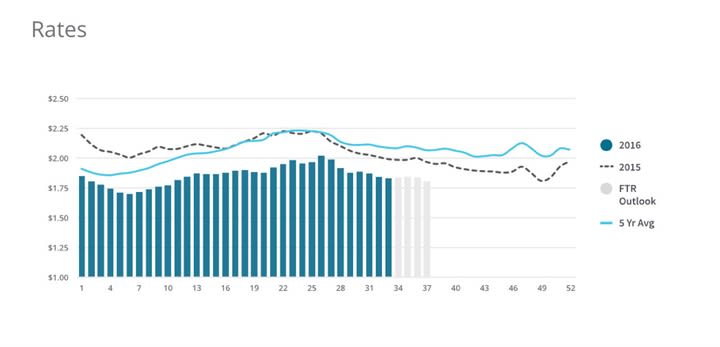

3 Trends in the Spot Freight Market

As FTR and Truckstop.com apply "big data" analysis to spot market pricing, Noel Perry, FTR transportation economist, offers some insights into the volatility of spot pricing and how spot prices correlate with contract pricing.

Graph courtesy FTR and Truckstop.com

As FTR and Truckstop.com apply "big data" analysis to spot market pricing, Noel Perry, FTR transportation economist, offers some insights into the volatility of spot pricing and how spot prices correlate with contract pricing.

1. Spot prices have been rising more than contract prices.

The data being analyzed starts in the first quarter of 2008, just before the big downturn. Since the bottom of that recession, contract prices have averaged a 1% quarter over quarter growth (annualized). Even with the big decline last year, spot prices have averaged 2%. This is consistent with the big move of random freight from the edges of contracts into the spot market, Perry notes. Volume has built, and so have rates.

"I expect this trend to peak in 2019 with the coming crisis in regulatory drag," Perry says. "After that is unclear."

2. Spot prices are way more volatile.

This is no surprise, Perry says. The spot market is defined as the home of swings in random demand. The capacity pressure indices calculated by Truckstop.com and DAT both swing widely in almost lockstep. It follows that price changes swing widely.

The standard deviation of spot rate changes since the bottom of the last recession is five times larger than that of contract rates. "In case you have forgotten your college stat definitions, that means spot rate growth varies five times more than contract rate growth," he says.

3. Both spot and contract pricing lag changes in capacity utilization.

With spot prices, the lags between market events and price response are short, perhaps up to a quarter, Perry says. The response is not instantaneous because truckers and shippers take time to realize that a change is required. There are also some small delays in the statistics. As big data (and forecasting tools) emerge, this lag should be shortened because market decision makers will know that something is happening sooner, he notes.

Contract rates have a much more noticeable lag. They tend to peak two quarters after spot rates move. In part, this is due to the nature of data collection and the schedule for contract renewals. In part, it is the lag in capacity migration between the two segments.

Both customers and carriers work to keep market conditions stable in this segment," Perry explains. Changes, increasingly come from outside forces overwhelming those efforts. Driver supply is one good example of such outside forces. If spot rates rise at some point, drivers serving that market (and carriers) will earn enough to justify leaving dependable contract situations. But rates have to climb and stay high for a while before drivers will take that risk.

"We know from history that strong changes in rate levels tend to last longer than one would expect," Perry said. "Both carriers and shippers get used to market conditions and tend to sustain them for a while after market conditions change. This is human nature.”

He pointed out two recent instances of this. First, the six-month capacity crisis of early 2004 funded a two-year burst in rates. More recently, the 2014 spot rate acceleration lasted until mid-2015 despite the fact that its first accelerant, bad winter weather, subsided by June of 2014, and the second accelerant, hours of service changes, were suspended in December 2014.

More Fleet Management

What Geotab's New AI Connector Means for Fleets

Fleets can now ask their usual AI assistants questions about maintenance, safety, fuel use, and vehicle performance, using their live Geotab data, and take action on the answers without leaving their preferred AI tool.

Read More →

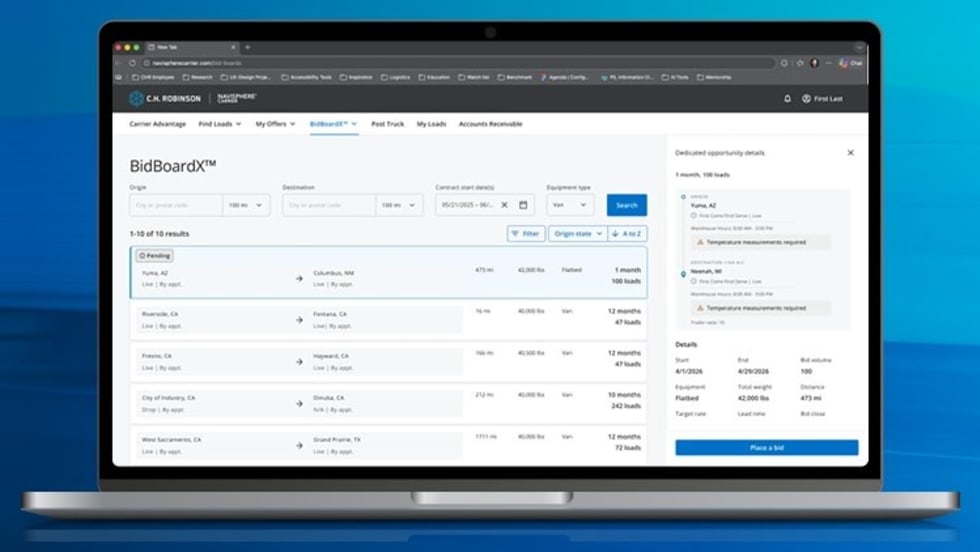

New C.H. Robinson Tool Opens Door to More Predictable Freight

BidBoardX lets carriers search, bid on, and secure committed freight opportunities through a single digital marketplace.

Read More →

New York City's Microhub Project is Delivering Results

Trucking, last-mile delivery companies, and environmental advocates like what they are seeing so far with New York's microhub program.

Read More →

Why Truck Detention Keeps Costing Fleets Time and Money

A 2024 ATRI study found detention affects nearly 40% of truckload stops and costs the industry more than $15 billion annually. Despite the toll on drivers, fleets, and supply chains, the problem remains stubbornly persistent.

Read More →

Time is Running Out to Apply for Exclusive HDT Event

Heavy Duty Trucking Exchange brings fleet managers and suppliers together for the deeper conversations that lead to ideas, partnerships, and solutions. Time is running out to apply for the September event.

Read More →

Amazon Launches Less-Than-Truckload Freight Offering for All Businesses

This launch is the latest addition to Amazon Supply Chain Services, a portfolio of supply chain capabilities from Amazon, including freight, distribution, fulfillment, and parcel shipping.

Read More →

Import Cargo Volume to See Year-Over-Year Gain Again in June, Then Remain Below 2025 Levels Into Fall

After July, the report predicts a weakening in import volume as consumer uncertainty remains high and the impact of increasing inflation takes its toll.

Read More →

AUCTION OF EQUITY INTEREST IN HEAVY HAUL TRUCKING COMPANY!!

Mark your calendar: June 30, 2026 (10:00 a.m. PDT). A 37.5% ownership interest in MagnaTrans, LLC, a California limited liability company doing business as Magna Transportation Group, will be sold in an in-person and online auction to the highest bidder or bidders under Article 9 of the Uniform Commercial Code. The Rancho Cucamonga-based heavy haul and over-dimensional trucking company operates across California, Oregon, and Arizona.

Read More →

Volvo Trucks Adds Unattended Over-the-Air Software Update Capabilities

The latest evolution of Volvo’s over-the-air update technology allows software updates to run while trucks are parked, helping fleets keep vehicles current without disrupting operations.

Read More →

How Waste Connections is Using Data, Telematics, and AI

How do you manage and maintain more than 18,000 connected trucks? Data. Lots of it.

Read More →