What's Behind the Tight Freight Market, and How Long Will It Last?

Although the April 1 start to “hard enforcement” of the electronic logging device mandate does not seem to have had a huge effect on trucking capacity (except perhaps in flatbeds), there are a number of other factors that are working to keep capacity tight and rates high, likely at least until late this year, according to FTR.

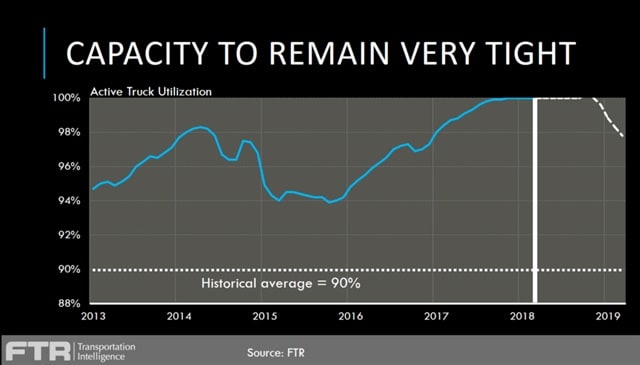

FTR expects trucking to remain near full capacity until near the end of the year and into 2019. Graph: FTR

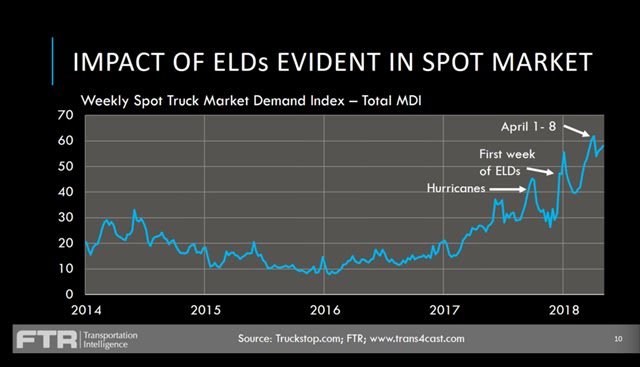

The spot market is one way to look at the impact of the ELD mandate on capacity. Graph: FTR/Truckstop.com

Although the April 1 start to “hard enforcement” of the electronic logging device mandate does not seem to have had a huge effect on trucking capacity (except perhaps in flatbeds), there are a number of other factors that are working to keep capacity tight and rates high, likely at least until late this year, according to FTR.

Avery Vise, FTR vice president of trucking research, shared the latest data with callers during a May 10 State of Freight webinar.

The key economic indicators affecting trucking are all positive, or at least neutral, he said. One possible concern is business inventories, which have ticked up higher recently. Potential reasons for that could be related to the need to keep product closer to customers for online sales, or even a reaction to the trucking capacity shortage itself, he said, as companies hold back some slower-moving inventory.

Of course, there are a number of external factors that could affect that rosy picture, including trade tensions and rising oil and fuel prices. But overall, Vise said, we can expect continued growth in the near term.

The flatbed sector is especially hot, and FTR expects loadings to be up 7% to 9% year-over-year through the year, perhaps even higher. Growth in van and reefer will not be as spectacular, but both will be solid through 2018.

ELD violations did not spike when ELD full enforcement hit Apri 1 – in fact, they dropped. Graph: FTR

The ELD Mandate and Capacity

But what everyone really wants to know is, how has hard enforcement of the ELD mandate affected capacity?

The best indicator for this, Vise said, is the spot market. Data from Truckstop.com, he said, suggests that capacity was tightening well before the initial December 18 ELD deadline, as many fleets went ahead and phased in the use of electronic logs before that date. “We did see a pretty substantial jump” during the first week of the ELD mandate, he said.

However, when you look at the April 1 deadline, at which point drivers were to be put out of service and points assessed on a carrier’s CSA record, something interesting happened, Vise said. “While the [Truckstop.com] MDI did rise the first week of April, it dropped the following week. That could reflect some typical softness after Easter, but the numbers do suggest there’s not any kind of catastrophe related to hard enforcement. In fact, the period between Dec. 18 and April 1 might have represented the worst of the impact.”

Even more curious, he said, is what happened with weekly ELD violations, which actually dropped during the first week of full enforcement.

One possible reason for that is that carriers simply waited to install or activate their ELDs until the hard deadline, knowing that until then the violations would not mean an out of service violation or CSA points.

Another possible reason would be that anti-ELD owner-operators and small carriers simply parked their trucks. However, he said, if that were the case, “we would expect a huge imbalance in the spot market, which we did not see.”

However, the data also shows, unsurprisingly, that non-compliance with the ELD mandate “has been almost totally on the lower end of the market… nearly 80% of violations are carriers with fewer than 20 trucks.” Carriers with 101 to 999 trucks made up only 3% of the violations.

Why Is the Flatbed Sector so Hot?

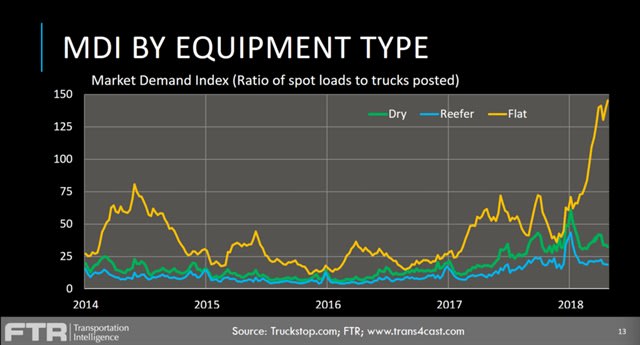

Truckstop.com’s Market Data Index tracking the spot market is overall in record territory, but that is principally due to “unprecedented tightness” in the flatbed sector, Vise said. Flatbed rates are up 45 cents per mile since the end of 2017, while van and refrigerated freight rates are down from their year-end highs.

Truckstop.com's Market Demand Index shows flatbeds have been in high demand on the spot market. Graph: FTR/Truckstop.com

Several possible reasons are combining to create this situation, he said, both on the demand side and the supply side of the equation. There’s more demand for flatbeds coming from recent strength in manufacturing and construction, as well as recent increases in petroleum prices pushing more domestic production.

On the supply side, Vise said, many people think the ELD mandate is hitting flatbed the hardest. This sector includes a lot of owner-operators and small carriers and is typically not the first to adopt new technology, he noted.

“There could also be equipment constraints. We saw a sharp increase in flatbed trailer orders starting in September, and that continued until very recently.”

The Driver Shortage and Tight Trucking Capacity

For over a year now, fleets have been saying that they could haul more freight if only they had the capacity to do it – chiefly limited by the driver shortage. And that’s certainly still continuing.

In the first three months of the year, the for-hire trucking industry was busy adding jobs, but that fell in April. “And this is not in a period where you would anticipate freight demand to soften to any kind of degree that would account for job losses,” Vise said. “We think carriers have largely exhausted the supply of potential drivers who already had CDLs and were employable.”

In addition to the low level of unemployment nationwide, Vise said, “you have competition [for labor] from sectors like manufacturing and construction, and even local delivery, which has grown sharply over the last year.”

One of the problems, he said, is that despite the number of carriers raising driver pay overall, “there isn’t much difference between wages in trucking and those in home building and manufacturing.”

What’s the Outlook for Trucking Capacity?

When you take all these factors, and add in the fact that railroads do not seem to be in a position to provide much additional capacity, either, “you end up with essentially full utilization of seated trucks, and this is where we’ve been essentially since the hurricanes. We don’t see any meaningful change until the fall.”

By that point, he said, fleets will have taken delivery of new trucks and trailers that are currently in the production pipeline, and aggressive driver recruiting efforts may have borne fruit by then. Also acting to help ease the capacity crunch will be things like schedule changes, more drop-and-hook operations, and other ways to eke out more efficiencies and take out lost time.

As a result, he said, FTR expects elevated year-over-year growth in rates to continue through the second quarter, but to come down somewhat from “fairly inflated levels” later in the year.

Don’t expect that change to come from any reprieve from the ELD regulations, Vise said – although he sees it as “quite possible” that a current temporary exemption for livestock haulers will be made permanent.

More likely, Vise said, would be relief from the underlying hours of service rules themselves, although that’s a longer-term prospect. He pointed out that there’s a pilot program under way to test moving back to a split-sleeper berth option, and the Owner-Operator Independent Drivers Association has petitioned for the ability to pause the 14-hour on-duty clock once during a shift for up to three hours.

“If these things come together during a business-friendly administration, I would anticipate a good chance that one of these has a chance of happening in the next few years,” he said.

Related: Fleet Survey Shows Driver Shortage Continues to Impact Equipment Buying Plans

More Fleet Management

How Innovative Trucking Leaders Turn Change Into an Advantage

As the pace of change accelerates in trucking, the fleets that adapt best have more than the latest technology. They have cultures that embrace improvement.

Read More →

Freight Broker Bonds Just Got Harder to Get. Here's What That Means for Your Fleet.

When it gets harder for a freight broker to prove they are financially sound, the ones who cannot clear that bar get pushed out of the market. And those are exactly the brokers who used to leave motor carriers holding the bag.

Read More →

Long-Awaited Canadian Border Bridge to Open in Detroit

For trucking, the bridge opening should offer immediate improvements in efficiency and reliability, with new customs facilities, expanded inspection capacity, and direct freeway-to-freeway connections.

Read More →

Aurora Rolls Out Next Generation of Driverless Trucks for Commercial Freight

Aurora's latest autonomous trucks it's rolling out with International feature lower-cost hardware designed for a million miles as the company expands commercial driverless freight operations across the U.S. Sun Belt.

Read More →

Freight Tonnage Down, Rates up, as Lower Capacity Powers Trucking Recovery

The recovery from the freight recession continues to be driven by reduction in capacity rather than by increased demand.

Read More →

Think Your Trucking Fleet Isn't Using Much AI? Think Again

Shadow AI — the use of unauthorized artificial intelligence tools at work — is becoming increasingly common, putting sensitive company data at risk. Learn how trucking fleets can protect sensitive data while embracing AI.

Read More →

ArcBest Consolidates Brands, Cuts Workforce

The company will bring three business units under the ArcBest brand, eliminate about 2% of positions, and expects the changes to generate $40 million in annual savings.

Read More →

Trucking Fleets Faced Record Operating Costs During Third Year of Freight Recession

ATRI's annual operational cost report shows carriers trimmed fleets, delayed equipment purchases, and ran older trucks as expenses continued to outpace freight rates.

Read More →

Michelin Adds AI Assistant to MyConnectedFleet Platform

Michelin’s new generative AI tool delivers instant fleet insights, helping managers analyze fuel use, tire maintenance, vehicle status, and operational performance without manually creating reports.

Read More →

LytxOne Platform Now Features AI, Compliance, and Asset Tracking Tools

New enhancements add AI-powered insights, asset tracking, compliance automation, and configurable privacy controls to Lytx's all-in-one fleet management platform.

Read More →