Related: Where Are We in the Business Cycle?

Commentary: Welcome to the Year of the Consumer

On what should we base a 2019 forecast? Start with what makes up almost 70% of our economy: the U.S. consumer.

December 21, 2018

On what should we base a 2019 forecast? Start with what makes up almost 70% of our economy: the U.S. consumer.

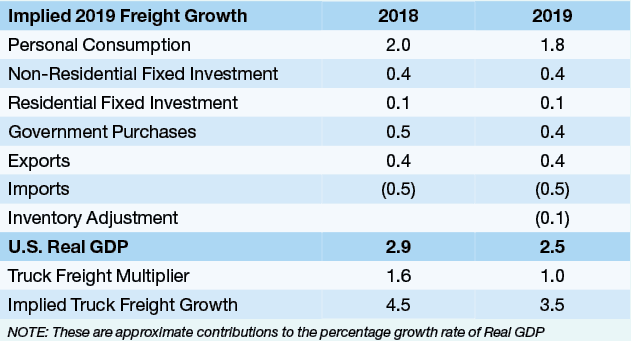

Source: Tahoe Ventures, LLC Estimates

3 min to read

As we exit 2018, there are many potential concerns: recent stock market volatility; rising interest rates; trade wars and higher raw material costs; risk to global currency exchange rates; a rapid drop in energy prices; slowing auto and housing demand; and global growth concerns.

So upon what should we base a 2019 forecast? We’ll start with what makes up almost 70% of our economy: the U.S. consumer. In our view, the U.S. consumer is sitting on solid ground. Unemployment is very low at about 3.7%, and wage growth is close to 3%, while inflation is only rising at about 2%, meaning disposable income is rising. Armed with a steady job and rising wages, the consumer should be spending, and in fact, that is what was happening in 2018, to the tune of 2.7% growth. We expect that to continue in 2019. In 2018 the consumer accounted for about 2 points of 2018 GDP growth, and we believe in 2019, that will continue, supporting 1.8 to 1.9 points of GDP growth.

Next, we look to the 18% of GDP that represents investment. Think of non-residential fixed investment as corporate capital expenditures – investments in tools, machinery, and commercial real estate. While that varies quite a bit over an economic cycle, with corporate profits on a high-single-digit growth path, we believe that component of GDP will remain relatively stable, contributing nearly 0.4 points to our GDP forecast. Rising interest rates will slow down the growth of housing investment, but continued employment and income will result in home purchasing, albeit for lower dollar amounts because of the higher cost of money. This only contributes 0.1 points to our forecast. So we are at 2.3-2.4% Real GDP growth so far.

Next on the list: government purchases. You can think of this as money spent on running our country, on our military, or on special government programs (excluding transfer payments such as Social Security). Military spending seems to be on the way up in 2019. In our view, there is the possibility of an infrastructure spending package, but we’ll leave that out for now. So we look for a slight increase from 1.7% growth to 2.5% growth. This will add between 0.4-0.5 points to our GDP forecast in 2019.

The last of the key figures is net exports, which is the sum of imports (negative to GDP growth) and exports (positive to GDP growth). Despite negative headlines regarding our potential trade war with China, it is the trade with Canada and Mexico that drives our economic engines, and the outlook for trade with our neighbors is steady. We have recently become a net exporter of energy, and while manufacturing industries may be hurt by the rise in raw material prices, and farm exports will be impacted by the U.S. dollar, we look for net exports to detract about 0.1-0.2 points from our GDP forecast.

So, adding all of this up, and taking a modest 0.1-0.2 points off for potential inventory adjustment for product pre-shipped ahead of potential tariffs, we get a real GDP forecast of 2.4%-2.6%. We’ll split it down the middle and call it 2.5%.

How do we convert this into a freight forecast? On average, total freight movements mirror Real GDP, with rail and ocean freight growing at slightly lower rates, and truck freight at a 100- to 150-basis-point premium. Using a more conservative 100 basis points, we believe truck freight demand will slow from 4.5% in 2018 to a strong, but slightly lower, 3.5% in 2019 – still strong enough to warrant continued equipment investment.

Jeff Kauffman has been a recognized transportation authority for almost 30 years, most notably heading freight transportation research for Merrill Lynch. Currently he is managing director for Loop Capital Markets and also heads Tahoe Ventures, a transportation consulting company. He can be reached at jkauffman@truckinginfo.com.

Subscribe to Our Newsletter

More Fleet Management

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →

July Imports Poised to Set Container Record

The National Retail Federation projects July container imports will surpass the pandemic-era record as shippers frontload freight ahead of expected August tariff increases.

Read More →

HDT Announces 2026 Truck Fleet Innovator Finalists

From AI and fleet electrification to safety, operations, and leadership, these HDT Truck Fleet Innovator finalists are changing how trucking gets done.

Read More →

Van Spot Rates Top Contract Rates for First Time Since 2022

There’s more good economic news for the North American trucking industry according to the latest Truckload Volume Index report from DAT.

Read More →

Carrier Transicold Extends Refrigerated Trailer Life

Fleet Refresh enables refrigerated fleets to replace aging transport refrigeration units instead of entire trailers, while adding Lynx Fleet telematics and BluEdge service coverage.

Read More →