contract rates continued climbing in May and June, not because freight demand is surging, but because fewer trucks and drivers are available.

Read More →

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

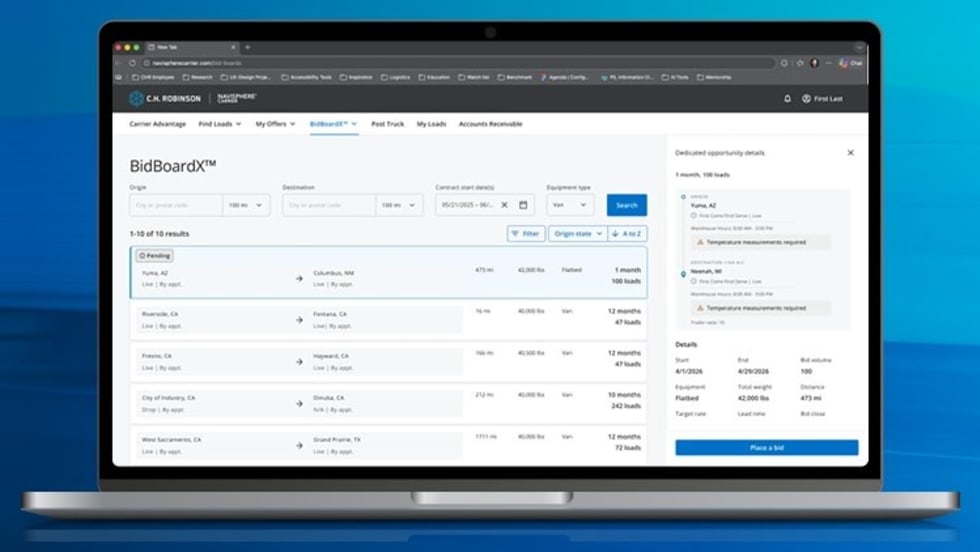

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →

Import Cargo Volume to See Year-Over-Year Gain Again in June, Then Remain Below 2025 Levels Into Fall

After July, the report predicts a weakening in import volume as consumer uncertainty remains high and the impact of increasing inflation takes its toll.

Read More →