McKinsey at CES: 2026 Begins with More Economic Pain Up Front

Don’t expect much good economic news for heavy duty trucking in the early part of the new year, according to McKinsey analyst Moritz Rittsieg. But there are signs that things could improve in the second half of 2026.

Moritz Rittstieg (left) and Tobias Schneiderbauer speak to the trucking media at CES 2026.

Photo: Jack Roberts

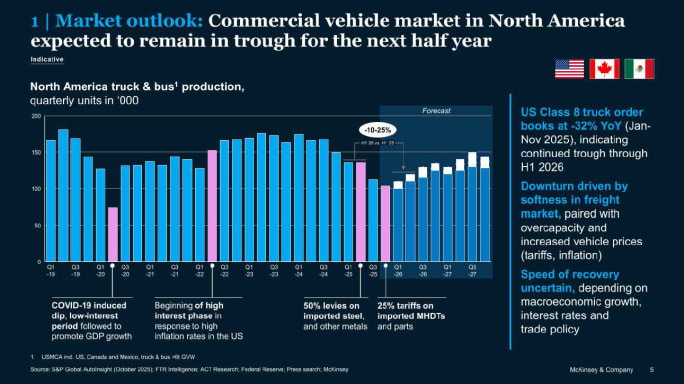

McKinsey & Company partner Moritz Rittstieg's view of the U.S. truck market this year is blunt: 2025 was “extremely challenging,” he said. And he is projecting 2026 to start out “equally challenging.”

However, Rittsteig and fellow McKinsey partner Tobias Schneiderbauer were cautiously optimistic that the economic conditions in trucking could improve toward the back half of the year.

Economic Uncertainty at the Forefront

The two spoke with North American trucking media at the 2026 CES electronics show in Las Vegas on January 6.

Rittstieg described an industry caught between weak near-term demand and long-term investment pressure—an uncomfortable place for OEMs, fleets, and anyone trying to read the tea leaves on Class 8 orders.

Photo: McKinsey & Company

His framing matches what many in this business are feeling: The market doesn’t look like it’s falling apart, exactly. But it doesn’t look like there will be smooth sailing in the near future, either.

For starters, Rittstieg noted that truck OEMs are getting hit hard on both the sales and profitability fronts.

That matters, he said, because the commercial vehicle industry is entering a period where manufacturers are expected to fund major technology transitions and retool their operations, even while the core business is under strain.

When truck orders are soft and profit is compressed, big “future investments” become harder to justify, and harder to execute.

How Truck Makers Are Dealing With the Market Uncertainty

Rittstieg said this is not a situation that will improve soon. Rather, he framed it as an operating reality for the early part of 2026, with OEMs forced into a defensive posture even as they plan for what comes next.

Asked whether McKinsey sees any bright spots in the heavy-duty market, Rittstieg didn’t hesitate.

“Not really,” he said. “None that I would be confident in.”

The problem, he explained, is that the usual obvious ”safe harbor” vehicle segments that hold up while others soften, such as vocational trucks, aren’t standing out in a way he would hang his name on.

And that points directly to what he sees as the key driver of the current order environment.

“Uncertainty is killing orders more than the lack of fleet profitability,” he said.

A lot of freight recessions can be explained with a familiar list: too much capacity, weak rates, slow demand, and carriers reacting accordingly.

Trucking Fleets Circle the Wagons

“What’s driving the postponement of purchases is uncertainty more than actual profitability right now,” Rittsieg said. “The uncertainty is just huge.”

He noted that many motor carriers have managed costs, parked equipment, right-sized networks, and tightened operations.

But in an environment shaped by shifting policy, pricing uncertainty, and broader macro questions, it’s hard to pull the trigger on major capital spending. Instead, heavy-duty trucking fleets are slowing their buying and stretching trade cycles.

Rittstieg said this is a textbook response to a freight recession. But because this one has stretched on for so long now, the usual “wait it out” phase has lasted longer than usual.

Photo: McKinsey & Company

Many fleets can delay truck replacement longer than normal, he said, especially if they have good maintenance programs, a stable customer base, and enough cash on hand to keep older trucks productive.

But that strategy has a limit, he warned. And McKinsey’s forecast for a potential recovery is rooted less in a sudden freight surge and more in the inevitability of equipment aging out.

“The most likely recovery point for the industry is forced replacement of older trucks,” he explained. “Eventually, fleets have to replace trucks. Not because the outlook becomes crystal clear, but because the equipment can’t be kept in service indefinitely.”

He emphasized that this is hope more than conviction, on McKinsey’s part. But, he added, it’s the most realistic mechanism on the table to jump-start a more economically robust trucking industry.

The Truck Maker Pricing Dilemma

Rittstieg pointed to the second half of 2026 as the window many in the industry are watching — again, not as a guaranteed snapback, but as a plausible turning point driven by replacement need.

“There is some hope that this is going to happen…in the second half of this year,” he said. “I haven’t heard anything yet, but…that’s the scenario we’re looking at.”

On the OEM side of the equation, Rittsieg said North American truck manufacturers face a pricing problem they can’t easily solve.

This, he said, was the “tension” tension between cost increases and the market’s ability — or willingness — to absorb higher prices.

Rittstieg said OEMs are currently hesitant to materially raise transaction prices because they’re already dealing with weak orders.

But tariffs and other cost drivers can force a “price reset” over time. That creates a nasty choice: protect margin and risk even fewer orders, or protect volume and take the profitability hit.

“The OEMs have been hesitant to really increase prices,” he said, “because they’re already looking at empty order books.”

If costs continue to rise and price increases lag, OEM profitability gets squeezed further. On the other hand, If OEMs raise prices aggressively, fleets may delay purchases even longer.

Either way, it’s not a clean setup for a fast recovery.

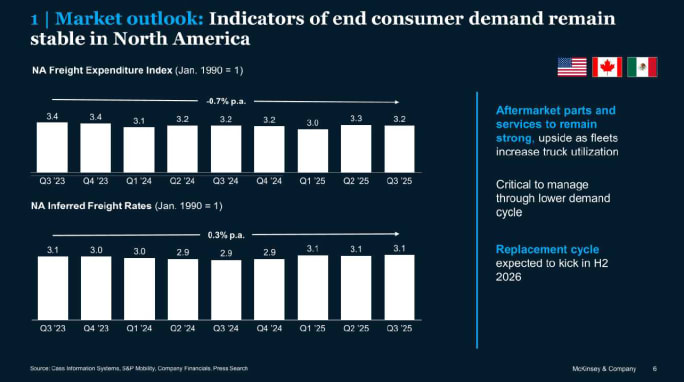

The Rise of the Truck Parts Aftermarket

When new-truck demand is soft, manufacturers look harder at what happens after the sale, Rittstieg said.

OEMs are under near-term pressure to defend and grow their aftermarket businesses, because that’s where steadier revenue comes from when orders dry up.

Photo: McKinsey & Company

McKinsey has found that roughly one out of every three dollars spent over a truck’s lifecycle happens post-sale.

The strategic play for OEMs in this situation is therefore obvious: Capture more of the money spent on aftermarket parts and maintain relationships with fleet customers through enhanced vehicle service and support.

For fleets, that can translate into OEMs pushing harder on service packages, parts programs, maintenance solutions, and anything that keeps customers in the factory ecosystem longer.

'The U.S. is the Market You Want to be In'

As bleak as the trucking industry appears to be at the moment, Rittsieg said there is still cause for optimism.

“The U.S. is still the best truck market globally,” he said. “When it comes to profit pools globally, the U.S. is the market you want to be in.”

That fact won’t make the early part of 2026 any easier for OEMs or fleets, he added. But it does help explain why OEMs continue to fight so hard for this market — and why, in Rittsieg’s view, manufacturers may shift even more resources and focus toward the U.S. over time.

“It’s a personal hypothesis for me,” he said. “OEMs…will shift more resources and focus towards the U.S… I’m still pretty bullish on the U.S. as a market.”

That’s the nuance in McKinsey’s message: The near term may be “more of the same,” but the U.S. is still where global truck makers make their money.

The industry may be grinding through a painful cycle, but it’s doing it in the most valuable truck market on earth.

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →