Related:Economic Growth Ahead at Trend Level, Says Economist at Aftermarket Event

What Will Earnings Look Like for Fleets This Year?

With our 2019 economics and truck volume forecast in place, where should that take us in terms of earnings, and where are we in the course of the earnings cycle for truckers? Commentary from the February issue of Heavy Duty Trucking magazine.

February 1, 2019

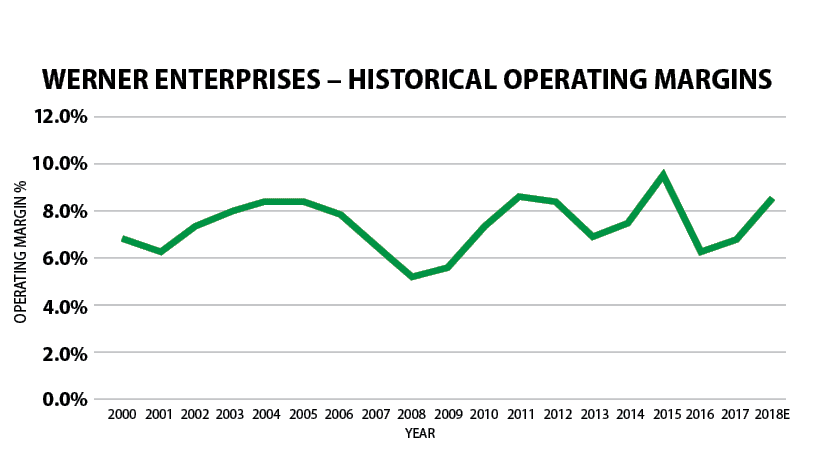

Since 2000, Werner’s operating margins have stayed in a consistent 6% to 9% range, with the majority of a cycle in the 6.5%-8.5% range.

Source: Company reports, Tahoe Ventures estimates

3 min to read

With our 2019 economics and truck volume forecast in place, where should that take us in terms of earnings, and where are we in the course of the earnings cycle for truckers?

Recent data has shown some slowing of economic growth. The Institute for Supply Management’s Purchasing Managers’ Index reported in January dropped to 54.1 from 59.3. Consumer confidence has slowed from a reading of 136.4 to 128.1. The three-month/10-year yield curve (which uses the difference between 10-year and three-month U.S. Treasury rates to calculate the probability of a recession) is currently around 35 basis points – almost flat. It’s normally about 200 basis points when healthy, and negative if the economy is at risk of recession.

Remember, in our forecast last month, we anticipated much of this “normalization” of growth expectations. While both the ISM and consumer confidence measures are sentiment indexes and do have predictive value, freight volumes and traffic continue to be strong. These lower readings could reflect concerns about stock market volatility and investor fears. As we noted last month, we expect the economy to slow to a more sustainable growth rate of around 2.5% GDP this year, where we spent much of the decade prior to 2016.

To explore the health of the trucking industry and what expectations are for 2019-2020, let’s look at where truck industry operator margins are right now, and where they might go. To simplify the analysis, let’s look at one large representative trucker – Werner Enterprises. Werner is a large truck fleet with about 7,800 trucks. It historically has grown organically, so acquisition-related costs don’t tend to cloud comparisons, and the company tends to be fairly consistent in terms of its margins over the course of a cycle.

Since 2000, Werner’s operating margins have stayed in a consistent 6% to 9% range, with the majority of a cycle in the 6.5%-8.5% range. Analyst expectations point toward an 8.6% operating profit margin for this year. (We look at margins all-in with fuel surcharges, versus the company’s reported results, which exclude fuel surcharges in calculating operating margins). Based on our expectations for a 3.5% truck freight growth level in 2019, and our expectations that the industry adds about 3% net capacity, we are looking for truck rates to be 2-3% higher by the end of 2019 than they were at the end of 2018. And they could even see an average for the year closer to 4%-5%, because we expect contract rates to begin the year in the 8-10% range. This would imply 6-8% revenue growth (the consensus of Wall Street analysts is 6.9%).

With all that in mind, and with declining fuel prices (the Energy Information Administration’s weekly on-highway diesel price index declined to $3.013/gallon for the week of Jan. 7), truck margins should be stronger for Werner in 2019. In fact, that is what Wall Street analysts are forecasting for Werner, according to Factset, which projects a 50 basis point (half a percentage point) improvement in Werner’s operating margin, implying an operating profit margin over 9% – the high end of the company’s historical range.

What does all this mean for fleet managers? While we expect some moderation in equipment orders because much of the order book for 2019 is filled, and uncertainty has increased regarding 2020 growth expectations, profit margins in the trucking industry should be healthy – near prior cycle peak levels. That means fleets should be a position to support continued buying of equipment, at least in the first part of the year. We look for truck OEMs to begin to enforce penalties for cancellations soon, which could thin out some of the order book as well.

Jeff Kauffman has been a recognized transportation authority for almost 30 years, most notably heading freight transportation research for Merrill Lynch. Currently he is managing director for Loop Capital Markets and also heads Tahoe Ventures, a transportation consulting company. He can be reached at jkauffman@truckinginfo.com.

Subscribe to Our Newsletter

More Fleet Management

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →

July Imports Poised to Set Container Record

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

Read More →